How to Calculate ACV: Formulas & Examples for 2026

ACV is a policy decision, not a math problem. The formula itself is trivial - it's division. The hard part is deciding what goes into the numerator, getting your VP of Sales and CFO to agree on that decision, and then applying it consistently quarter after quarter.

Let's be honest: we've sat through more board meetings than we'd like where ACV and ARR were used interchangeably, and it never ends well.

ACV Means Two Different Things

"ACV" serves double duty across two completely different industries.

In SaaS and subscription businesses, ACV stands for Annual Contract Value - the annualized recurring revenue from a single customer contract. If you're here for this, jump to How to Calculate Annual Contract Value (SaaS).

In insurance, ACV stands for Actual Cash Value - the depreciated value of your property at the moment of a loss. If you're here for this, jump to How to Calculate Actual Cash Value (Insurance).

Same acronym, completely different math.

Quick Reference

SaaS: ACV = Total Contract Value (recurring only) / Contract Length in Years. Exclude one-time fees. Document your calculation policy before you start - your team probably doesn't agree on the details yet. Benchmark: the median private B2B SaaS ACV was $26,265 in 2024, up from $22,357 the prior year.

Insurance: ACV = Replacement Cost - Depreciation. Your insurer's offer is negotiable - always request the full valuation report. Three recognized methods exist, and which one applies depends on your state and policy language.

How to Calculate Annual Contract Value (SaaS)

The Core Formula

The standard formula is straightforward:

ACV = Total Contract Value (TCV) / Contract Length (Years)

The critical nuance: TCV here means recurring revenue only. Strip out one-time fees before you divide.

A customer signs a 3-year deal worth $120K in recurring subscription fees plus a $5K implementation fee. TCV for ACV purposes = $120K. ACV = $120K / 3 = $40K. That $5K implementation fee doesn't touch the calculation.

"Annual" vs "Average"

Teams routinely argue past each other because they're calculating different things with the same acronym. Some mean Annual Contract Value - the annualized value of one specific contract. Others mean Average Contract Value - the average across all contracts. An r/SaaS thread is full of practitioners talking past each other for exactly this reason.

The fix is simple but non-negotiable: write down your definition and circulate it before anyone opens a spreadsheet.

If you haven't written down your ACV policy, you don't have one.

Worked Scenarios

Multi-year contract: Customer signs a 2-year deal at $60K/year recurring. TCV = $120K. ACV = $120K / 2 = $60K.

Short-term contract, annualized: Customer signs a 6-month contract at $5K/month recurring. To annualize: $5K x 12 = $60K ACV. Some teams prefer to report only the contracted amount of $30K for 6 months - this is why your policy document matters.

Contracts with embedded one-time fees: A 3-year deal includes $50K/year recurring plus $15K onboarding in year one. First-year revenue hits $65K, but ACV is $50K every year. The onboarding fee is real revenue, but it belongs in TCV reporting, not ACV. An r/FPandA discussion describes exactly this scenario - a finance team wanted to include only year-one one-off revenue and ignore the rest, which is the kind of ambiguity that creates reporting chaos across the entire org. In our experience, the include/exclude debate wastes more time than the actual calculation. Document your rules and enforce them every quarter.

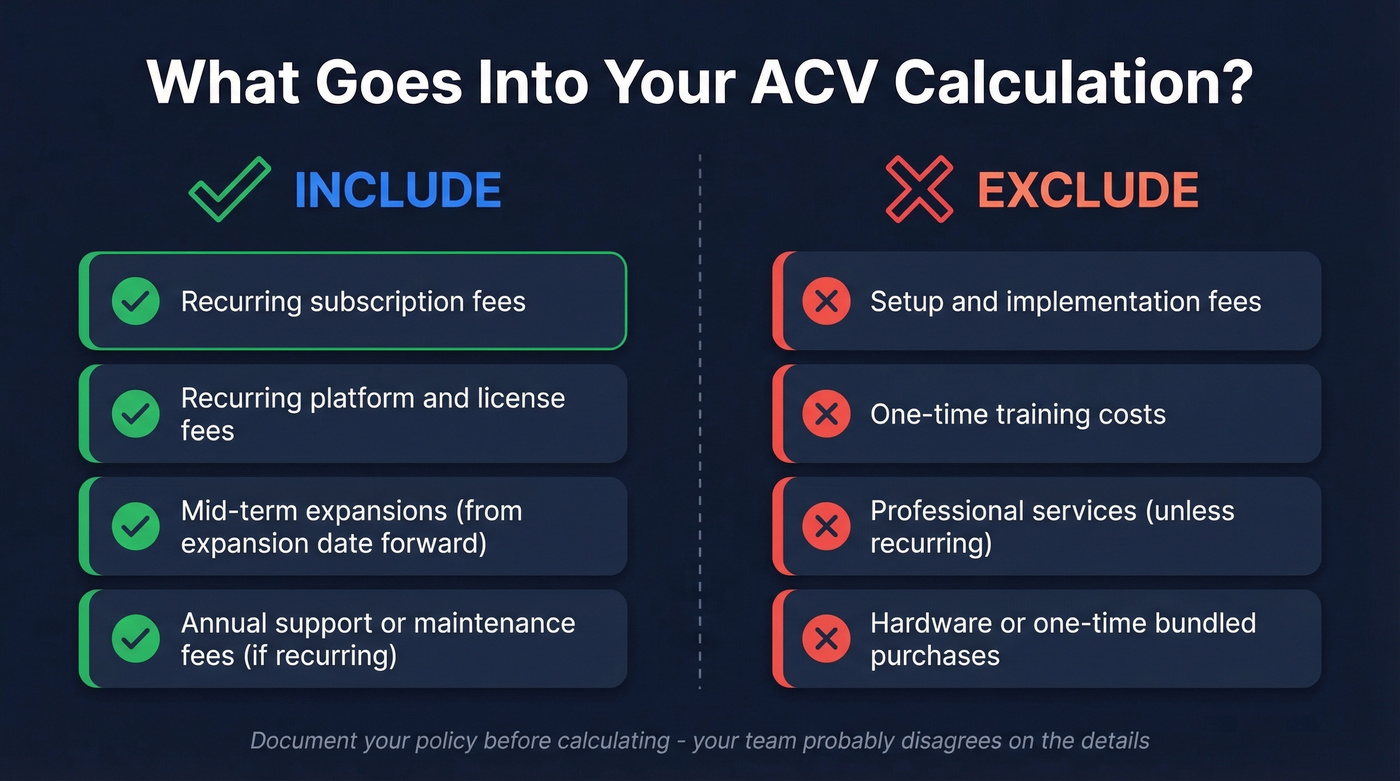

What to Include and Exclude

Include: Recurring subscription fees, recurring platform/license fees, and mid-term expansions from the expansion date forward. (If you need a clean way to standardize this in your CRM, start with lead status definitions and reporting rules.)

Exclude: Setup and implementation fees, one-time training costs, professional services (unless they recur), and hardware or one-time purchases bundled into the contract. If you’re building a repeatable process, sales process optimization matters more than the spreadsheet.

Your ACV policy only matters if reps can actually reach the accounts that move the needle. Prospeo gives your team 300M+ profiles with 30+ filters - including buyer intent, funding, and headcount growth - so they target accounts worth closing, not accounts worth chasing.

Build pipeline that grows ACV, not just activity metrics.

Ramp Deals and Usage-Based Pricing

Ramp deals break the clean formula because the annual value changes as the customer scales. SaaStr outlines two approaches:

Approach 1: Pay as revenue materializes. Credit commissions over time as usage grows. ACV reflects actual realized revenue, not projections. Simpler, less risk, but pipeline metrics look smaller upfront.

Approach 2: Model expected value upfront, with clawbacks. Estimate the customer's likely annual spend, book that as ACV, and claw back if usage falls short. Better for forecasting, but creates commission disputes.

We've seen teams waste months debating this. Pick Approach 1 unless your usage data is mature enough to model reliably. Clawbacks destroy rep trust faster than they improve forecast accuracy. If you’re trying to make this predictable, pair it with sales forecasting solutions that can handle usage signals.

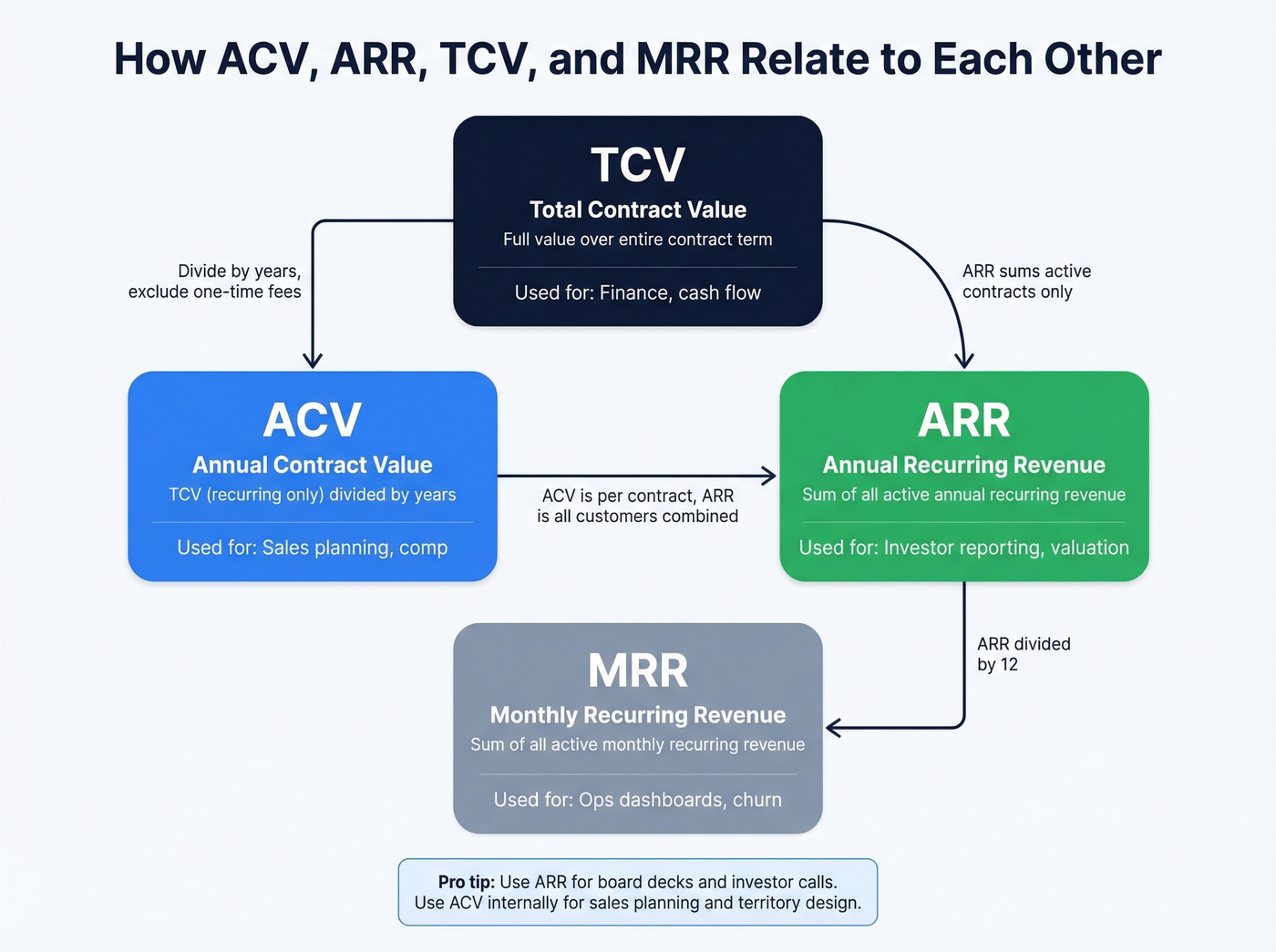

ACV vs ARR vs TCV

| Metric | Formula | When to Use | Standardized? |

|---|---|---|---|

| ACV | TCV (recurring) / Years | Sales planning, comp | No |

| ARR | Sum of all active annual recurring revenue | Investor reporting, valuation | Mostly |

| TCV | Total value over full contract term | Finance, cash flow | No |

| MRR | Sum of all active monthly recurring revenue | Ops dashboards, churn tracking | Yes |

An analysis of 160+ public tech company SEC filings found that even ARR definitions fall into four buckets: pure subscription, subscription plus variable, subscription plus managed services, and variable revenue only.

Use ARR for external reporting and investor conversations. Use ACV internally for sales planning, territory design, and comp structures. Make sure your board knows which definition you're using. If you’re pressure-testing the model, pipeline health metrics will usually surface ACV policy issues fast.

What's a Good ACV?

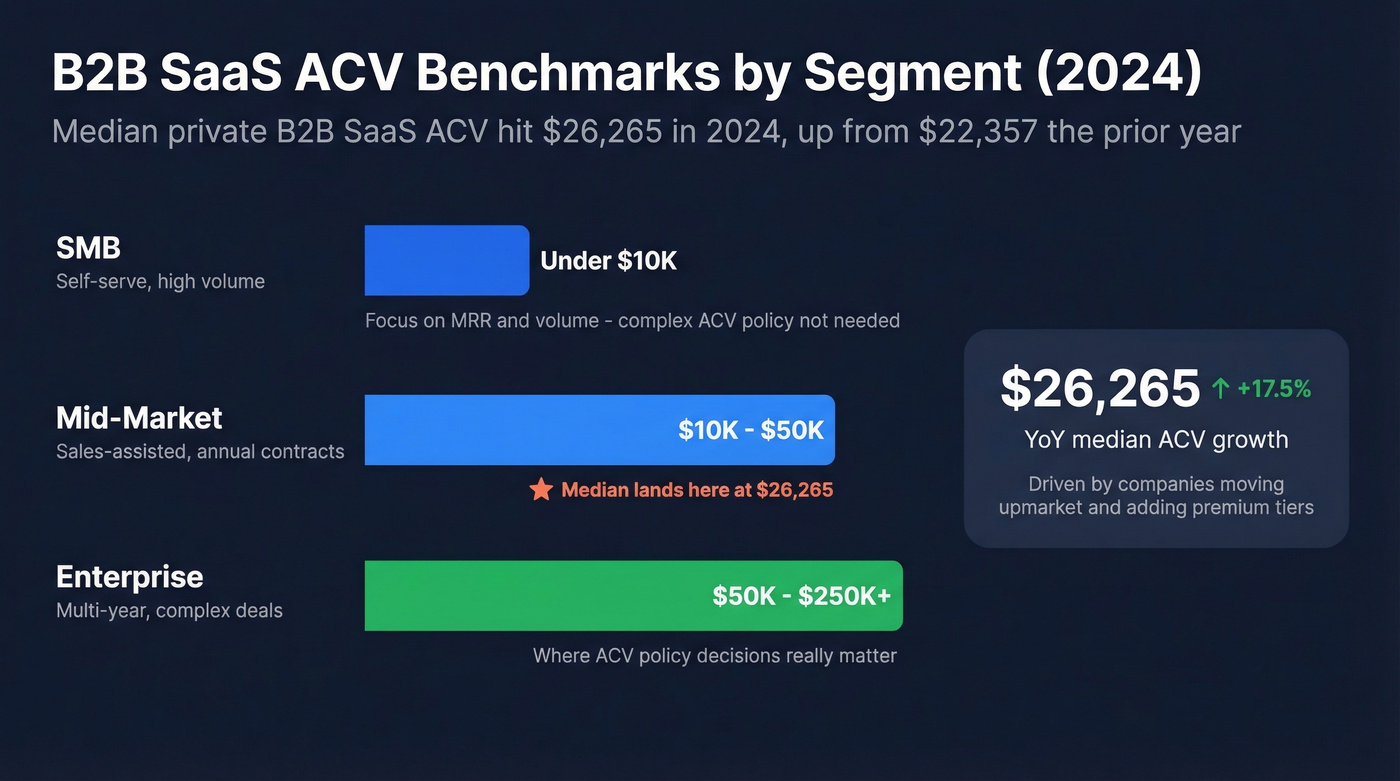

The median private B2B SaaS ACV was $26,265 in 2024, up from $22,357 the prior year - driven largely by companies moving upmarket and adding premium tiers. SMB products typically run under $10K, mid-market lands in the $10K-$50K range, and enterprise deals stretch from $50K to $250K+.

Here's the thing: if your deals are consistently below $10K, you probably don't need a complex ACV policy at all. Focus on MRR and volume. The annualized contract math starts mattering when deals get large enough that one contract can move the needle on a rep's quota. If you’re moving upmarket, align this with enterprise B2B sales motions.

Growing ACV means closing larger deals with more senior decision-makers - and that starts with reaching them. Tools like Prospeo help reps spend time selling into bigger accounts instead of bouncing off bad data, with 98% email accuracy and 125M+ verified mobile numbers. To keep outreach consistent as deal sizes rise, use sales prospecting techniques that match your ICP.

Bigger deals require direct access to senior decision-makers. Prospeo delivers 98% verified emails and 125M+ mobile numbers with a 30% pickup rate - so your reps spend time selling into enterprise accounts instead of bouncing off bad data at ~$0.01/email.

Stop losing enterprise deals to bad contact data.

How to Calculate Actual Cash Value (Insurance)

The Formula and Three Methods

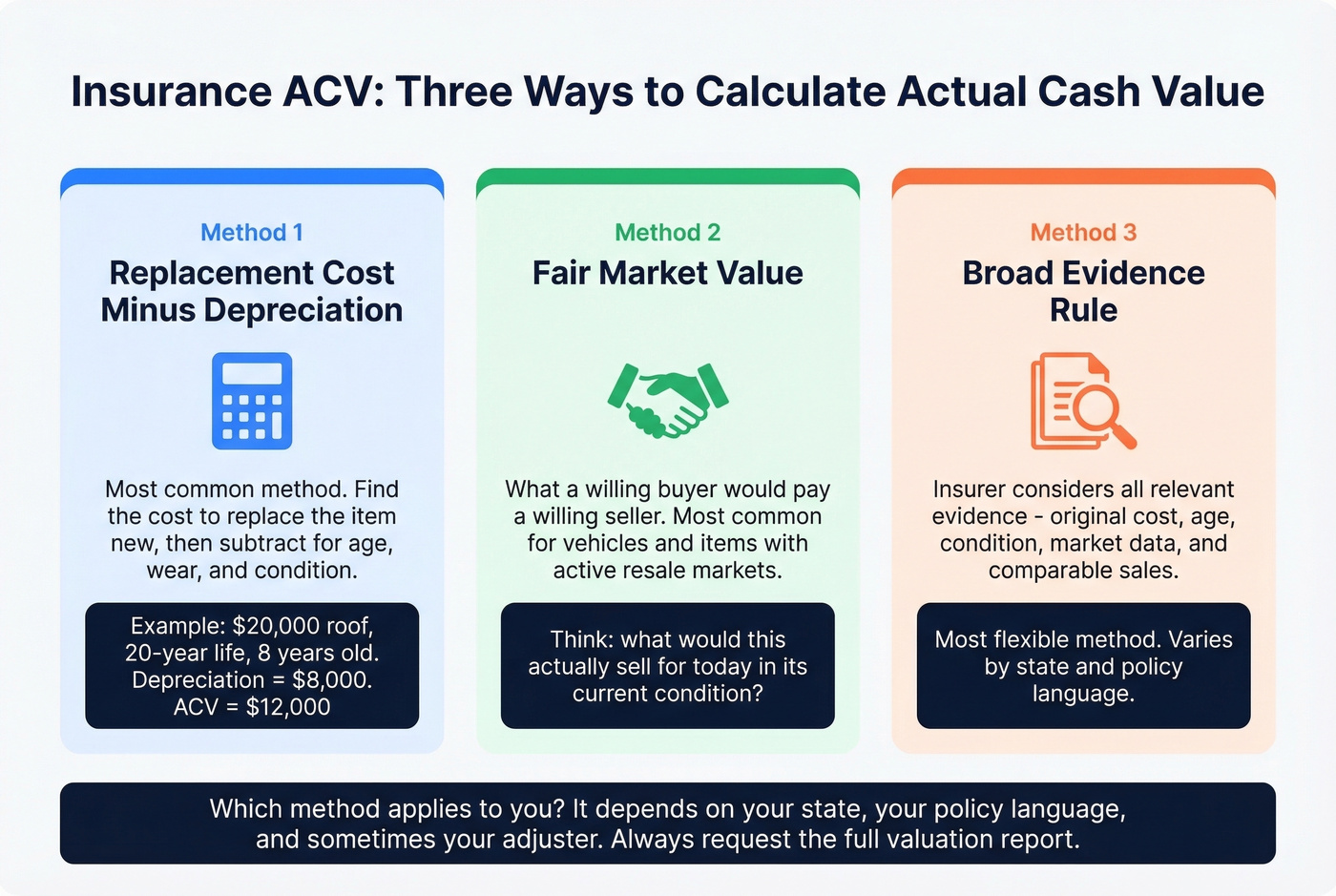

In insurance, ACV determines what your insurer pays when property is damaged or totaled. The IRMI (International Risk Management Institute) recognizes three approaches:

- Replacement cost minus depreciation - the most common method. Find what it costs to replace the item new, then subtract for age, wear, and condition.

- Fair market value - what a willing buyer would pay a willing seller. Common for vehicles.

- Broad evidence rule - the insurer considers all relevant evidence including original cost, age, condition, and market data.

Worked example using straight-line depreciation: You bought a roof for $20,000 with a 20-year expected lifespan. After 8 years, a storm destroys it. Depreciation = ($20,000 / 20) x 8 = $8,000. ACV = $20,000 - $8,000 = $12,000. That's your starting payout before deductible.

Why Your Payout Seems Low

Insurance ACV is built on the indemnity principle: the goal is to make you whole, not better off than before the loss. The depreciated value will almost always feel low compared to what you'd actually pay to replace the item in today's market.

There's no single nationwide rule. Methods vary by state, by policy language, and sometimes by adjuster. A major ongoing controversy is whether insurers can depreciate labor costs in addition to materials - several states have moved to prohibit labor depreciation, which can materially increase payouts. Check your state's department of insurance for current rules.

Real talk: ACV isn't the same as what you see on dealer lots or marketplace listings. Listing prices reflect what sellers hope to get. Actual cash value reflects what the item is worth in its current condition, factoring in depreciation, at the moment of loss. The gap between those numbers is where most disputes start.

Negotiating a Higher Settlement

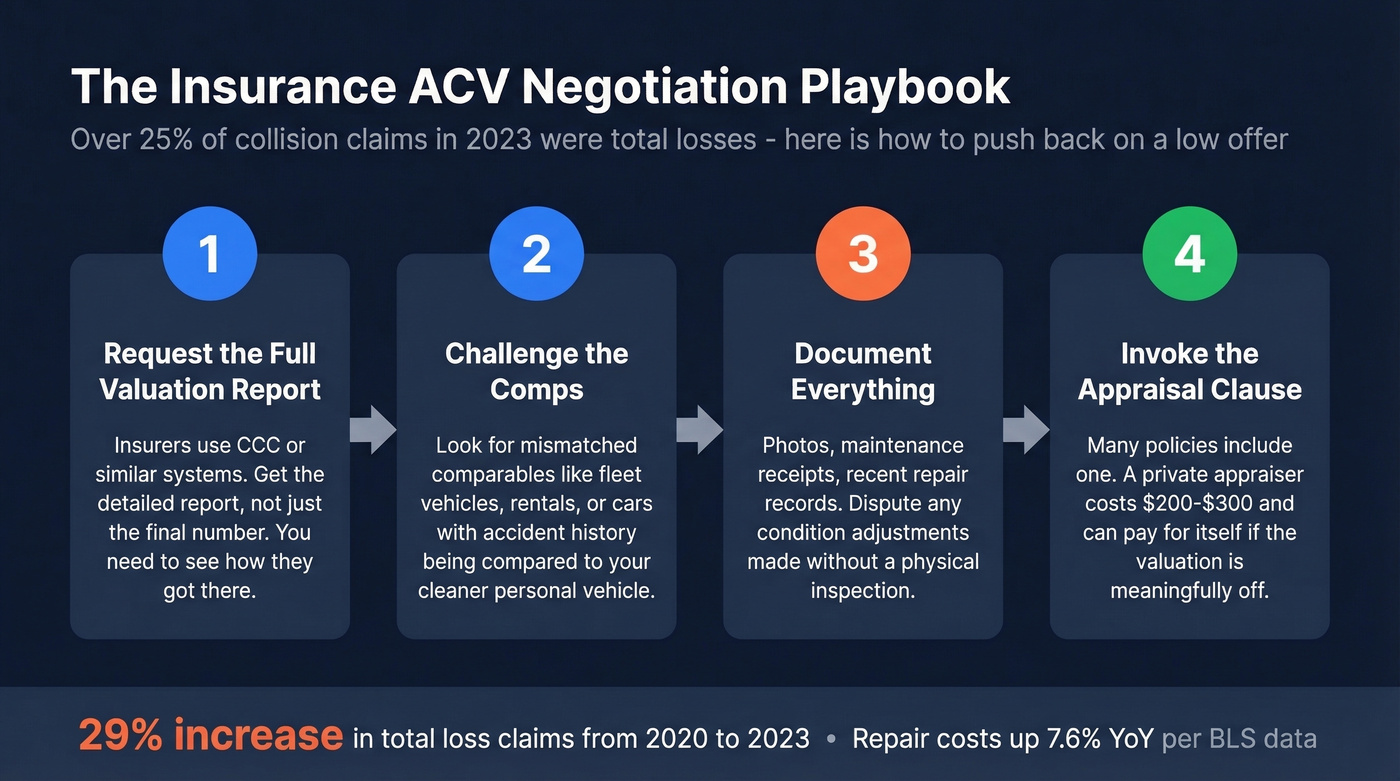

Over a quarter of all collision claims in 2023 were total losses - a 29% increase from 2020. Motor vehicle repair costs increased 7.6% between April 2024 and April 2025 per BLS data. Insurers typically declare a vehicle a total loss when repair costs exceed around 60-80% of the car's ACV, depending on state and insurer.

If you're in this situation, skip the frustration and go straight to the playbook:

- Request the full valuation report. Insurers often use CCC or similar third-party valuation systems. Get the detailed report, not just the number.

- Challenge the comps. A common issue in CCC reports is mismatched comparables - fleet or rental vehicles, cars with accident history - being used against a cleaner personal vehicle. Push back with comps that reflect your car's actual condition.

- Document everything. Photos, maintenance receipts, records of recent repairs. Condition adjustments applied without a physical inspection are worth disputing.

- Invoke the appraisal clause. Many policies include one. Hiring a private appraiser typically costs $200-$300 and can pay for itself if the valuation is meaningfully off.

CCC reports aren't gospel. They're a starting point, and insurers expect pushback from informed policyholders.

FAQ

Does ACV include one-time fees?

No. Standard practice excludes setup, implementation, and training fees from the ACV calculation. Include only recurring revenue before dividing by contract years. One-time charges belong in TCV reporting instead.

What's the difference between ACV and ARR?

ACV is the annualized value of one contract. ARR is annualized recurring revenue across all customers. Use ARR for investor reporting and valuation; use ACV for sales planning, territory design, and rep compensation.

How do insurers determine actual cash value?

Insurers use one of three methods: replacement cost minus depreciation, fair market value, or the broad evidence rule. The method depends on your state and policy language. Always request the full valuation report before accepting an offer.

Can you negotiate ACV with your insurer?

Yes. Request the detailed valuation report, challenge mismatched comps with your own comparable sales data, provide maintenance documentation, and hire a private appraiser if the gap justifies the cost.

What's a good ACV for SaaS?

The median private B2B SaaS ACV was $26,265 in 2024. SMB products typically run under $10K, mid-market $10K-$50K, and enterprise $50K-$250K+. The right target depends on your go-to-market motion and sales model.