Fintech Go-to-Market Strategy: The Data-Backed Framework for 2026

A founder on r/fintech shared a story that stuck with us. Twelve weeks in, six paying clients, roughly $20K ARR. Strong early traction from door-to-door outbound. Then he paused sales for six weeks to polish the product. Growth flatlined. That's not a tactics problem - a solid go-to-market strategy for fintech would've prevented it entirely. He didn't need seven GTM steps. He needed three decisions.

Three Decisions That Define Your Fintech GTM

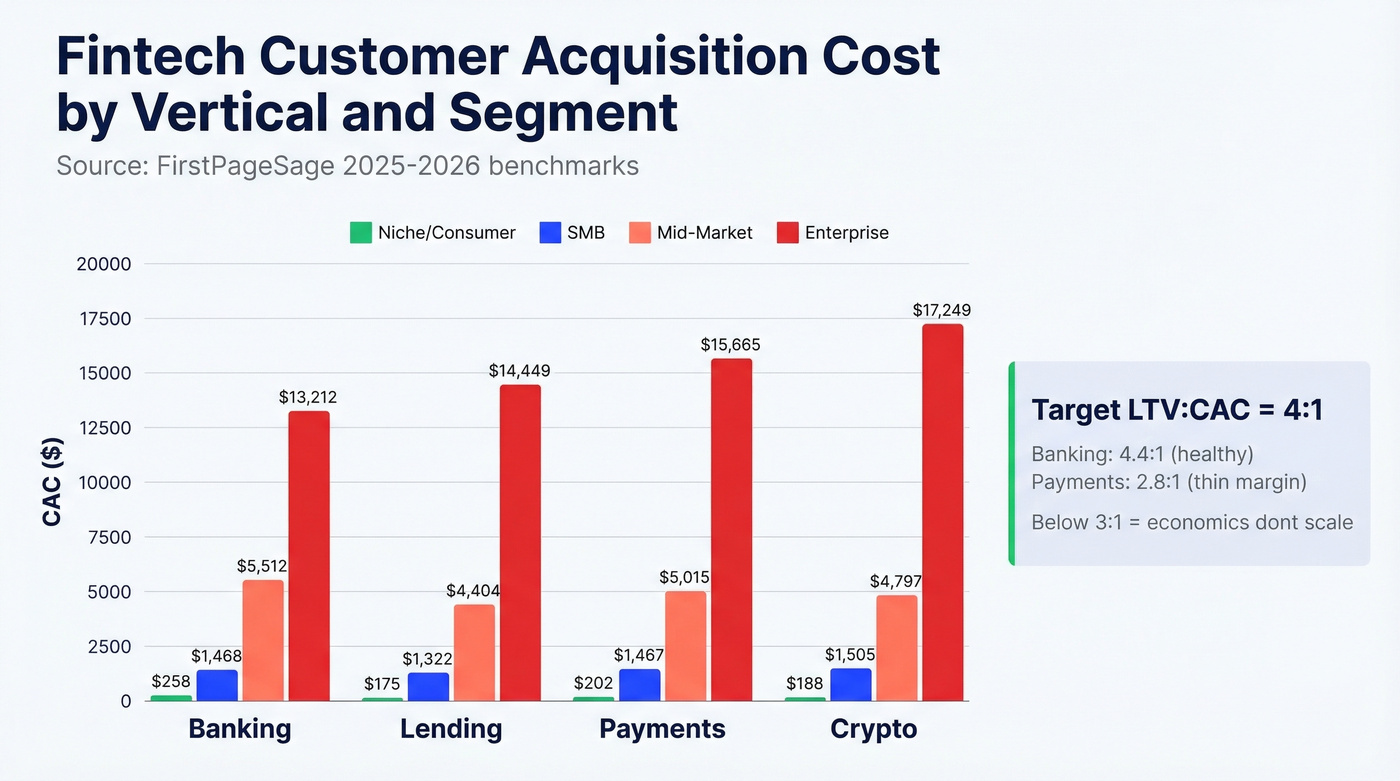

- Who - Your ICP defines your CAC. Acquiring a niche banking customer costs $258. An enterprise one costs $13,212. Same vertical, 50x difference.

- How - Your ACV determines your motion. PLG under $10K, sales-led above $25K, hybrid in between.

- What it costs - Channel CAC ranges from $647 (SEO) to $4,664 (ABM).

Everything else is execution.

Define Your ICP and Know Your CAC

Your ICP doesn't just shape messaging - it determines whether you spend $175 or $17,249 per customer. Here's the breakdown from FirstPageSage:

| Vertical | Niche/Consumer | SMB | Mid-Market | Enterprise |

|---|---|---|---|---|

| Banking | $258 | $1,468 | $5,512 | $13,212 |

| Lending | $175 | $1,322 | $4,404 | $14,449 |

| Payments | $202 | $1,467 | $5,015 | $15,665 |

| Crypto | $188 | $1,505 | $4,797 | $17,249 |

Banking averages a 4.4:1 LTV:CAC - healthy. Payment processing sits at 2.8:1, which means razor-thin margin for error. The ideal target is 4:1. Below 3:1, your acquisition economics don't scale.

Most fintechs underestimate their true CAC by 40-60% because they exclude onboarding, compliance overhead, and sales engineering time. If your spreadsheet only counts ad spend and SDR salaries, you're lying to yourself.

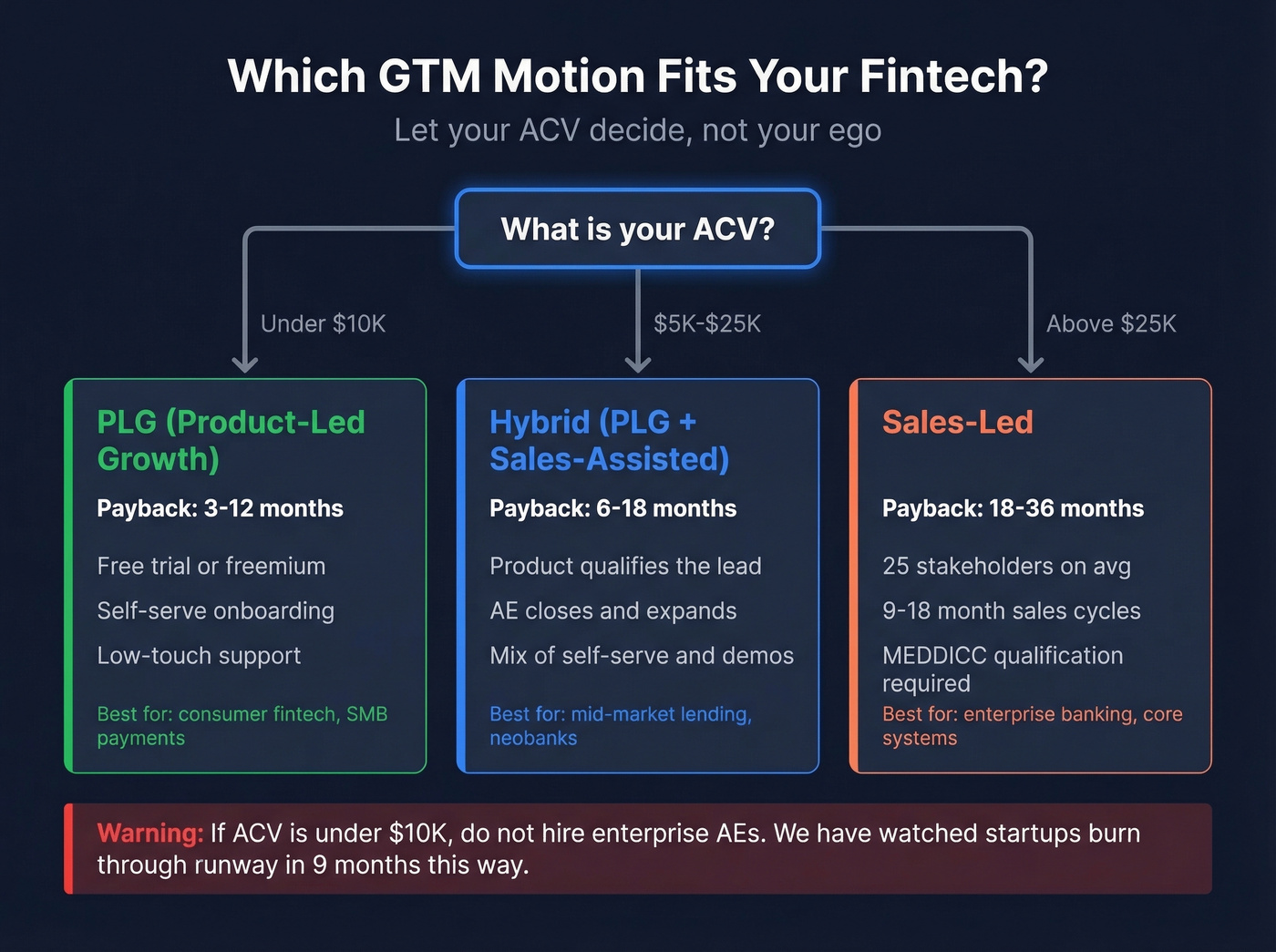

Choose Your GTM Motion

ACV is the clearest signal for which motion to run.

| ACV | Motion | Payback Period |

|---|---|---|

| Under $10K | PLG | 3-12 months |

| $5K-$25K | Hybrid (PLG + sales-assisted) | 6-18 months |

| Above $25K | Sales-led | 18-36 months |

Selling into banks or large FIs? B2B buying committees have grown to 25 stakeholders, up from 16 in 2017, which means enterprise fintech sales cycles run 9-18 months and a single missed stakeholder with veto power can kill a deal you've been working for a year. MEDDICC isn't optional here.

Here's the thing: if your ACV sits below $10K, you almost certainly don't need a sales-led motion. We've watched early-stage fintechs hire enterprise AEs at $50K ACV targets and burn through runway in nine months. PLG or bust until the deal sizes justify the headcount.

Pick Your Channels

Not all channels are equal. The CAC gaps are dramatic:

| Channel | B2B CAC | B2C CAC |

|---|---|---|

| SEO / Thought Leadership | $647 | $298 |

| Social Media | $658 | $212 |

| PPC / SEM | $802 | $290 |

| Content Marketing | $1,254 | $890 |

| ABM | $4,664 | - |

Partnerships and community-led distribution outperform paid ad funnels in fintech. Reddit practitioners consistently confirm this. The Apple Card partnership reached 12 million users - distribution you can't buy with PPC. Embedded finance works the same lever at a different scale: Unit's ecosystem now holds $1.3B in deposits, up 65% year over year.

In our experience, fintechs that lead with SEO and partnerships before touching paid ads build more sustainable pipelines. Paid comes after organic traction, not before it.

Fintech CAC explodes when outbound bounces. Prospeo's 98% email accuracy and 7-day data refresh keep your domain reputation clean while you prospect into banks and FIs. 30+ filters to target by industry, headcount, funding, and job title - at $0.01 per email.

Stop burning CAC on contacts who left three months ago.

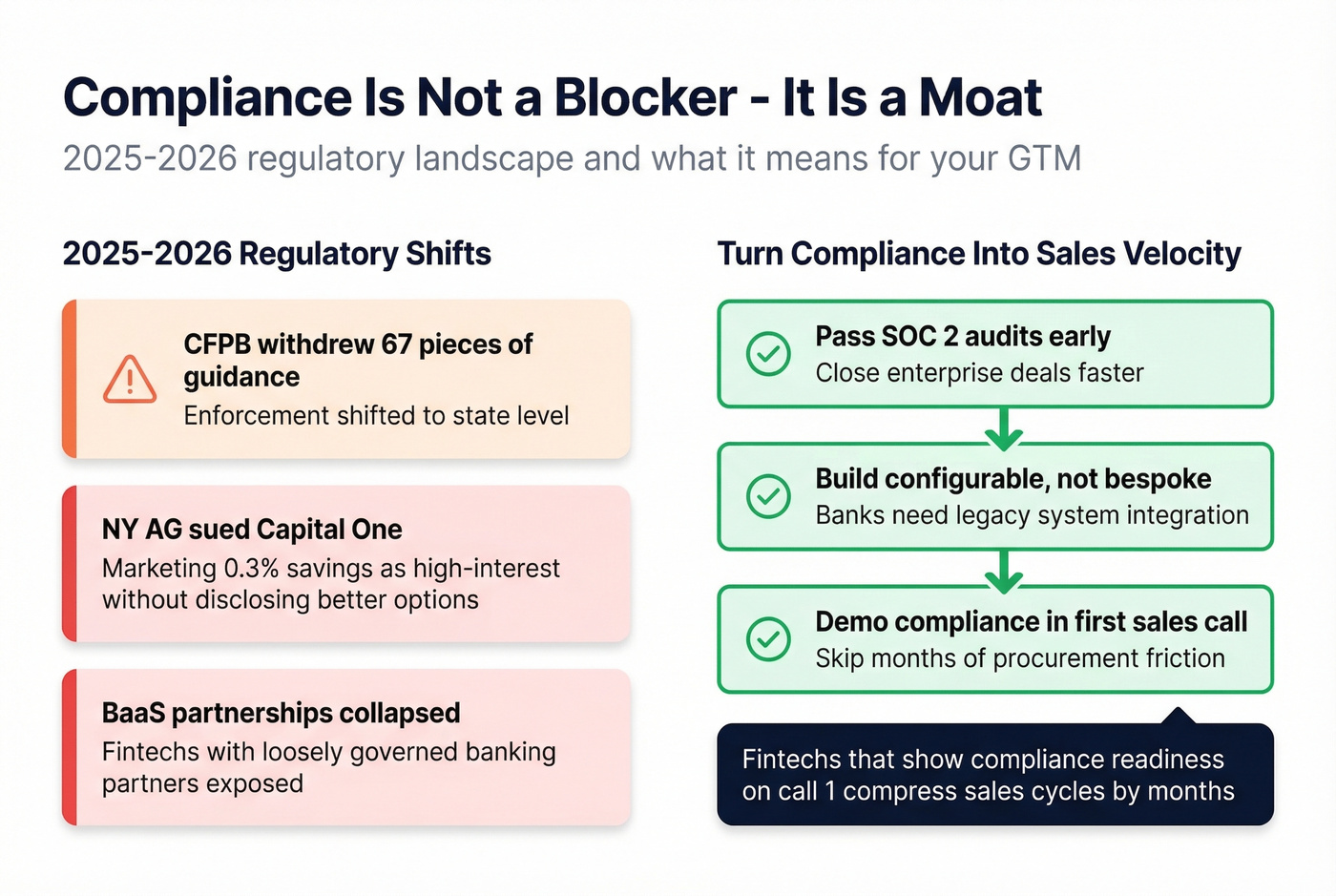

Build a GTM That Compliance Teams Approve

Most founders treat compliance as a blocker. The smart ones treat it as a moat.

The CFPB withdrew 67 pieces of guidance in mid-2025, creating real uncertainty about how certain issues will be interpreted and enforced going forward. Enforcement shifted to the states - the New York AG sued Capital One for marketing a "high-interest" savings account at 0.3% without disclosing better options. BaaS partnerships collapsed across several U.S. providers in late 2024, exposing fintechs with loosely governed banking partners.

Let's be honest: fintechs that pass security reviews and SOC 2 audits close enterprise deals faster. Banks won't adopt products that don't integrate with legacy systems - build configurable, not bespoke. If you can demonstrate compliance readiness in the first sales call, you skip months of procurement friction. Compliance isn't a cost center. It's a sales accelerator.

Build Your Prospect List

Fintech's prospect universe is narrow. If you're selling into banks or credit unions, you're targeting a finite set of institutions with specific decision-makers, and every bounced email damages your domain reputation with buyers who are already risk-averse. That Reddit founder who paused outbound for six weeks? His pipeline didn't slow down. It stopped.

This is where data quality becomes non-negotiable. Prospeo's 98% email accuracy and 7-day data refresh cycle mean your outreach actually reaches current contacts - not people who changed roles three months ago. Use 30+ search filters to narrow by industry, job title, and company size, pull verified emails and direct dials, push to Salesforce or HubSpot, and start outbound without bounces tanking your sender reputation.

Go-to-Market Mistakes That Kill Fintech Startups

Underpricing. That founder with $20K ARR? Low pricing signals "not enterprise-ready" to banks. Most fintech pricing is hybrid - platform fee plus variable fees. If you're in payments, interchange caps (0.2% debit, 0.3% credit in EU) and roughly 120-day chargeback windows directly affect your unit economics. Price for the segment you want, not the one that's easiest to close.

Pausing outbound to "fix the product." Momentum dies faster than you think. Ship and sell simultaneously.

Over-investing in paid before organic. SEO costs $647 per customer in B2B fintech. ABM costs $4,664. Find what converts organically first, then pour fuel on it.

Ignoring compliance until a deal falls through. One failed security review stalls your pipeline for a quarter. We've seen teams lose six-figure deals because they couldn't produce a SOC 2 report on request.

Sending outbound on bad data. Skip this if you want to learn the hard way, but bounced emails destroy domain reputation, and in fintech, buyers Google your company before they reply. If your first impression is a bounced message to someone who left the company, you're done.

Enterprise fintech deals have 25 stakeholders. Miss one and the deal dies. Prospeo gives you verified emails and direct dials for every buyer on the committee - 125M+ mobile numbers with a 30% pickup rate, refreshed weekly.

Reach the full buying committee, not just the gatekeeper.

Fintech Go-to-Market Strategy FAQ

How long does a fintech GTM take to show results?

B2C PLG can see traction in 2-4 months. B2B SMB takes 4-8 months. Enterprise runs 9-18 months for a typical sales cycle. Budget runway for at least two full cycles before evaluating channel performance - anything less and you're measuring noise, not signal.

What's a good LTV:CAC ratio for fintech?

Target 4:1. Banking averages 4.4:1, payment processing 2.8:1. Below 3:1, raise prices or find cheaper acquisition channels before scaling spend. Don't scale what doesn't work.

How do you build a fintech prospect list without burning your domain?

Define your ICP by institution size, decision-maker role, and geography, then use a B2B data platform with verified emails to avoid bounces. Prospeo's 98% email accuracy and 7-day refresh cycle keep contact data current - critical when targeting risk-averse financial buyers who penalize sloppy outreach. For teams scaling outbound to banks and credit unions, that accuracy gap between 79% and 98% is the difference between a healthy domain and one that's blacklisted within weeks.