Deal Flow Management: Benchmarks, Mistakes, and Tools That Work

A RevOps lead at a growth-stage PE fund told us last quarter that their "deal flow management system" was a shared Google Sheet with 400 rows, color-coded by one associate who'd just put in her two weeks. That's not an edge case. An estimated 80% of corporate development teams still operate on spreadsheets, shared drives, and email threads. Meanwhile, PE conversion rates have dropped to 25% with a median time-to-close of 231 days. If your process can't survive one person leaving, it isn't a process - it's a liability.

What You Need (Quick Version)

The average VC reviews 101 opportunities per investment. In PE, the median time-to-close is 231 days. If you're still managing this in spreadsheets, you need two things: a dedicated pipeline tool and a reliable contact data source.

Here's the short version by team type:

- Institutional PE with 50+ people: DealCloud for end-to-end deal management.

- Budget-conscious or early-stage funds: monday CRM or 4Degrees for pipeline tracking.

What Is Deal Flow Management?

Deal flow is the stream of investment opportunities reaching your desk - the raw material your fund runs on. Deal flow management is the system you use to track, evaluate, and advance those opportunities from first touch to close. Process, people, tools.

The sourcing mechanics diverge sharply by fund type. VC deal flow skews toward proprietary sourcing: 30% of venture investments begin with VCs reaching out directly to founders. PE deal flow leans more on intermediaries - investment banks, brokers, and formal auction processes. Corp dev teams sit somewhere in between, often managing long relationship arcs with targets they won't acquire for years.

The distinction between proprietary and intermediated deals matters more than most teams acknowledge. Proprietary deals face less competition and typically close at better valuations, but they require active outreach infrastructure: verified contact data, relationship tracking, and a sourcing engine that doesn't depend on bankers sending you teasers.

Deal Flow by the Numbers

Here's the thing: most teams obsess over pipeline tools while ignoring the data that proves their funnel is broken.

PE benchmarks deserve top billing because they're the most brutal. That 231-day median time-to-close and 25% conversion rate mean three out of four deals a PE team pursues go nowhere - burning months of analyst time each. On the VC side, the numbers are different but equally unforgiving.

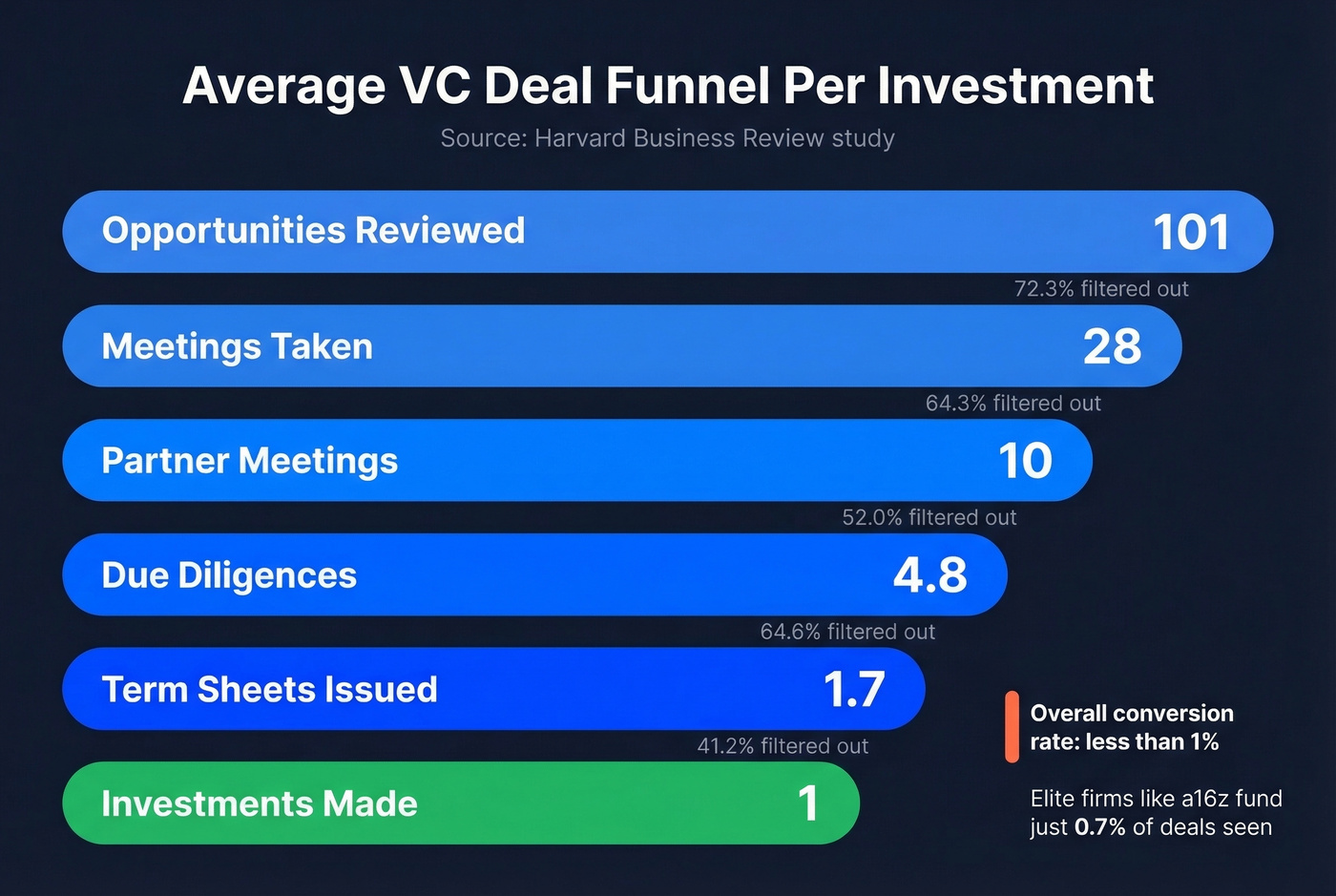

A Harvard Business Review study tracked the average VC funnel per investment:

| Funnel Stage | Average Count |

|---|---|

| Opportunities reviewed | 101 |

| Meetings taken | 28 |

| Partner meetings | 10 |

| Due diligences | 4.8 |

| Term sheets issued | 1.7 |

| Investments made | 1 |

That's a 1% conversion rate from top-of-funnel to funded deal. Elite firms are even more selective - Andreessen Horowitz funds 0.7% of deals they see, and GREE Ventures funds 0.5%. The average VC deal takes 83 days to close, with 118+ hours spent on due diligence alone.

These numbers are the reason spreadsheet-based systems collapse. When you're juggling 101 opportunities per investment across multiple partners, a shared Google Sheet doesn't provide the relationship context, stage tracking, or follow-up automation you need to avoid dropping deals.

When you're screening 101 opportunities per investment, one bounced email can cost you a proprietary deal. Prospeo delivers 98% email accuracy across 300M+ professional profiles - refreshed every 7 days, not every 6 weeks. Find verified emails and direct dials for founders, CEOs, and portfolio company executives at $0.01 per lead.

Stop losing deals to stale contact data. Start sourcing with verified emails.

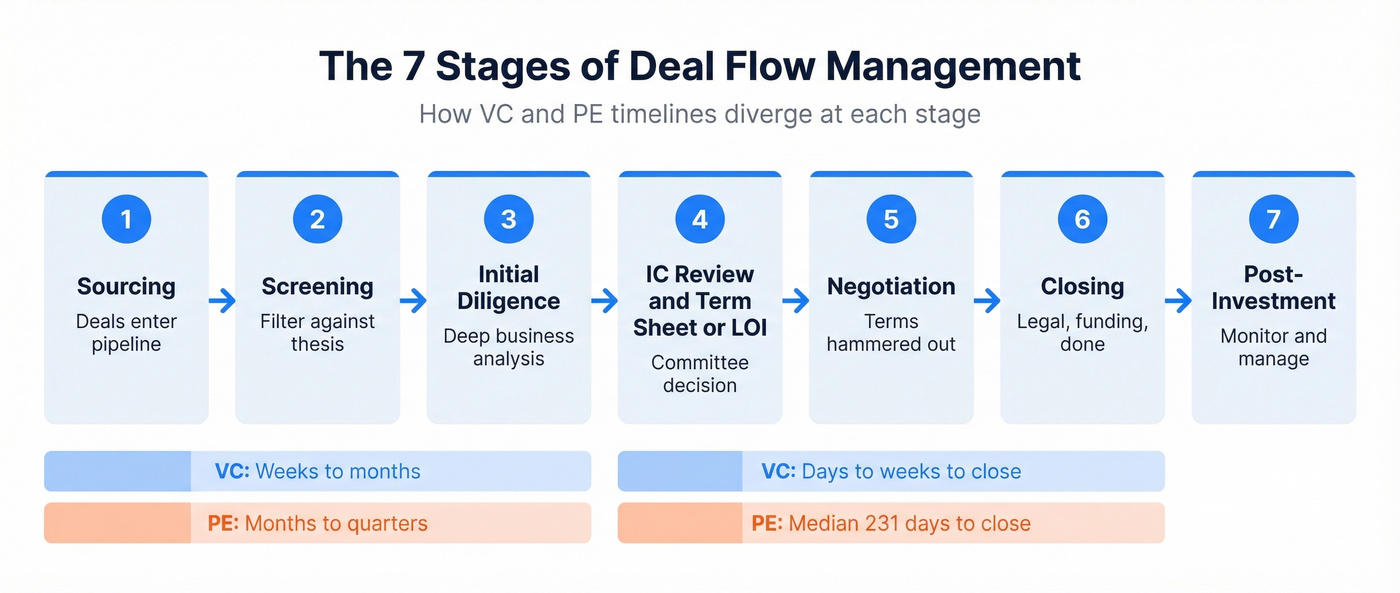

The 7 Stages of the Deal Flow Process

Carta's framework breaks the investment pipeline into seven stages. We've enriched it with VC vs. PE distinctions that matter in practice.

Sourcing and Screening

Stage 1 - Sourcing. This is where deals enter your pipeline. VC teams source through founder networks, demo days, warm intros, and direct outreach. PE teams rely more on investment banks, brokers, and proprietary relationships built over years. The quality of your sourcing determines everything downstream.

Stage 2 - Screening and evaluation. You're filtering against your investment thesis: sector focus, stage, deal size, geography. Most teams reject the majority of inbound at this stage.

Diligence and IC Review

Stage 3 - Initial diligence. Deeper analysis of the business model, financials, market, and team. VC teams might spend a few weeks here; PE teams can spend months, especially for complex carve-outs.

Stage 4 - Investment committee and term sheet or LOI. This is where VC and PE diverge most sharply. VC firms issue term sheets - relatively lightweight documents outlining valuation and key terms. PE firms issue letters of intent, which kick off formal legal and financial diligence that can run for months.

Negotiation Through Post-Investment

Stages 5-6 - Negotiation, legal diligence, and closing. Lawyers get involved, deal terms get hammered out, and money moves. For VC, closing can happen in weeks. For PE, escrow, regulatory approvals, and debt financing stretch the timeline significantly.

Stage 7 - Post-investment monitoring. The deal isn't done at close. VC firms track portfolio company metrics and board participation. PE firms manage operational improvements, add-on acquisitions, and exit planning. This is where many teams drop the ball - they optimize for deal-making but under-invest in portfolio management infrastructure.

Five Mistakes That Kill Returns

We've seen these patterns destroy returns across fund types. Each one is fixable, but only if you name it.

1. Network isolation. Funds that source exclusively through their own network miss deals. The best firms maintain active co-investor relationships and cross-pollinate deal flow. One input channel means you're exposed.

2. Weak follow-up cadence. A founder you met at a conference six months ago just raised a Series A - and you didn't know because nobody followed up. This is partly a process problem and partly a data problem. Contact information decays fast: people change roles, switch emails, move companies. Most teams don't think about data freshness until their emails start bouncing.

3. Ignoring risk signals. Continuous risk monitoring isn't optional. Teams that only assess risk during initial diligence miss deteriorating fundamentals, management changes, and market shifts that emerge between term sheet and close.

4. Scattered sourcing processes. Too many channels, not aligned to thesis. When inbound comes through email, a CRM, a shared inbox, and three partners' personal networks, deals fall through cracks. Centralize inbound or accept that you'll lose opportunities.

5. Poor integration planning. PE deal teams consistently underestimate post-close integration complexity. Misaligned management incentives, inadequate operational improvement plans, and cultural misfit between acquirer and target are the three killers, and the fix starts during diligence, not after close.

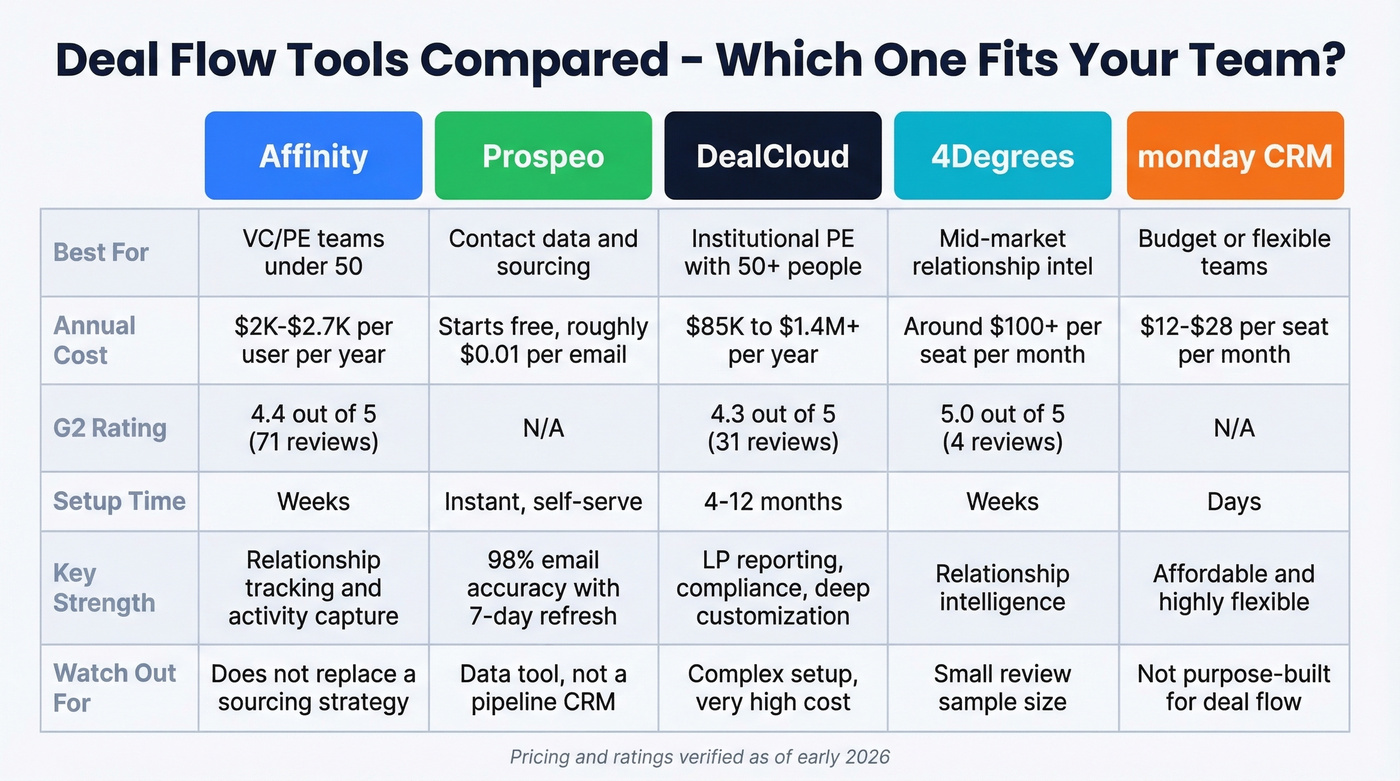

Deal Flow Tools Compared

Let's be honest about the dirty secret of investment pipeline software: most tools solve the tracking problem but ignore the upstream data problem. You can have the best CRM in the world, but if you can't get a verified email for the CEO of your target company, your sourcing engine is broken.

| Tool | Best For | Pricing | G2 Rating | Implementation |

|---|---|---|---|---|

| Affinity | VC/PE teams under 50 | $2K-$2.7K/user/yr | 4.4/5 (71 reviews) | Weeks |

| Prospeo | Contact data sourcing | ~$0.01/email; free tier | - | Self-serve, instant |

| DealCloud | Institutional PE, 50+ | $85K-$1.4M+/yr | 4.3/5 (31 reviews) | 4-12 months |

| 4Degrees | Mid-market rel. intel | ~$100/mo+ per seat | 5.0/5 (4 reviews) | Weeks |

| monday CRM | Budget / flexible teams | $12-$28/seat/mo | - | Days |

Affinity - Relationship-Driven VC/PE

If you're a sub-50-person fund moving off spreadsheets, start here. Affinity automates activity capture, scores relationships, and gets your pipeline live in weeks, not months. Pricing runs $2,000/user/year for Essential, $2,300 for Scale, and $2,700 for Advanced, with an Enterprise tier for custom needs. The adoption rate Affinity reports - above 96% - tracks with what we've seen in practice. Tools that are easy to use actually get used, and Affinity's ease-of-use score of 8.7 on G2 is best-in-class for this category.

In our experience, the biggest risk with Affinity isn't the tool itself but the assumption that it replaces a sourcing strategy. It tracks relationships beautifully. It doesn't find new ones for you.

Skip this if you're a 200-person institutional PE firm that needs deep compliance workflows, custom LP reporting, and multi-entity deal tracking. Affinity is built for speed, not regulatory complexity.

Prospeo - Deal Sourcing Data

Pipeline tools manage your deals. Prospeo fills the top of the funnel. The database covers 300M+ professional profiles with 98% email accuracy and 125M+ verified mobile numbers on a 7-day refresh cycle - the industry average is six weeks. For deal sourcing, where you're reaching out to founders, CFOs, and advisors who change roles frequently, freshness matters more than database size. It starts free at 75 emails/month (plus 100 Chrome extension credits/month), scales at roughly $0.01/email, and integrates with Salesforce and HubSpot.

DealCloud - Institutional PE

At an average annual cost of $505K, DealCloud isn't a tool you evaluate casually. The full range runs $85K-$1.4M+/year, and implementation takes 4-12 months. So why do large PE firms pay it? Because nothing else handles LP reporting, compliance workflows, multi-entity deal tracking, and deep customization at the same level. G2 reviewers consistently flag setup complexity as the main drawback - "initial setup can be time-consuming and challenging" is a recurring theme - but G2's head-to-head scoring also puts DealCloud's support quality at 9.4 out of 10. It earns its keep once you're through the implementation gauntlet.

One negotiation tip: DealCloud tends to discount services more readily than subscription fees, so push on implementation costs. (If you want a structured way to do that, see our guide on anchor in negotiation.)

4Degrees - Mid-Market Relationship Intelligence

4Degrees sits between Affinity and DealCloud in both price and complexity. It maps who in your firm knows whom and surfaces warm paths to deal targets. Pricing starts around $100/month per seat, though actual deployment costs scale with team size and are quote-based. The 5.0/5 rating is based on only 4 reviews - too small a sample to trust. Worth evaluating if Affinity feels too lightweight but DealCloud is overkill.

monday CRM - Budget Flexibility

monday CRM isn't built for PE or VC specifically, but it's highly customizable and starts at $12-$28/seat/month with a minimum of 3 seats. For early-stage funds or corp dev teams that need basic pipeline tracking without committing to a vertical-specific tool, it's a pragmatic starting point. You'll outgrow it. But it buys you time while you figure out what you actually need.

Weak follow-up cadence is the second-biggest deal flow killer - and bad data makes it worse. People change roles, emails bounce, and your carefully built pipeline goes cold. Prospeo's 7-day refresh cycle and 125M+ verified mobile numbers mean your outreach actually reaches decision-makers, whether you're chasing a founder or a target company's CFO.

Your deal flow is only as strong as the data behind it.

How to Choose the Right Tool

The right stack depends on three variables: team size, fund type, and budget.

| Team Size | Fund Type | Pipeline Tool | Contact Data |

|---|---|---|---|

| Under 10 | VC / early PE | Affinity Essential | Prospeo free tier |

| 10-50 | Growth PE / corp dev | Affinity Scale or 4Degrees | Prospeo paid |

| 50+ | Institutional PE | DealCloud | DealCloud enrichment + Prospeo |

| Any, budget under $500/mo | Any | monday CRM | Prospeo free tier |

Don't over-index on features during evaluation. The best deal flow tool is the one your team actually uses. We've seen $500K/year DealCloud deployments where teams still revert to spreadsheets because implementation drags and nobody gets trained properly. If your fund's average check size is under seven figures and your team is under 20 people, you almost certainly don't need enterprise-grade software. Affinity plus a solid data enrichment layer will get you 90% of the way there at a fraction of the cost.

FAQ

What's the difference between deal flow and deal flow management?

Deal flow is the stream of investment opportunities reaching your firm. Deal flow management is the system - process, tools, and people - you use to track and advance those opportunities through your pipeline. One is the input; the other is the operating system that determines conversion rates.

When should a fund move from spreadsheets to dedicated software?

When multiple partners share deal coverage and inbound volume exceeds what one person can reliably track - typically around 50+ active opportunities. If you've ever lost a deal because nobody followed up, you're already past the threshold. Affinity or monday CRM can get you live in days, not months.

How do VC and PE deal flow processes differ?

VC deals close in 83 days on average, use term sheets, and rely on direct founder outreach. PE deals take a median 231 days, use LOIs, and involve intermediaries and formal auctions. VC teams need speed and relationship tracking; PE teams need compliance workflows and multi-stage diligence infrastructure.