Go-to-Market Strategy for Telecommunications: The 2026 Playbook

Every telecom GTM guide online is a generic SaaS playbook with "telecommunications" swapped into the headers. That doesn't work. Telecom has regulatory layers, 6-12 month enterprise sales cycles, channel conflict that confuses 43% of buyers, and declining ARPU - none of which a standard framework addresses.

We've reviewed dozens of go-to-market plans built for telecommunications companies, and the ones that fail all share the same problem: they prioritize planning over execution. Stop building 50-page GTM decks. Start shipping.

The three motions worth investing in for 2026: API productization ($6.7B market by 2028), managed services bundling (85%+ of channel-led sales will include IT attachments this year), and NaaS marketplaces. Simplify procurement, resolve channel conflict, and reach verified decision-makers faster.

Why Telecom GTM Differs From Every Other Vertical

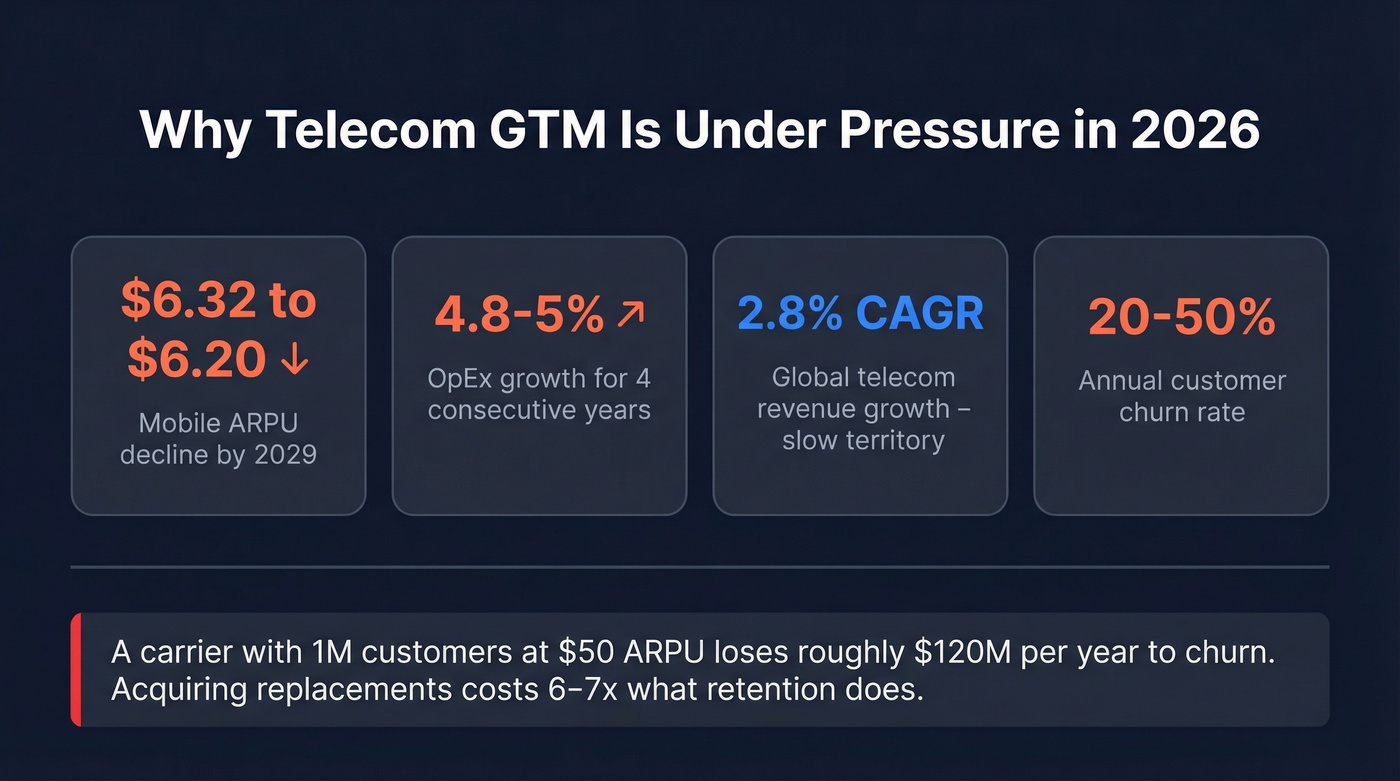

The economics are getting worse. PwC forecasts global mobile ARPU declining from $6.32 in 2024 to $6.20 by 2029 - you're selling harder just to stay flat. Operating expenses grew 4.8-5% for the fourth consecutive year, squeezing margins from both sides. Global telecom service revenue grows from $1.15T to roughly $1.32T by 2029 at a 2.8% CAGR. That's slow-growth territory, and investors know it: telecom stocks returned about 11% in 2024 while the S&P 500 returned roughly 25%, per Deloitte.

Churn makes everything worse. At 20-50% annually, a carrier with 1M customers at $50 ARPU hemorrhages roughly $120M/year. Acquiring replacements costs 6-7x what retention does.

There's a reason practitioners on r/sales can't even agree on what "GTM" means in telecom - the term is overloaded, and the execution gap is wider here than in any other B2B vertical. Telecom GTM doesn't fail at strategy. It fails at execution.

Five GTM Motions That Work in 2026

Traditional Connectivity

Global telecom revenue hits $1.15T and grows to roughly $1.32T by 2029 across direct enterprise, channel, and MVNO routes. This is table stakes, not a growth play. The real question is what you layer on top.

Managed Services Bundling

Omdia predicts 85%+ of channel-led telco sales will include IT services attachments in 2026. Enterprise buyers increasingly expect security, SD-WAN, and UCaaS bundled with connectivity. If you're still selling naked circuits, your partners are already looking elsewhere - and they won't tell you before they leave.

API Productization

This is the highest-growth motion in telecom right now, and it isn't close. IDC forecasts the telco API market at $6.7B by 2028, growing at 57.1% CAGR. Americas leads at $2.7B, followed by APAC ($2.1B) and Europe ($1.9B). GSMA Open Gateway spans 67 operator groups covering roughly 75% of global connections. The play: package network capabilities as developer-friendly APIs with self-serve docs and usage-based pricing. SIM swap detection and number verification are quick-win APIs that generate revenue now while you build out more complex offerings.

NaaS Marketplace

The NaaS market sits at an estimated $23.50B and it's reshaping how enterprises buy network services. The shift from CapEx to pay-as-you-go OpEx changes the GTM motion entirely: direct B2B self-serve portals, B2B2X partner resale, and ecosystem monetization all become viable. Here's the stat that should get your attention - roughly 50% of GTM outperformers run an online marketplace versus just 15% of companies losing share.

Private 5G and Network Slicing

With 88% of North America covered by 5G and 259M+ devices in the US, the infrastructure is ready. Private 5G is an enterprise-direct play - manufacturing floors, logistics hubs, healthcare campuses - sold through SI partnerships. Network slicing adds a programmable layer on top. This is consultative, long-cycle selling. Not a volume play. Skip this if your sales team doesn't have deep vertical expertise and existing SI relationships.

Telecom enterprise deals stall when reps waste months chasing bad contact data. Prospeo gives you 98% verified emails and 125M+ direct dials to CIOs, VPs of Network Ops, and procurement leads - refreshed every 7 days, not every 6 weeks. Layer in intent data tracking 15,000 topics to find enterprises actively evaluating vendor switches.

Cut 2-3 weeks off every telecom deal cycle starting today.

Channel Strategy: Solve the Conflict

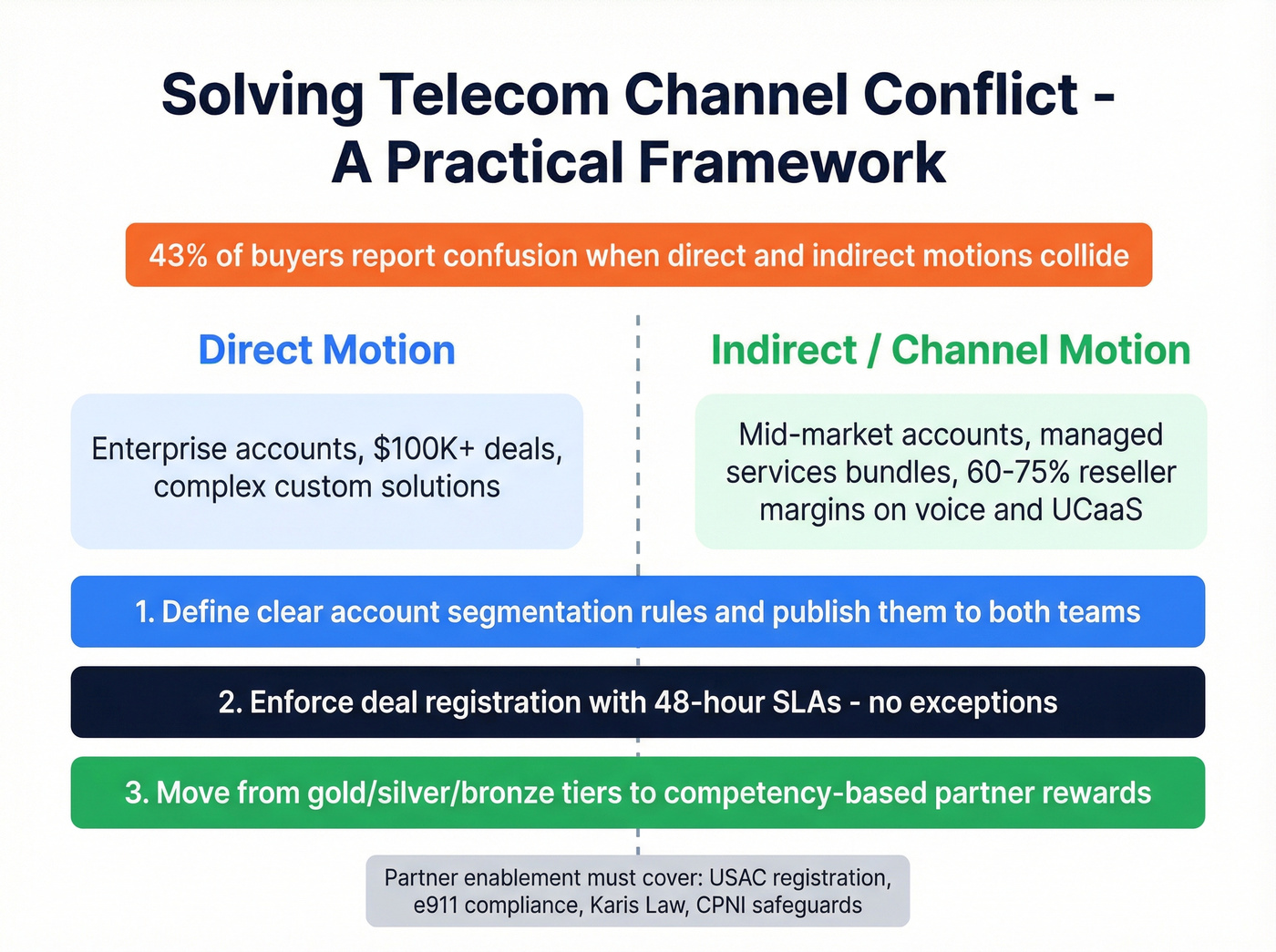

Let's be honest: channel conflict is telecom's most underestimated GTM killer. 43% of buyers report confusion when direct and indirect motions collide - higher than the 38% cross-industry average. That confusion doesn't just slow deals. It kills them.

The big operators are betting heavily on indirect. T-Mobile targeted 50% channel sales growth. Lumen aims for 70% indirect sales. Omdia predicts 100+ M&A and JV moves in 2026 reshaping telco portfolios. Reseller margins run 60-75% on voice/UCaaS bundles, which keeps partners engaged, but the model is shifting fast. At least one major US telco is expected to move to point-based partner rewards, replacing metallic tiers with competency-based programs. If you're still running gold/silver/bronze, you're behind.

Resellers also face real regulatory overhead - USAC registration, e911 compliance, Kari's Law location rules, and CPNI safeguards. Factor this into partner enablement or watch onboarding stall for months while legal sorts it out.

What actually works: Define clear account segmentation rules - enterprise direct, mid-market through partners - and enforce deal registration with 48-hour SLAs. Move from metallic tier programs to competency-based rewards that incentivize solution selling over volume.

Enterprise Sales Execution

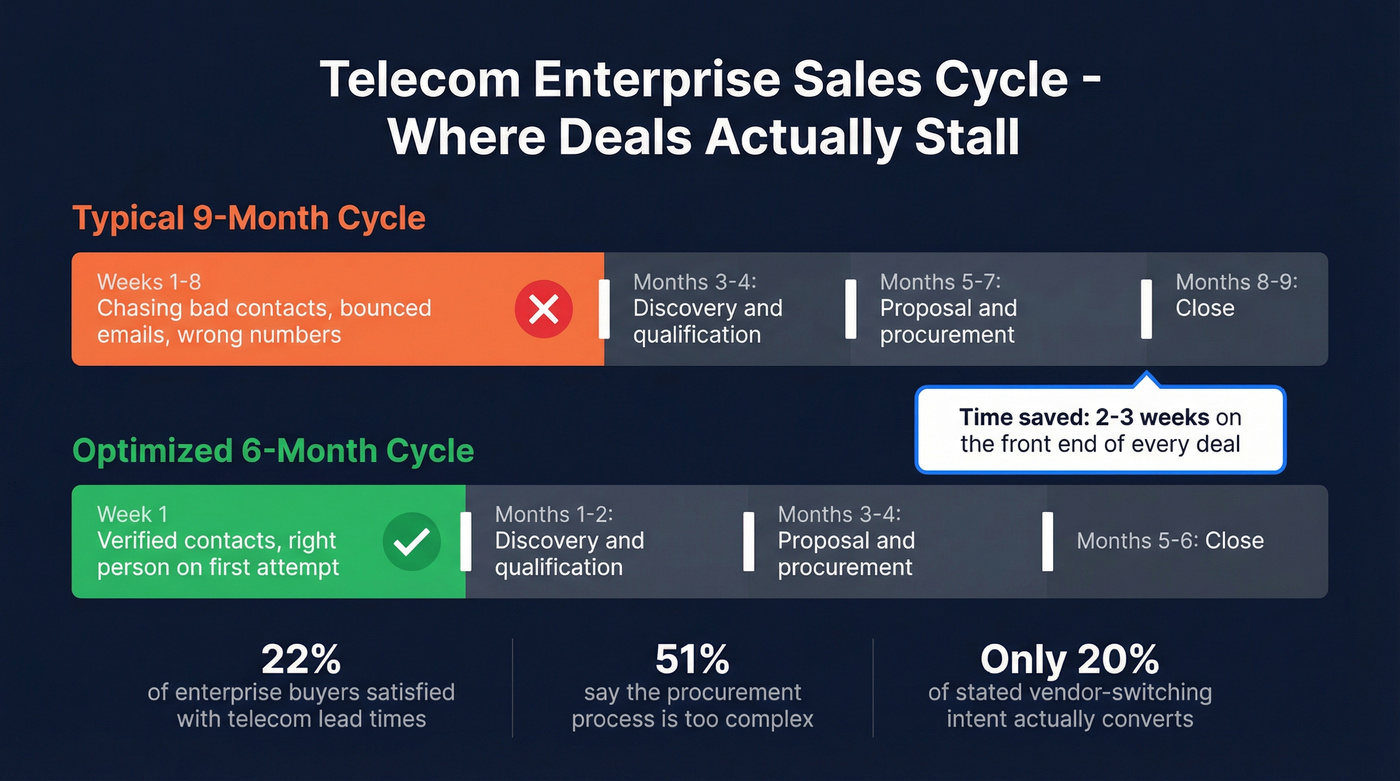

Here's the thing: if your deal size sits below $25K, you probably don't need a 6-month enterprise sales cycle - you need a simpler procurement process. Only 22% of enterprise buyers are satisfied with telecom lead times, and 51% say the process is too complex. Worse, only roughly 20% of stated vendor-switching intent actually converts. You're not losing to competitors. You're losing to inertia.

In our experience, telecom teams that start with verified contact data cut 2-3 weeks off the front end of every deal. When your cycle runs 6-12 months, starting with bounced emails and wrong numbers wastes the first two months on noise. We've seen teams using Prospeo's 7-day data refresh cycle and 98% email accuracy reach CIOs, VPs of Network Ops, and procurement leads on the first attempt instead of the third - across 125M+ verified mobile numbers globally. Layer in intent data tracking 15,000 topics to identify enterprises actively evaluating network upgrades or vendor switches, so reps prioritize accounts with real buying signals instead of guessing.

The difference between a 9-month close and a 6-month close often isn't your pitch deck. It's whether you reached the right person in week one or week eight.

Measuring Telecom GTM Performance

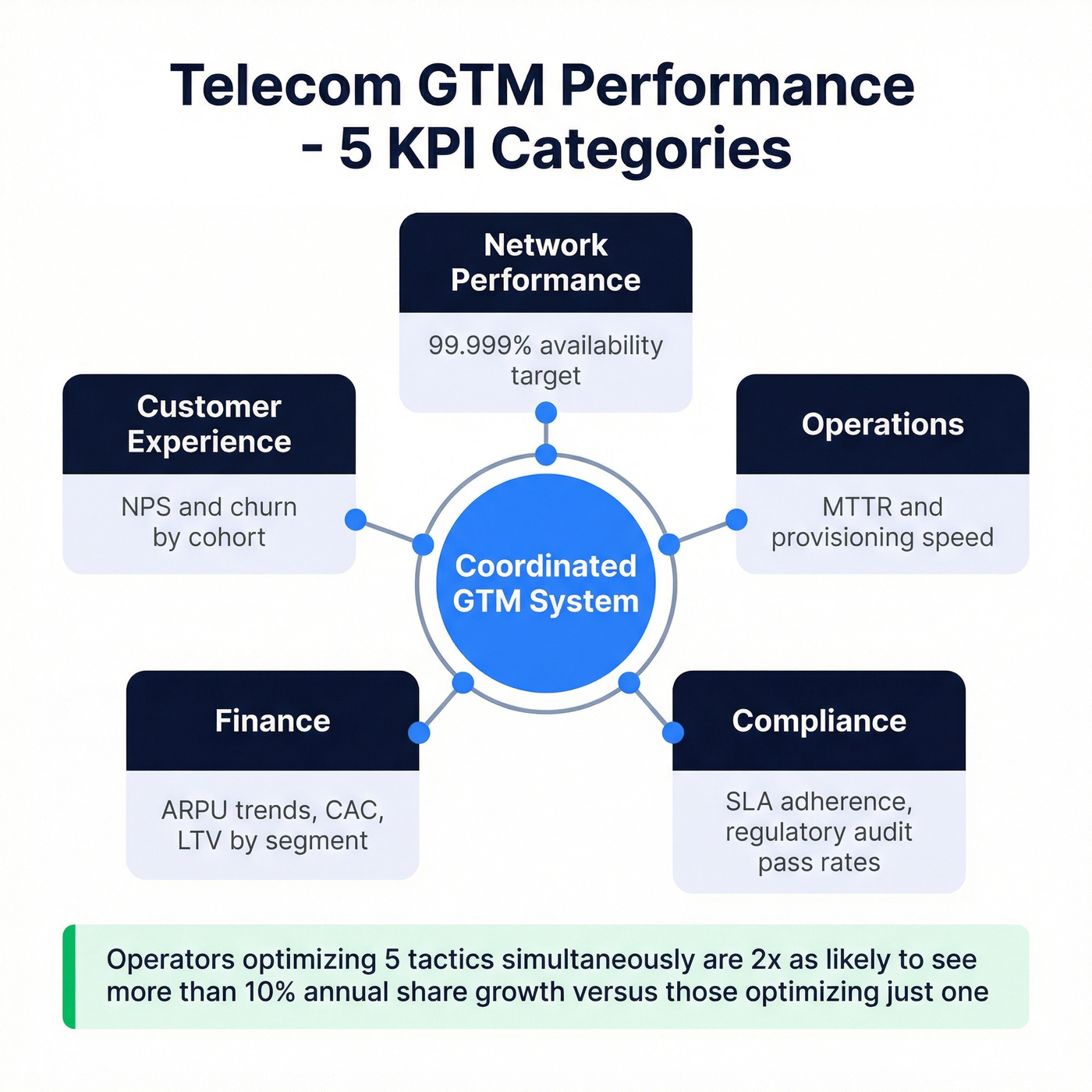

Five KPI categories matter, and most teams only track two of them well.

Network performance targets 99.999% availability. Operations tracks MTTR and provisioning speed. Compliance measures SLA adherence and regulatory audit pass rates. Finance watches ARPU trends, CAC, and LTV by segment. Customer experience monitors NPS and churn by cohort.

Operators optimizing five tactics simultaneously - sales tech, hyper-personalization, hybrid sales, marketplaces, e-commerce - are 2x as likely to see >10% annual share growth versus those optimizing just one. A strong go-to-market strategy for telecommunications companies in 2026 isn't a single motion. It's a coordinated system of motions measured against all five dimensions, with clear ownership for each.

FAQ

What makes telecom GTM different from SaaS GTM?

Regulatory burden, 6-12 month sales cycles, channel conflict affecting 43% of buyers, OSS/BSS integration complexity, and declining ARPU ($6.32 to $6.20 by 2029) create constraints that standard SaaS frameworks ignore entirely. The procurement process alone - with USAC registration, e911 compliance, and CPNI safeguards - adds months that SaaS companies never deal with.

Which telecom GTM motion has the highest growth potential?

API productization - projected at $6.7B by 2028 at 57.1% CAGR. Quick-win APIs like SIM swap detection and number verification generate revenue now through GSMA Open Gateway's 67-operator ecosystem.

How do I reach telecom decision-makers faster?

Use a B2B data platform with verified emails and direct dials refreshed weekly. Stale data is the silent killer of telecom outbound - when your cycle already runs half a year, you can't afford to waste the first month chasing bad numbers. Pair contact data with intent signals to prioritize in-market accounts.

How should telecom companies handle channel conflict?

Define clear account segmentation rules - enterprise direct, mid-market through partners - and enforce deal registration with 48-hour SLAs. Move from metallic tier programs to competency-based rewards that incentivize solution selling over volume. Most importantly, publish the rules so both your direct team and your partners know exactly where the lines are.

Running a channel-heavy telecom GTM? Your partners need pipeline too. Prospeo's 30+ search filters - buyer intent, technographics, headcount growth, funding - let you identify mid-market accounts ready for managed services bundles. At $0.01 per verified email, scaling outbound across direct and indirect motions costs 90% less than ZoomInfo.

Stop losing telecom deals to inertia. Start reaching buyers who are actually in-market.