Check Bounce: What It Means & What to Do in 2026

You wrote a check for past-due property taxes three weeks ago. The payee finally deposited it yesterday, and now your bank is hitting you with an NSF fee because you'd already moved that money. A check bounce you didn't see coming. Your first thought: "Is this a crime? Am I getting sued?" Take a breath - we've seen people spiral over a single bounced check when the fix takes 15 minutes. You're probably fine, but you need to understand what just happened, what it'll cost, and how to make it right.

What you need (quick version):

- You wrote a bounced check. Contact the payee immediately, cover the amount plus any fees, and call your bank to request a fee waiver. Many banks waive the first one if you ask.

- You received a bounced check. Contact the writer, give them a chance to make it right, re-deposit once, then escalate: demand letter, small claims court, police report if it looks intentional.

- You want to verify a check before depositing. Inspect the physical security features, verify the MICR line and ABA routing number independently, and call the issuing bank using a number you find yourself - never the one printed on the check.

What Is a Bounced Check?

A bounced check - also called an NSF check, returned check, rubber check, or dishonored check - is a check your bank refuses to honor. The mechanics are simple: you write or deposit a check, the bank processes it, discovers it can't be paid, and sends it back. Then fees hit both sides.

The writer gets charged an NSF or overdraft fee by their bank. The recipient gets charged a returned-check fee by theirs. The only winners are the banks.

Why Checks Bounce

Checks don't just bounce because someone's broke. There are at least eight common reasons, and some have nothing to do with your balance.

Insufficient funds (NSF). The classic. Your account doesn't have enough to cover the check - the most common reason by far.

Closed or frozen account. If the account was closed, flagged for fraud, or frozen by a court order, the check goes nowhere.

Stale date. Most banks won't honor a check older than 180 days. That two-month-old paycheck sitting in your drawer? Your bank isn't obligated to process it.

Stop payment. The writer called their bank and canceled the check before it cleared. This costs the writer a fee too - usually around $30-$35.

Signature or information mismatch. Wrong date, missing signature, amount written in words doesn't match the numbers. Banks catch these more often than you'd think.

Fraud or forgery. Someone altered the check, forged a signature, or the check itself is counterfeit.

Bank error. Rare, but it happens. Processing mistakes, system glitches, misrouted transactions.

Post-dated check processed early. You wrote a check dated for next Friday, but the recipient deposited it today. Banks generally aren't required to wait for the date on the check.

One detail worth knowing: when multiple checks hit your account on the same day and there isn't enough to cover all of them, the bank decides which ones get paid and which bounce. The posting order can increase the number of overdrafts and NSFs - and the fees you get hit with.

Here's the scenario that catches people off guard: a Reddit user cashed three paychecks at once, with the oldest being two months old. Two of them bounced days later - after the funds initially appeared in their account. "It cleared" doesn't always mean "it's good." That distinction matters, and we'll get into why.

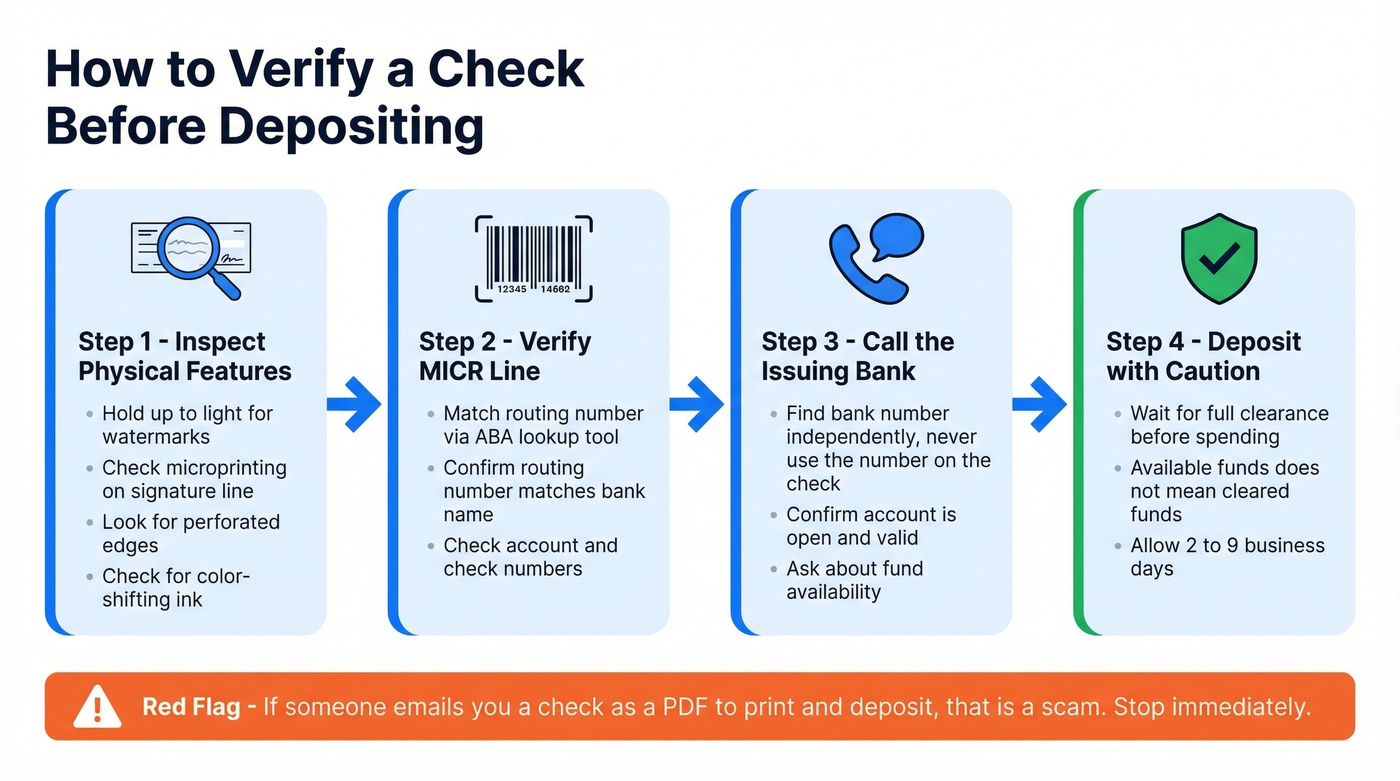

How to Verify a Check Before Depositing

Most articles skip this entirely. Everyone tells you what to do after a bounced check. Almost nobody tells you how to catch a bad check before you deposit it.

Physical Security Features

Before you even think about depositing, look at the check itself. Legitimate checks have security features that are hard to fake:

- Watermarks. Hold the check up to a light. You should see a faint design or pattern embedded in the paper.

- Microprinting. Look at the signature line or borders with a magnifying glass. Legitimate checks have tiny text that appears as a solid line to the naked eye but reads as words up close. Photocopied fakes can't reproduce this - the text blurs.

- Perforated edges. Checks torn from a checkbook have at least one rough, perforated edge. A check with four smooth, cleanly cut edges was likely printed on a standard printer.

- Color-shifting ink or holograms. Some banks use ink that changes color when tilted, or holographic security strips.

If the check was emailed to you as a PDF to print and mobile-deposit - stop. That's a textbook scam pattern. Legitimate businesses don't email checks for you to print at home.

Verify the MICR Line and Routing Number

The MICR line - those machine-readable characters printed in magnetic ink along the bottom of the check - contains three critical pieces of information: the bank's routing number, the account number, and the check number. On a legitimate check, these characters have a distinctive feel and font that standard printers can't replicate.

You can verify the routing number through the ABA's routing number lookup tool or the Federal Reserve's FedACH directory. If the routing number doesn't match the bank printed on the check, stop. That's your clearest fraud signal.

Call the Issuing Bank

This is the most reliable verification step a consumer can take. Look up the issuing bank's phone number independently - through their official website or a Google search. Never call the number printed on the check itself, because scammers print their own phone numbers.

When you call, have this ready:

- Check number

- Amount

- Date on the check

- Payor's name

Ask the bank to confirm the account is open and valid. Some banks will confirm whether funds are available; others won't, citing privacy policies. Either way, confirming the account exists and is active eliminates the most common fraud scenarios.

Why Verification Isn't a Guarantee

Even if the bank confirms funds today, that money could be withdrawn tomorrow. Verification tells you the check is legitimate and the account is active right now. It doesn't guarantee the check will clear three days from now. Think of it as reducing risk, not eliminating it.

This "verify before you act" principle applies well beyond paper checks. In B2B sales, sending outreach to an unverified email address is the equivalent of depositing an unchecked check - you're hoping it lands, but you haven't done the work to confirm. Tools like Prospeo verify B2B emails in real-time with 98% accuracy, so nothing bounces. Same principle, different domain.

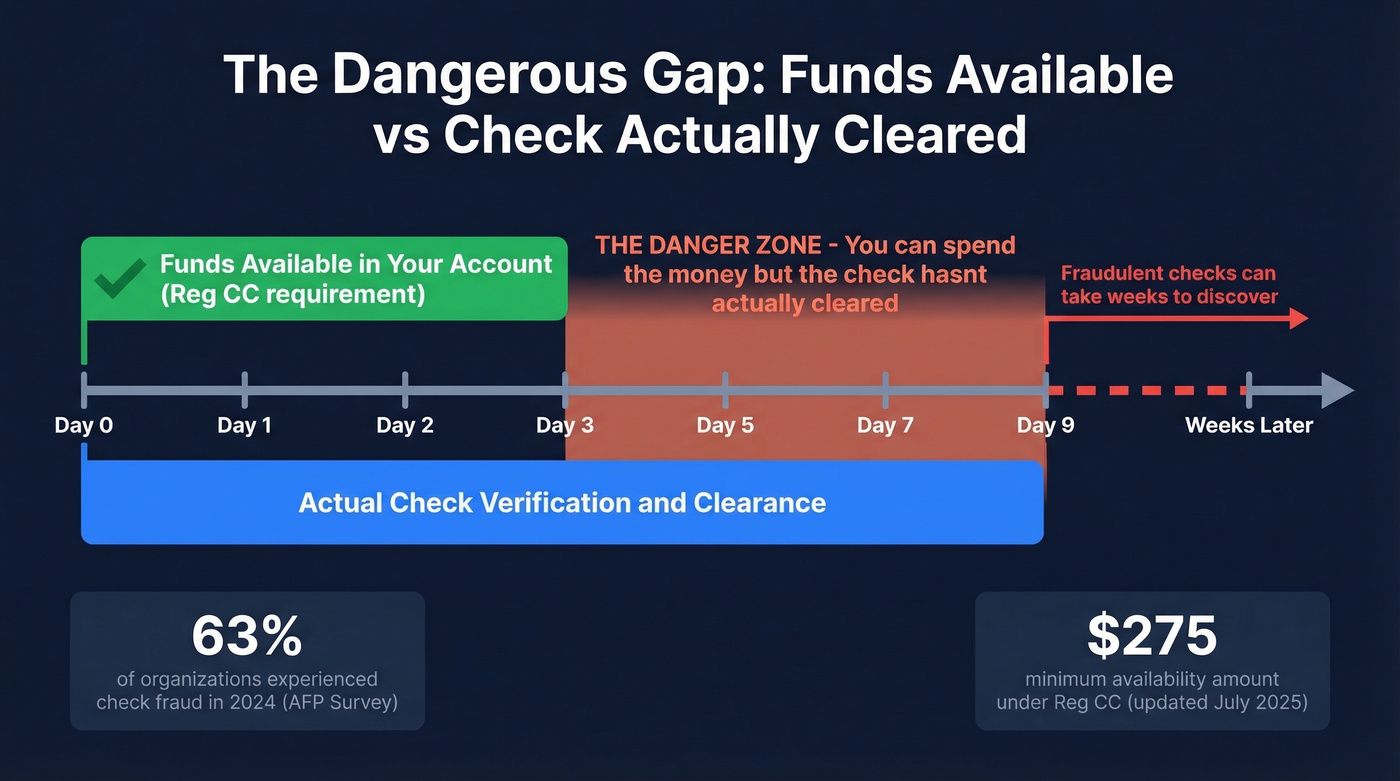

How Long Until a Bounced Check Shows Up?

Here's where the system gets genuinely confusing: your bank makes funds available before the check actually clears. This isn't a bug - it's federal law.

Regulation CC requires banks to make deposited funds available within specific timeframes, often within 1-2 business days for routine deposits. But "available" doesn't mean "cleared." The actual verification process - where the issuing bank confirms the check is good - can take longer. Checks can clear as quickly as the same business day, with many clearing within 2 business days, but extended holds can stretch 7 to 9 business days. For fraudulent checks, the FTC warns it can take weeks to discover a fake.

A few important distinctions. A "business day" under Reg CC means Monday through Friday, excluding federal holidays. A "banking day" is any business day the bank is open for substantially all banking functions, up to its posted cutoff hour. Deposit a check at 9 PM on Friday, and the clock doesn't start until Monday.

Under current Reg CC thresholds (updated July 2025), the minimum availability amount is $275 and the large-deposit threshold is $6,725. These numbers adjust every five years for inflation.

The practical takeaway: 63% of organizations experienced check fraud in 2024, per an AFP survey. The gap between "funds available" and "check cleared" is exactly where fraud lives. Don't spend deposited check funds immediately, especially for large amounts or checks from unfamiliar sources.

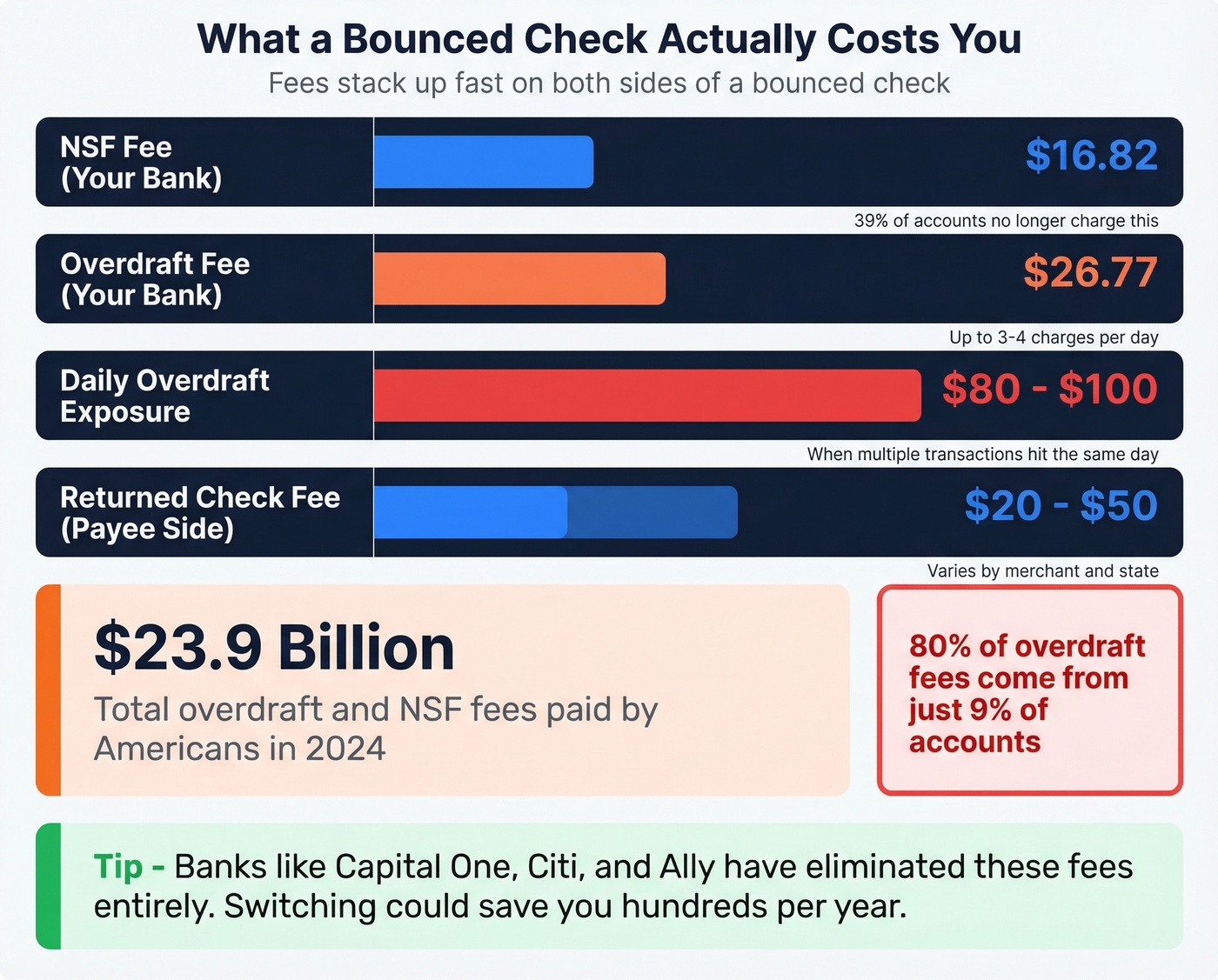

What a Check Bounce Costs

Banks charge you a fee for not having enough money. Then they charge the recipient a fee for receiving your bad check. The system punishes both sides, and the numbers add fast.

Average Fees

| Fee Type | Average Amount | Notes |

|---|---|---|

| NSF fee (your bank) | $16.82 | 39% of accounts no longer charge |

| Overdraft fee (your bank) | $26.77 | Up to 3-4 per day |

| Daily overdraft exposure | $80-$100 | If multiple transactions hit |

| Returned check fee (payee) | $20-$50 | Varies by merchant/state |

| Industry total (2024) | $23.9B combined | $12.1B overdraft + $11.8B NSF |

That industry total isn't a typo. Americans paid nearly $24 billion in overdraft and NSF fees in 2024. A Reuters analysis found that top-bank fee revenue actually rose 2% to $2.99B in the first nine months of the year - this after a proposed CFPB rule that would've capped overdraft fees at $5 was scrapped. The CFPB estimated that cap would've saved consumers $5 billion a year.

Nearly 80% of overdraft charges come from just 9% of accounts. The people paying the most fees are the ones who can least afford them.

Banks That Dropped NSF Fees

Capital One stopped charging NSF fees in 2021 and eliminated overdraft fees in early 2022. Citibank dropped overdraft, NSF, and returned-item fees entirely in June 2022. Ally eliminated overdraft fees permanently in June 2021. Bank of America stopped NSF fees in 2022 and cut its overdraft fee from $35 to $10, capping it at two per day.

If you're still banking somewhere that charges $35 per overdraft with no daily cap, switch. The fee structure alone can save you hundreds a year.

You'd never deposit a check without verifying it first. Why send outreach to unverified emails? Prospeo's 5-step verification delivers 98% email accuracy - cutting bounce rates from 35% to under 4% for teams like Snyk and Meritt.

Verify every email before it bounces and kills your domain reputation.

What to Do When a Check Bounces

If You Wrote It

Don't panic, but don't ignore it either.

Contact the payee immediately. Don't wait for them to call you. Acknowledge the situation and commit to a timeline for making it right. This single step prevents most escalations. We've seen a $50 bounced check turn into a $500 legal headache simply because the writer avoided the payee's calls for two weeks.

Deposit funds and arrange payment. Cover the original amount plus any fees the payee incurred. If you can't cover it all at once, propose a payment plan in writing.

Call your bank and ask for a fee waiver. If this is your first NSF or overdraft, many banks will waive the fee. Be polite, be direct, and reference your account history.

Set up overdraft protection. Link a savings account or line of credit to your checking account. The transfer fee is usually $10-$12, sometimes free depending on the bank, but it's cheaper than a $27 overdraft charge.

Document everything. Keep records of your communications with the payee and your bank. If this escalates, you want a paper trail showing you acted in good faith.

If You Received It

This is the harder side. You've already provided the service or delivered the goods. The customer isn't returning calls. Here's how to escalate:

Contact the writer. Give them a reasonable window - 5 to 7 business days - to make the payment. Put it in writing so you have a record.

Re-deposit once. Many banks allow at least one re-deposit attempt. If it bounces again, don't keep trying. You'll just rack up more fees on your end.

Send a certified demand letter. This is a formal written notice that the check bounced, the amount owed including your fees and any statutory penalties your state allows, and a deadline to pay. Send it via certified mail with return receipt. Many states require this letter before you can pursue legal action.

File in small claims court. For amounts under your state's small claims limit - often $5,000-$10,000 - this is the fastest legal remedy. Filing fees run $30-$100.

File a police report if you suspect intent. One small business owner on Reddit described chasing a $400 bounced check for two weeks. The check was number 003 from a brand-new checkbook, which strongly suggested the customer knew the account couldn't cover it. Police took the paperwork and encouraged the owner not to drop charges.

Is Bouncing a Check Illegal?

Let's go back to that property tax scenario. You wrote a check in good faith, the payee sat on it for three weeks, and your balance had changed by then. You're not a criminal.

The key legal distinction is intent. Most state "worthless check" laws require that the writer knew funds were insufficient at the time they wrote the check, with intent to defraud. An accidental bounce - where you genuinely believed you had the funds - doesn't meet that threshold.

Postdating a check is generally legal too, unless you wrote it knowing it wouldn't be honored on the future date.

Where it gets serious is when someone writes checks they know will bounce, especially repeatedly or for large amounts. Penalties vary by state and the check amount, and many states escalate from misdemeanor treatment at lower amounts to felony treatment above certain thresholds. If you're facing actual legal consequences, consult an attorney in your state.

Long-Term Damage: ChexSystems

Most people know that unpaid debts can hurt their credit score. Fewer know that bounced checks can lock you out of opening a bank account entirely.

What It Tracks

ChexSystems is a specialty consumer reporting agency regulated under the Fair Credit Reporting Act. It tracks your deposit account history: overdrafts, unpaid fees, returned checks, suspected fraud, and involuntary account closures. Banks check your ChexSystems report when you apply for a new account, and a negative record can get you denied. Merchants also use TeleCheck to screen check-writers at the point of sale, so a history of bounced checks can affect your ability to pay by check at retail stores.

The score range runs 100 to 899. Negative information stays on your report for five years.

That's not abstract. 4.2% of U.S. households - about 5.6 million - are completely unbanked, and ChexSystems records are a major contributing factor.

You're entitled to a free ChexSystems report once every 12 months. If you've bounced checks or had accounts closed, request yours at chexsystems.com.

How to Dispute a Record

If you find inaccurate information, you have the right to dispute it. Submit your dispute through the ChexSystems consumer portal, by phone, or by mail, with supporting documentation - bank statements, payment receipts, correspondence. By law, they have 30 days to complete the investigation (21 days for Maine residents). If the item is verified as inaccurate, it gets removed. If it stands, you can add a consumer statement to your file explaining the circumstances.

If your ChexSystems record is too damaged for a traditional bank account, look into second-chance checking accounts. Banks like Chime, Varo, and several credit unions offer accounts specifically designed for people rebuilding their banking history.

Fake Check Scams in 2026

It's absurd that in 2026, it can still take weeks to find out a check is fake. But that timing gap is exactly what scammers exploit.

The pattern is consistent: someone sends you a check - often for more than they owe - and asks you to deposit it and send the difference back via wire transfer, gift cards, or cryptocurrency. Your bank makes the funds available in a day or two. You send the money. Weeks later, the check turns out to be counterfeit, and you're on the hook for the full amount.

The FTC identifies several common scam types: mystery shopper jobs, personal assistant positions, car wrap advertising offers, prize or sweepstakes "winnings," and overpayment schemes. Job scam losses alone hit $501 million in 2024, up from $90 million in 2020. Total reported fraud losses reached $12.5 billion.

If you've already deposited a suspicious check and sent money:

- Gift cards: Contact the issuer immediately with the card numbers. Some can freeze remaining balances.

- Wire transfer: Call the wire transfer company and request a reversal. Speed matters - the longer you wait, the lower your chances.

- Money order: Request a stop payment from the issuer.

- Report it: File complaints with the FTC, the U.S. Postal Inspection Service if the check came by mail, and your state attorney general.

How to Prevent a Check Bounce

Every bank tells you to "monitor your balance." That's about as useful as telling someone to "eat healthy." Here's what actually works.

Set low-balance alerts at a specific threshold. Not at $0 - at $200 above your largest recurring payment. If your rent auto-drafts at $1,500, set an alert at $1,700. This gives you a buffer window to transfer funds before anything bounces.

Link overdraft protection. Yes, it's another fee (usually $10-$12 per transfer, sometimes free), but it's cheaper than a $27 overdraft charge and infinitely cheaper than the cascading damage of a returned check hitting your ChexSystems record.

Maintain a minimum buffer. Keep at least one month's worth of fixed expenses as a floor in your checking account. Treat that amount as untouchable.

Stop using personal checks for large payments. Here's the thing: 91% of U.S. businesses still used paper checks in 2024, and that's indefensible. The check system is a relic propped up by institutional inertia. For anything over $500, use a cashier's check, ACH transfer, or P2P payment. Cashier's checks are guaranteed by the bank. ACH transfers clear electronically. Both eliminate the "will it bounce?" uncertainty entirely. QuickBooks recommends waiting at least 30 days before spending funds from a newly deposited check if you can't verify it - that alone tells you how fragile the system is.

If you’re trying to prevent “bounces” on the email side too, start with list hygiene and verification basics in our guide on how to prevent email bounces.

FAQ

Can a bounced check affect my credit score?

Not directly - ChexSystems is separate from the three major credit bureaus. If the bounced check leads to an unpaid debt sent to collections, that collection account will appear on your credit report. The ChexSystems record affects your ability to open bank accounts, not your FICO score.

How many times can a bounced check be re-deposited?

Most banks allow one or two re-deposit attempts before refusing further processing. After that, pursue the check writer directly for a replacement payment via cashier's check or ACH transfer. Re-depositing repeatedly just generates more returned-check fees on your end.

Can I go to jail for bouncing a check?

Only if you wrote the check knowing funds were insufficient, with intent to defraud. Accidental bounces aren't criminal - prosecutors must prove intent, which is a high bar for a one-time NSF situation. Repeated bad checks or large amounts raise the stakes significantly.

What's the difference between an NSF fee and an overdraft fee?

An NSF fee means your bank rejected the payment and charged you for the failed transaction. An overdraft fee means your bank covered the payment on your behalf and charged you for that service. Overdraft fees tend to be higher ($26.77 average vs. $16.82 for NSF) because the bank actually fronted the cash.

How do I verify email addresses to prevent bounces in B2B outreach?

Run every address through a real-time verification system before sending - the same principle as verifying a check before depositing it. Prospeo's 5-step email verification catches invalid addresses, spam traps, and catch-all domains with 98% accuracy, preventing deliverability damage before it starts.

Bounced checks and bounced emails share the same root cause: acting on unverified data. Prospeo refreshes 300M+ profiles every 7 days - not every 6 weeks - so your outreach hits real inboxes at real companies, every time.

Stop guessing. Start verifying at $0.01 per email.