Mid-Market Growth in 2026: What the Data Says and What Operators Are Actually Doing

A Reddit user tried to sell his lower-middle-market business four times over 30 years. Buyers walked every time - messy finances, too much owner dependence, no real sales process. He finally hired a CFO, built repeatable systems, and engaged an investment bank. Thirty interested parties. Six serious buyers. A PE exit.

That arc captures mid-market growth perfectly. The opportunity is enormous, but execution separates the winners from the stuck.

State of the Middle Market in 2026

The middle market isn't a niche. It's roughly 200,000 U.S. firms generating $10M-$1B in revenue, collectively producing over $10 trillion and employing 48 million people - about one-third of annual U.S. private-sector gross receipts. Yet it gets a fraction of the analyst coverage that enterprise and SMB segments receive.

The headline number looks strong: mid-market revenue growth accelerated to 11.7% at year-end 2025, per the National Center for the Middle Market's MMI. But zoom out to the full-year average and the picture gets more nuanced. The 2025 average was 10.7%, down from 12.4% in 2024. Growth is real, but it's decelerating.

Employment growth softened to 7.3%, which actually tells a positive story when you do the math. The NCMM defines productivity as revenue growth minus workforce growth, so mid-market firms are squeezing more output per employee, not just hiring their way to bigger numbers.

Citrin Cooperman's survey of 1,000 senior leaders at private companies fills in the profitability picture. 86% reported revenue growth versus the prior year, with 30% calling it significant. On the bottom line, 83% reported EBITDA growth. But here's the tension: 76% reported moderate-to-significant payroll cost increases, and 73% flagged rising direct costs. Growth is happening, but margins are under pressure from both sides.

| Metric | 2025 | Context |

|---|---|---|

| Revenue growth (NCMM full-year avg) | 10.7% | Down from 12.4% in 2024 |

| Employment growth | 7.3% | Softened - productivity rising |

| % reporting revenue growth (NCMM) | 84% | Down from 2024 |

| EBITDA growth (% of firms, Citrin Cooperman) | 83% | Strong despite cost pressure |

| Payroll cost pressure (moderate-to-significant) | 76% | Rising |

The firms that win in 2026 will grow revenue while holding headcount flat - the productivity math the NCMM is already tracking.

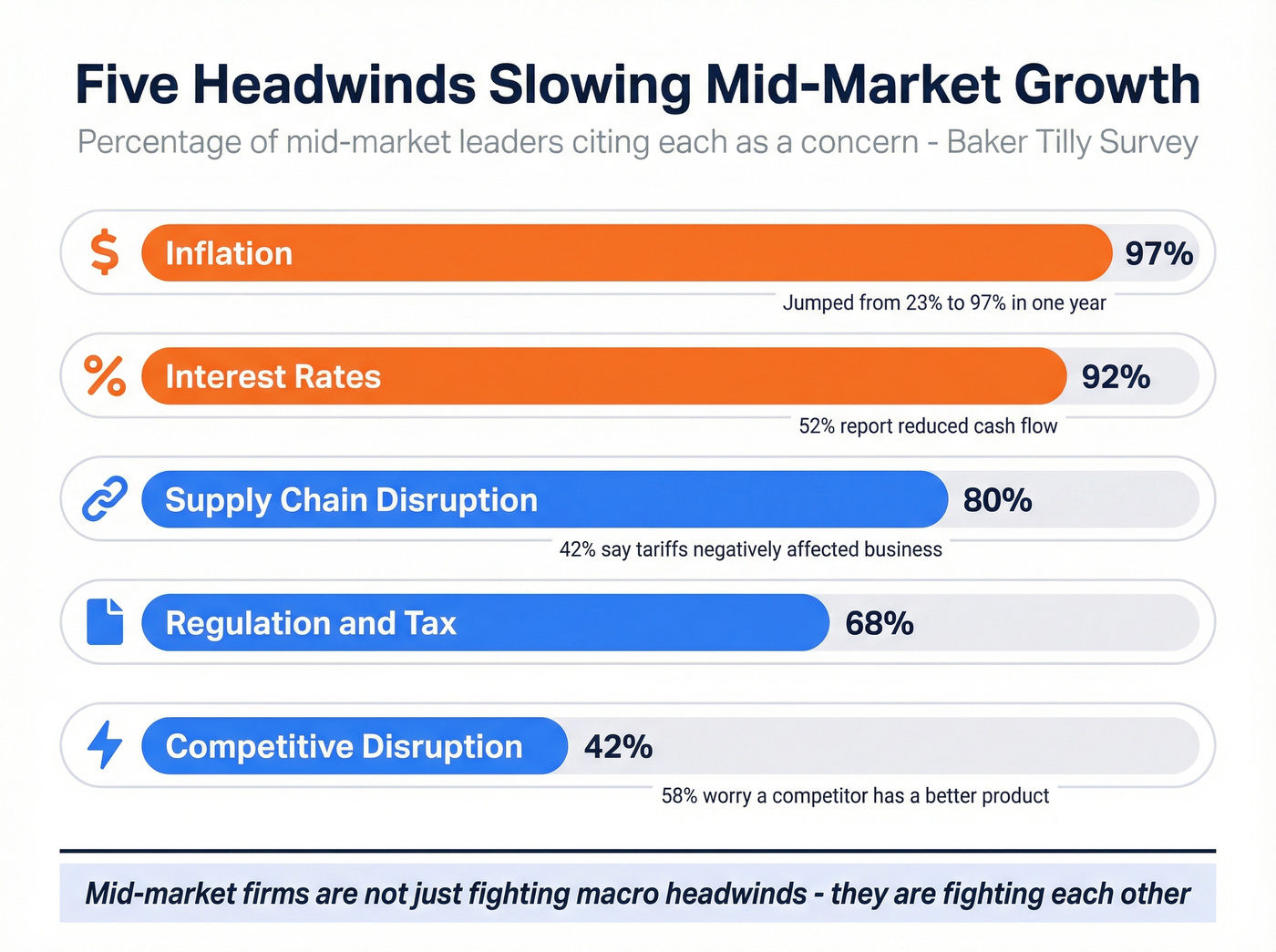

Five Headwinds Slowing Mid-Market Growth

Baker Tilly's mid-market survey paints a clear picture of what's keeping leaders up at night.

Inflation went from 23% to 97% of leaders citing it as a worsening concern in a single year. That's not a gradual shift - it's a sentiment earthquake. U.S. Treasury data pegged headline CPI at 3.0% in September 2025, which isn't runaway inflation by historical standards. But for mid-market operators already dealing with payroll and input cost increases, even moderate inflation compounds fast.

Interest rates are the second-biggest constraint, with 92% of mid-market leaders actively managing or preparing for increased costs. The downstream effects: reduced cash flow (52%), limited ability to invest in expansion or R&D (50%), and reduced consumer demand (42%). For firms that rely on debt to fund acquisitions or capital expenditures, this is the difference between doing a deal and sitting on the sidelines.

Supply chain disruption has moved from a crisis to a structural reality. 80% of leaders made or considered supply chain changes in 2025 due to tariffs and regulatory pressure, prioritizing resilience (41%), cost management (39%), and response speed (38%). Citizens' M&A Outlook found that 42% of companies said tariffs and trade policy negatively affected their business in 2025 - a concrete number that underscores the shift from theoretical risk to real P&L impact.

Regulation and tax concerns affect 68% of leaders. And 42% are on alert for competitive disruption - specifically, 58% worry a competitor has a better product or service, and 52% fear being undercut on pricing. Mid-market firms aren't just fighting macro headwinds. They're fighting each other.

Growth Strategy: M&A and PE

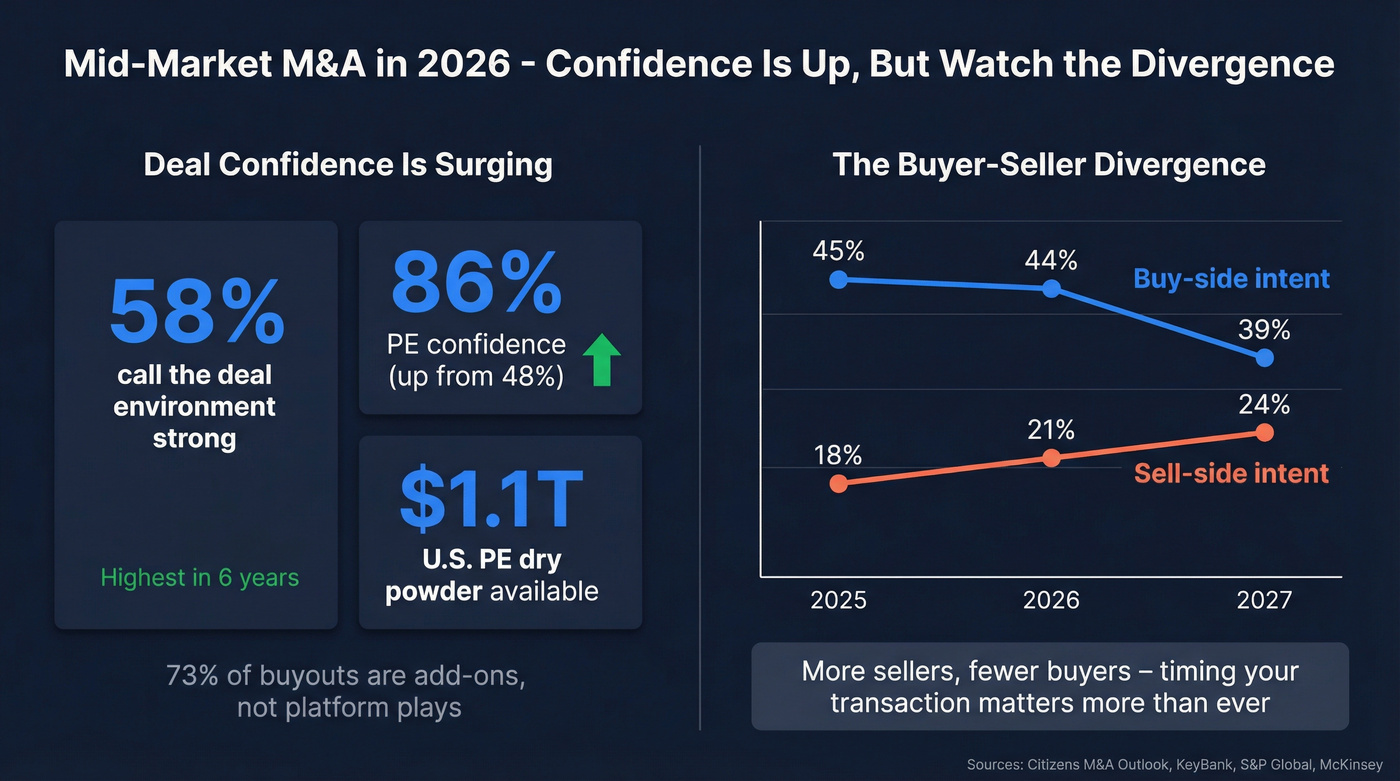

Deal Confidence Is Surging

Here's the thing about mid-market M&A in 2026: everyone's optimistic, but the optimism is lopsided. Citizens' 15th annual M&A Outlook found that 58% characterize the current deal environment as strong - the highest reading in six years. PE confidence jumped from 48% at the start of 2025 to 86% by year-end, and 90% of PE firms expect deal flow to remain steady or increase.

The capital is there. U.S. PE dry powder sits near $1.1 trillion, with $2.2 trillion globally per S&P Global Market Intelligence. In 2025, the U.S. PE market logged 9,000+ transactions totaling $1.2 trillion, with add-ons accounting for 73% of buyouts - a clear signal that PE firms are building through bolt-on acquisitions, not just platform plays. Globally, McKinsey pegged 2025 M&A deal value at $4.7 trillion, up 43% from $3.3 trillion.

But KeyBank's sentiment data introduces a wrinkle. Buy-side intent is declining: 45% of mid-market firms planned acquisitions by end of 2025, 44% in 2026, and 39% by 2027. Meanwhile, sell-side intent is rising from 18% to 24% over the same period. More sellers, fewer buyers. That divergence matters for anyone timing a transaction.

What Buyers Actually Want

We've seen too many mid-market deals fall apart in diligence. The obstacles aren't mysterious - KeyBank's survey ranks them: relationships (44% buy-side, 58% sell-side), financing availability (43%), cultural considerations (43% buy-side, 56% sell-side), integration and synergies (42%), and diligence bandwidth (39% buy-side, 42% sell-side).

RSM's dealmaking trends report is blunt about what separates closeable deals from time-wasters. Audit-ready financials and clean, organized data are nonnegotiable. Buyers now scrutinize technology readiness and whether the target has a clear AI strategy tied to efficiency or growth.

And here's the valuation kicker: McKinsey's analysis of "arena industries" - sectors where tech-enabled business models dominate - shows companies commanding an EV/EBITDA of 27.1x versus 16.5x for established companies. That's a 64% valuation premium for being AI-ready and tech-forward. If you're building toward an exit, your technology strategy isn't a nice-to-have. It's the single biggest lever on your multiple.

Growth Strategy: AI and Operations

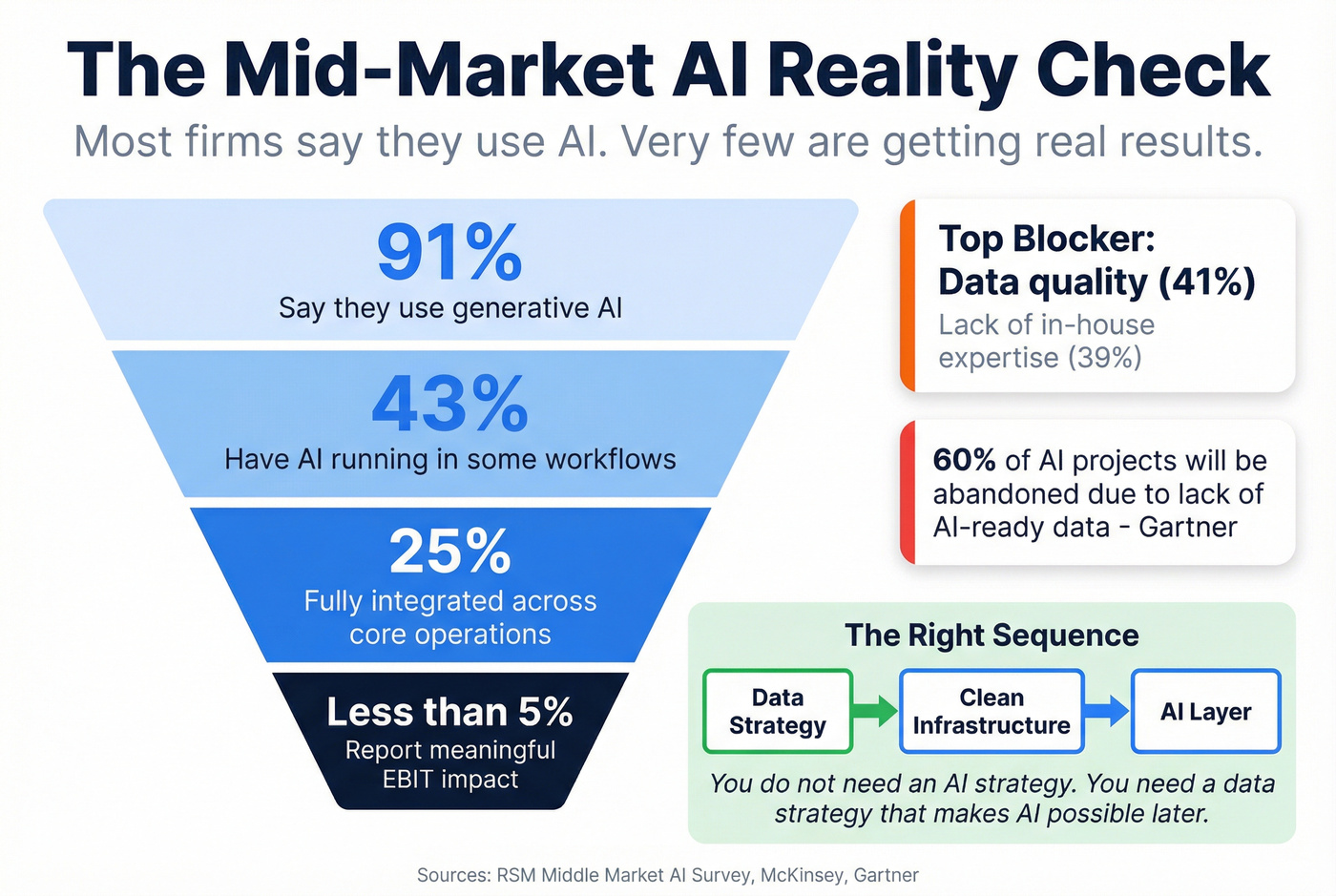

Stop calling it digital transformation. Call it data hygiene.

RSM's Middle Market AI Survey found that 91% of mid-market firms report using generative AI. Sounds impressive until you dig deeper: only 25% say genAI is fully integrated across core operations, 43% have it running in some workflows, and 92% experienced implementation challenges.

The top blocker? Data quality, cited by 41% of firms with implementation issues. Lack of in-house expertise came in at 39%. These aren't AI problems - they're infrastructure problems that existed before anyone typed a prompt into ChatGPT.

Across all company sizes, McKinsey found that nearly two-thirds of organizations haven't begun scaling AI across the enterprise. Only 39% report any EBIT impact at the enterprise level, and most say it's less than 5% of EBIT. Gartner estimates 60% of AI projects will be abandoned due to lack of AI-ready data.

Where AI is delivering value, the use cases are specific and measurable. The top applications are text generation and summarization (49%), workflow development (45%), and data analytics (44%). Time savings concentrate in IT projects (50%), data analytics (45%), and customer service (39%). In our experience, the companies that skip data hygiene and jump straight to AI platforms waste months before circling back to the fundamentals.

Black Clover is the proof case. This mid-market company implemented a data warehouse and custom reporting - not an AI platform. The outcome: 400% growth. The foundation was data visibility, not artificial intelligence.

Weidenhammer, a mid-market services firm, took a different approach: rolling out Microsoft Copilot to drive productivity and client growth. The key was starting with a specific use case, not trying to overhaul everything at once.

DSM Partnership's guidance for mid-market digital strategy starts with client journey mapping - identifying the "moments that matter" from discovery through buying, onboarding, and service. Build data ownership standards. Create a single secure view for teams. Then layer technology on top. The sequence matters: strategy before technology, always.

Let's be honest: most mid-market firms don't need an AI strategy. They need a data strategy that happens to make AI possible later. The 60% abandonment rate isn't an AI failure - it's a sequencing failure.

Mid-market firms growing revenue while holding headcount flat need data that works the first time. Prospeo delivers 98% verified emails and 125M+ direct dials refreshed every 7 days - so your team books more meetings without adding reps.

Squeeze more pipeline per rep with data that actually connects.

International Expansion and Talent

Building a Market Expansion Plan

Grote Company, a food processing equipment manufacturer, now generates nearly 50% of its revenue from overseas markets. That didn't happen by accident - it happened through decades of building local distribution networks and technical expertise in markets where food processing standards differ significantly from U.S. norms. A deliberate market expansion plan - identifying target geographies, building local partnerships, and adapting to regional regulations - was the backbone of that transformation.

For mid-market firms that don't have decades to build international operations organically, acquisition-led entry is the faster path. Acquiring an established overseas entity gives you local market knowledge, existing customer relationships, and regulatory familiarity on day one. Eide Bailly's research confirms the appetite: 56% of mid-market firms plan to expand their offerings, and 37% plan to expand to new geographic regions.

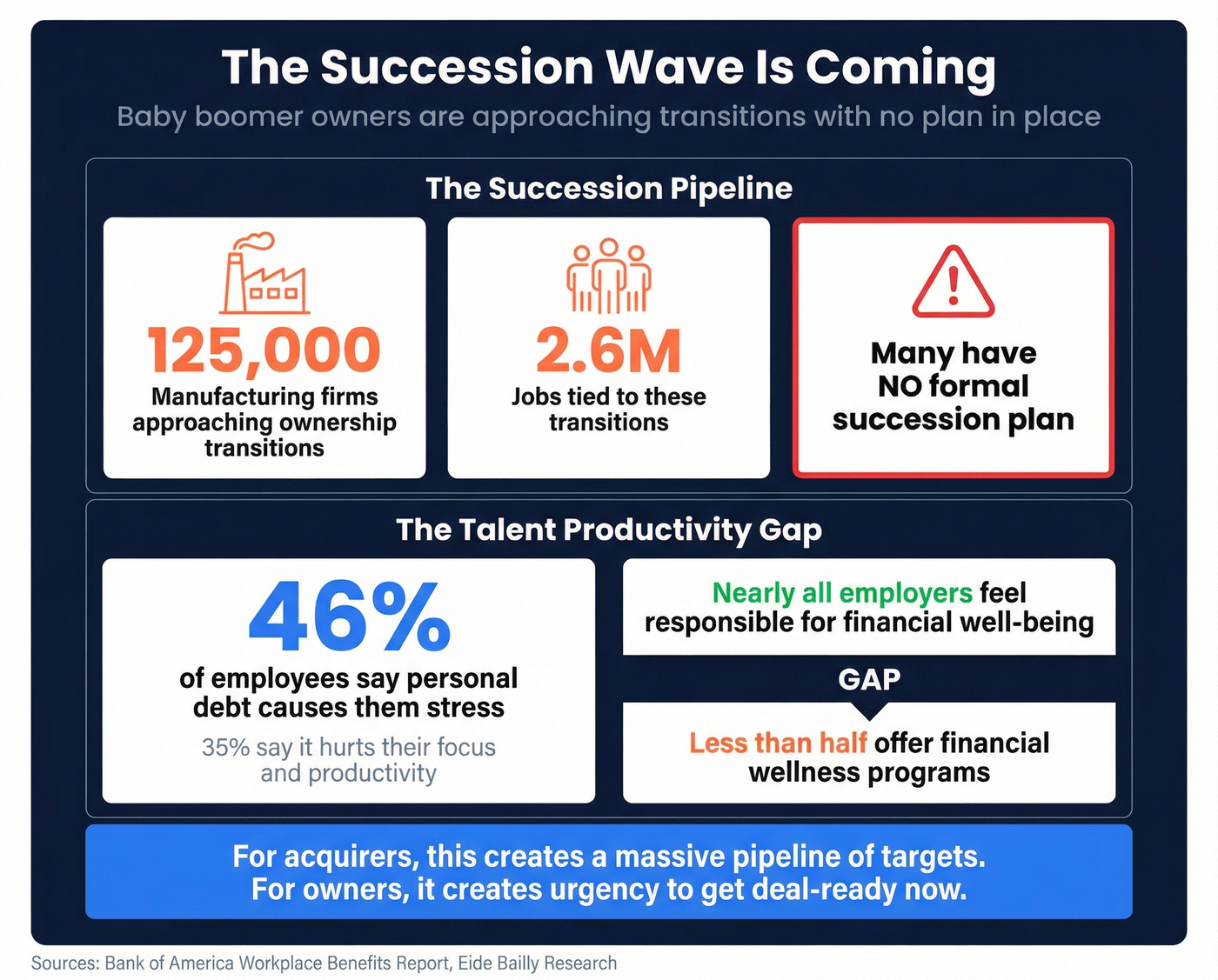

The Talent and Succession Gap

The talent challenge in the middle market isn't just about hiring - it's about keeping people productive and planning for leadership transitions. Bank of America's Workplace Benefits Report found that 46% of employees say personal debt causes them stress, and 35% say it interferes with their focus and productivity. Nearly all employers feel responsible for employees' financial well-being, yet less than half offer financial wellness programs. That's a gap mid-market firms can close cheaply, and the productivity upside is meaningful.

The succession wave is the bigger structural issue. Baby boomer owners represent approximately 125,000 manufacturing firms and 2.6 million jobs approaching ownership transitions. Many have no formal succession plan. For acquirers, this creates a massive pipeline of potential targets. For the owners themselves, it creates urgency to get deal-ready now.

Readiness Framework for Scaling

Eide Bailly's framework distills the path into four inflection points:

- Visibility before growth. You can't scale what you can't measure. Real-time, trusted data is the prerequisite - and over 50% of business leaders cite access to accurate, timely data as their biggest challenge.

- Strategy before technology. Digital tools amplify a clear strategy. They don't replace one. Map your customer journey and data governance before buying platforms.

- Readiness before investment. Whether you're raising capital, pursuing M&A, or investing in new markets, operational readiness determines whether the investment compounds or combusts.

- Continuity before transition. Succession planning, key-person risk reduction, and process documentation aren't exit activities - they're growth activities that happen to also make you sellable.

Black Clover's 400% growth story maps directly to this framework. They started with visibility through a data warehouse and custom reporting, built strategy around what the data revealed, and invested from a position of operational clarity. No AI buzzwords required. The framework sounds simple. The execution isn't. But the sequence is what matters - skip a step and you're building on sand.

Building Pipeline

Every growth strategy in this guide - M&A, AI, international expansion - eventually requires pipeline. New customers, new partners, new acquisition targets. Mid-market firms face a structural gap here: too big for scrappy manual prospecting, too small to justify $15-40K/year data contracts from legacy providers. One r/fatFIRE thread captured the frustration perfectly - deal sourcing through traditional marketplaces was widely panned as ineffective for mid-market operators.

Look, we've watched teams burn weeks trying to build target lists from stale databases and bounced emails. Prospeo closes that gap with 300M+ professional profiles, 98% verified email accuracy, and 125M+ verified mobile numbers on a 7-day refresh cycle. The search interface offers 30+ filters including buyer intent signals tracking 15,000+ topics, headcount growth, funding, and technographics. Filter by company revenue and headcount to target mid-market firms specifically, then export verified contacts directly to your CRM or sequencer. At roughly $0.01 per email - 90% cheaper than legacy providers - with no annual contracts and a free tier to test, it's the obvious starting point for mid-market sales teams that need enterprise-grade data without enterprise overhead.

41% of mid-market firms say data quality is their top AI and operations blocker. Prospeo's 5-step verification, 92% enrichment match rate, and 50+ data points per contact fix the infrastructure problem before it kills your growth strategy.

Stop blaming AI adoption - fix your data first.

Exit Readiness: Lessons From the Field

That Reddit owner-operator story from the intro deserves a deeper look. Four failed exits over 30 years. The pattern was consistent: buyers would engage, start diligence, and walk away. Messy finances that couldn't survive scrutiny, a business too dependent on the owner, and no competitive process to create urgency.

The fixes were equally predictable. Hiring a CFO was the single biggest improvement - it professionalized the financials and gave buyers confidence in the numbers. Building a real sales process and making key hires reduced owner-dependence risk. Engaging an investment bank created the competitive dynamic that had been missing.

RSM's dealmaking guidance echoes every lesson from that story. Audit-ready financials are nonnegotiable. A data-supported value-creation strategy shows buyers where the upside lives. Technology readiness demonstrates the business can scale beyond its current state.

KeyBank's data shows sell-side intent rising from 18% to 24% by 2027. More mid-market owners are moving toward exits. But with buy-side intent declining over the same period, competitive dynamics will shift toward buyers. Operators planning an exit in the next 18-24 months should be getting deal-ready now, not later.

The exit readiness checklist that emerges from the data:

- Audit-ready financials with a real CFO or fractional CFO in place

- Reduced owner dependence through documented processes and key hires

- Clean CRM and customer data that can survive diligence scrutiny

- A data-supported value-creation narrative, not just "we're growing"

- Technology stack that demonstrates scalability

- Competitive sale process managed by professionals, not the founder

Skip this section if you're not within three years of a potential exit. But if you are, every month you delay preparation is a month of leverage you're handing to the buyer.

FAQ

What qualifies as a mid-market company?

Mid-market companies generate between $10M and $1B in annual revenue. There are roughly 200,000 of these firms in the U.S., collectively producing over $10 trillion in annual revenue and employing approximately 48 million people - about one-third of private-sector gross receipts.

What's the average revenue growth rate?

The NCMM's Middle Market Indicator reported 11.7% revenue growth at year-end 2025, with a full-year average of 10.7% - down from 12.4% in 2024. Growth remains strong but is decelerating, with 84% of middle-market companies reporting positive revenue gains.

Is 2026 a good year for mid-market M&A?

Yes - 58% of executives describe the deal environment as strong, PE confidence sits at 86%, and $1.1 trillion in U.S. dry powder awaits deployment. But buy-side intent is declining toward 2027 (45% to 39%) while sell-side intent rises (18% to 24%), so timing matters.

Where should mid-market firms start with AI?

Data hygiene first. 41% of firms cite data quality as the top AI implementation blocker, and Gartner estimates 60% of AI projects get abandoned due to lack of AI-ready data. Start with a data warehouse and clean reporting infrastructure before purchasing any AI platform.

How do mid-market sales teams build pipeline affordably?

Self-serve B2B data platforms now offer 300M+ profiles with 98% email accuracy at roughly $0.01 per email - no contracts or $30K annual commitments required. Filter by buyer intent, headcount growth, and revenue to target mid-market prospects specifically, then export verified contacts directly to your CRM.