How to Get Leads for Mortgage Loans: The Practitioner's Playbook

A new LO we know spent her first three months emailing realtors, getting ghosted, and then suggested splitting Zillow ad spend 50/50 with the one agent who actually called her back. That agent never responded again.

Figuring out how to get leads for mortgage loans is the first real challenge every LO faces - and the advice floating around assumes you already have a referral network or a $7,500/month Zillow budget. The financial services blended CPL sits at $653, mortgage leads get expensive fast because many sources are resold or shared, and pricing climbs based on exclusivity. Competition for every borrower is fiercer than it's been in a generation.

The LOs who build sustainable pipelines don't rely on one channel. They stack two or three sources that compound over time, and they measure cost per funded loan - not cost per lead. That distinction changes everything about how you allocate budget and effort.

What Actually Works (Quick Version)

New LO? Start with social media on TikTok and Instagram plus non-traditional referral partners like CPAs, estate attorneys, and financial planners. You don't have a database or realtor network yet, so build visibility first.

Established? Double down on realtor referral partnerships and database reactivation. Your existing network is your cheapest pipeline by a wide margin.

Scaling? Layer in owned content and SEO, plus selective exclusive lead buying. Measure everything by cost per funded loan.

Mortgage Lead Costs in 2026

Before you spend a dollar, understand what you're buying. Lead pricing varies wildly based on exclusivity, freshness, and source. One LO on r/loanoriginators reported spending $7,500/month on Zillow alone - and was actively looking for alternatives after five years.

Another common scenario: you drop $15,000 on a portal over a few months, close three loans, and realize you paid $5,000 per funded loan. That math only works if your average commission covers it comfortably.

Current market pricing:

| Lead Type | Cost/Lead | Contact Rate |

|---|---|---|

| Aged (30-85 days) | $2-$5 | 20-35% |

| Aged (86-365 days) | $1-$2 | 15-25% |

| Aged (366+ days) | $0.50-$1 | 8-18% |

| Fresh shared (3-5 buyers) | $20-$35 | 35-50% |

| Semi-exclusive (2 buyers) | $35-$50 | 40-55% |

| Exclusive (vendor) | $50-$100 | 50-65% |

| High-intent exclusive | $100-$150+ | 55-70% |

| Live transfer (standard) | $50-$75 | 8-15% close |

| Live transfer (premium) | $75-$100+ | 12-20% close |

| Trigger leads* | $0.15-$0.50 | 15-25% |

*Trigger lead pricing is volume-tiered: $0.30-$0.50 for 1K-5K leads, $0.20-$0.30 for 5K-25K, and $0.15-$0.20 for 25K+.

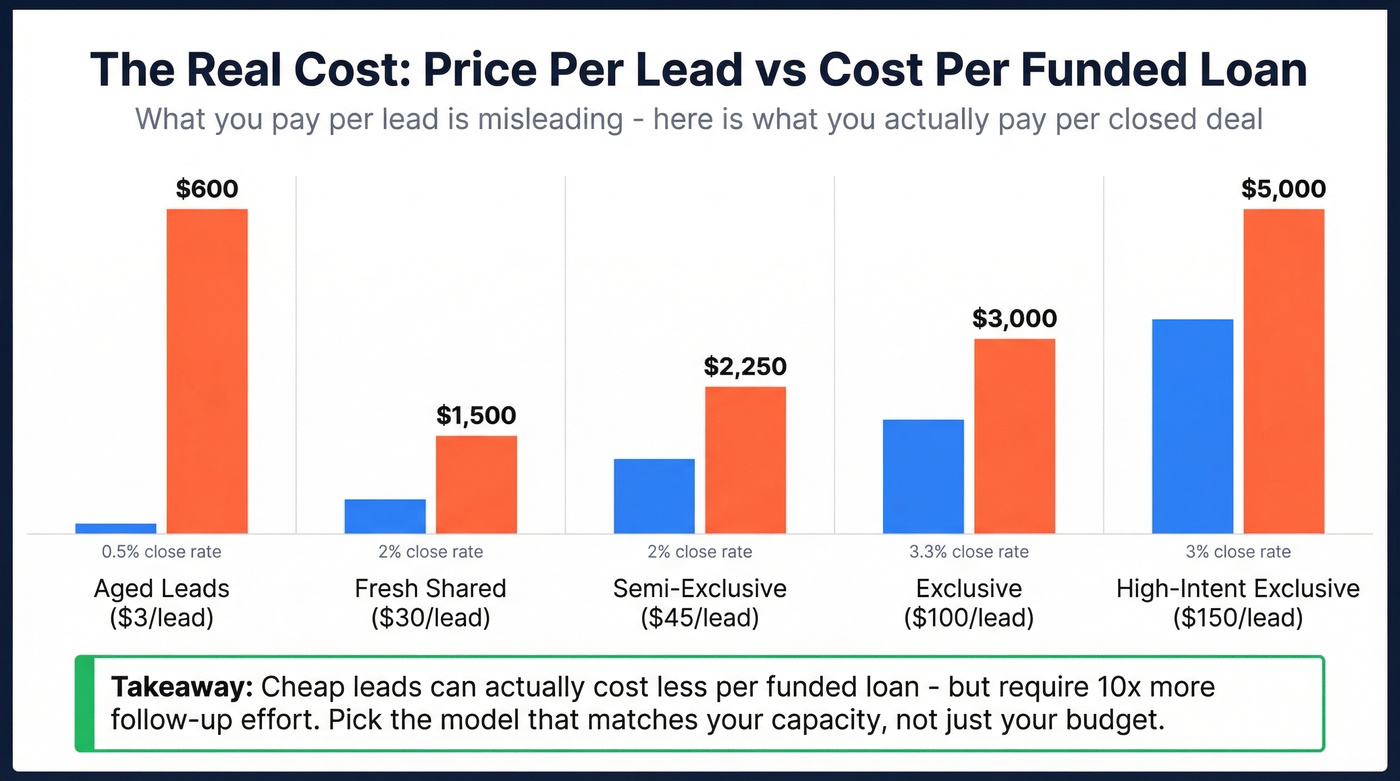

The takeaway isn't that one type is "best." A $150 exclusive lead that closes at 5% costs you $3,000 per funded deal. A $3 aged lead that closes at 0.5% costs you $600 per funded deal - but requires ten times the follow-up effort. Pick the model that matches your capacity, not just your budget.

8 Proven Mortgage Lead Generation Channels

Realtor Referral Partnerships

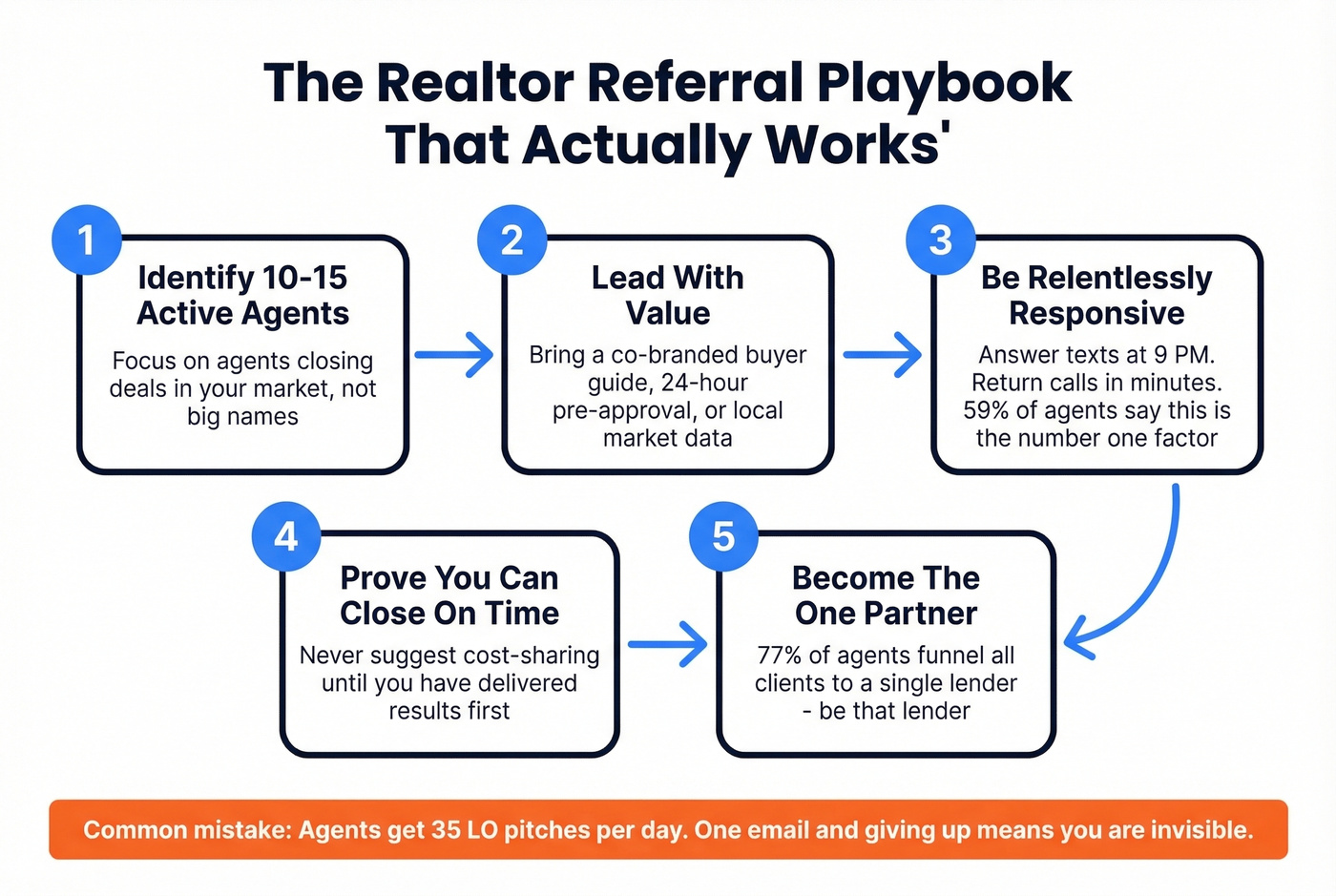

Still the highest-ROI channel for established LOs. 96% of top loan officers cite agent partners as their strongest referral source, and 77% of agents funnel all their clients to a single lender partner. If you're that partner, you've got a pipeline that compounds every quarter.

But getting there is brutal. Agents get bombarded with up to 35 LO pitches per day, and 59% say responsiveness is the number-one factor in choosing a lending partner - not rates, not marketing spend, not technology.

Here's what new LOs get wrong: they lead with what they need instead of what they offer. They suggest cost-sharing arrangements before they've proven they can close on time. They send one email and give up.

The playbook that works: pick 10-15 agents in your market who are actively closing deals. Show up with value - a pre-approval process that takes 24 hours, a co-branded first-time buyer guide, or market data they can share with clients. Then be relentlessly responsive. Answer texts at 9 PM. Return calls within minutes. That's how you become the one partner out of 35 daily pitches who actually sticks.

Non-Traditional Referral Partners

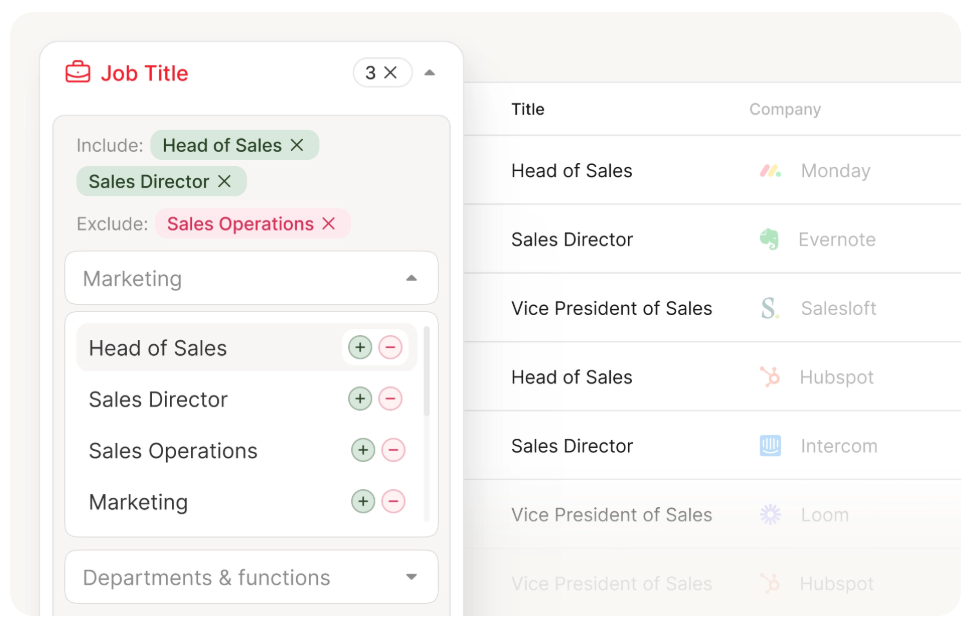

Realtors get all the attention, but CPAs, estate attorneys, divorce attorneys, financial planners, insurance agents, and credit union loan officers all sit upstream of mortgage decisions. A CPA doing someone's taxes sees the W-2 income, the savings balance, and the rental payments - they know who's ready to buy before the client does.

The challenge is finding these professionals systematically instead of cold-walking into offices. Prospeo handles this well: build targeted lists of CPAs, attorneys, and financial planners in your specific market, filter by job title and location across 300M+ professional profiles, then export verified emails and direct dials. The 98% email accuracy means your outreach actually lands, and the free tier gives you 75 verified emails per month - enough to build a referral partner pipeline from scratch without spending a dollar on lead vendors.

The outreach itself is simple: introduce yourself, explain the mutual benefit (you send them clients who need tax advice or estate planning, they send you clients who need pre-qualification), and suggest a coffee meeting. Most LOs never think to prospect these partners systematically, which means the field is wide open.

Content Marketing and SEO

Local mortgage content is one of the least competitive SEO niches relative to its value. Searches like "first-time homebuyer programs in [your city]," "FHA loan requirements [state] 2026," and "conventional loan rates [county] today" carry real buyer intent and thin competition from individual LOs.

Start a blog on your website. Write two to four posts per month targeting local keywords. A single well-ranking page on your state's down payment assistance program - the kind of niche topic that gets zero competition from national sites - can rank within weeks and pull in pre-qualified traffic for years. After 12 months of consistent publishing, your organic pipeline can rival what you'd get from a $2,000/month ad budget.

Link to authoritative resources like HUD's local homebuying resources and your state housing finance agency's first-time buyer programs to build topical authority. Cover jumbo loan thresholds, VA loan eligibility, and Fannie Mae guideline changes - these signal depth to both readers and search engines.

Social Media

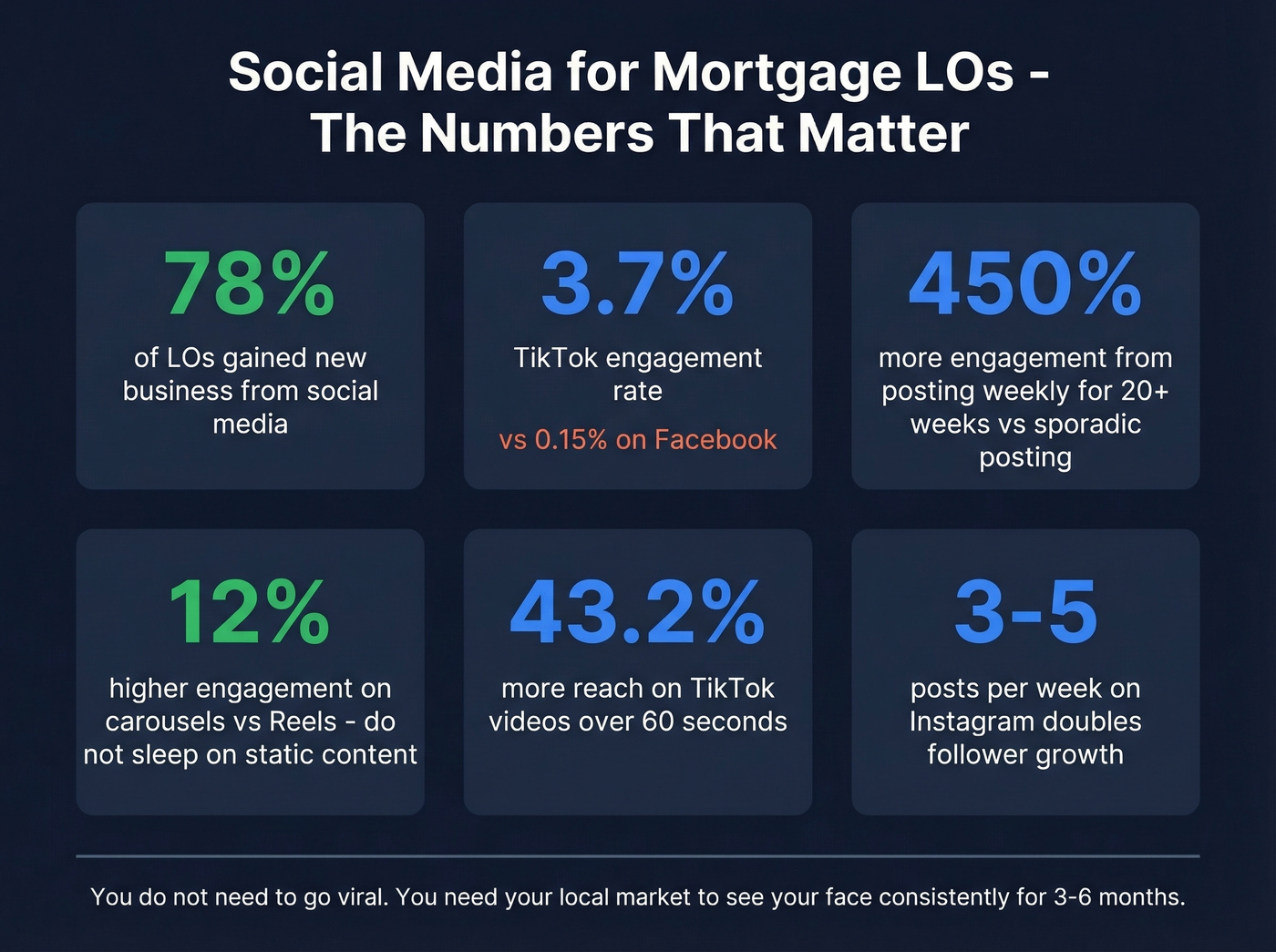

78% of mortgage loan officers report gaining new business directly from social media. The engagement gap between platforms is massive: TikTok mortgage content averages ~3.7% engagement versus Facebook's ~0.15%.

Content formats that work: myth-vs-fact carousels ("You need 20% down - myth or fact?"), day-in-the-life vertical video, local market snapshots with real numbers, client journey stories with permission, and rate-vs-reality breakdowns. Carousels actually outperform Reels by 12% on engagement, so don't sleep on static content.

Consistency matters more than creativity. Posting once a week for 20+ weeks produces 450% more engagement than sporadic posting. Instagram at 3-5 posts per week doubles follower growth. TikTok videos over 60 seconds get 43.2% more reach and 63.8% more watch time than shorter clips.

You don't need to go viral. You need your local market to see your face and name consistently enough that when they think "mortgage," they think of you. That takes 3-6 months of steady posting, not one lucky Reel.

Local SEO and Google Business Profile

Your Google Business Profile is free and criminally underused by most LOs. Optimize it with your NMLS number, service areas, loan types you handle - FHA, VA, conventional, jumbo - and hours. Post weekly updates covering rate changes, market commentary, and client wins. Ask every closed client for a Google review and aim for 50+ reviews within your first year.

Target local keywords on your website: "[city] mortgage lender," "best mortgage rates in [county]," "VA loan [city]." Strong buyer intent, and most individual LOs aren't competing for them.

Database Reactivation

Your CRM is full of leads who said "not right now" six months ago. Rates shift, life circumstances change, and the LO who stays in touch gets the deal when timing aligns.

Set up a monthly touchpoint cadence. HubSpot, Zoho, and Streak all have free tiers that handle this, and mortgage-specific CRMs like Surefire and BNTouch have built-in rate-alert triggers that automate the process entirely. Each month, reach out with something valuable: a rate drop alert, a new loan program announcement, a seasonal hook like "spring buying season is starting - here's what's changed since we last talked." The key is value-based messaging, not "just checking in." Re-engaging old leads monthly is one of the highest-ROI activities in mortgage because the acquisition cost is zero - you already paid for these contacts.

Paid Ads and Direct Mail

Use this if: You have $2,000+/month to test, a landing page with a clear CTA like a pre-qualification form or rate quote tool, and the patience to optimize for 60-90 days before judging results.

Skip this if: You're a new LO with no budget cushion, or you don't have a system to follow up within 5 minutes. Paid leads that sit for hours are wasted money.

Google Ads targeting "[city] mortgage rates" and "home loan pre-approval" can work well, but financial services paid CPL averages $761. Facebook and Instagram ads run cheaper - expect $20-$60 per lead for a well-targeted campaign - but lead quality is lower because you're interrupting, not capturing intent.

Don't overlook direct mail. It's old-school, but mortgage direct mail still pulls a 5-9% response rate versus about 1% for email. A targeted postcard campaign to recent pre-movers or rate-sensitive homeowners in your zip code can cost around $0.50-$1.50 per piece and generate warm inbound calls. In our experience, LOs who pair digital ads with a direct mail drip to the same audience see noticeably higher conversion rates than either channel alone. If you want a deeper breakdown of formats, targeting, and cost math, see our guide to direct mail.

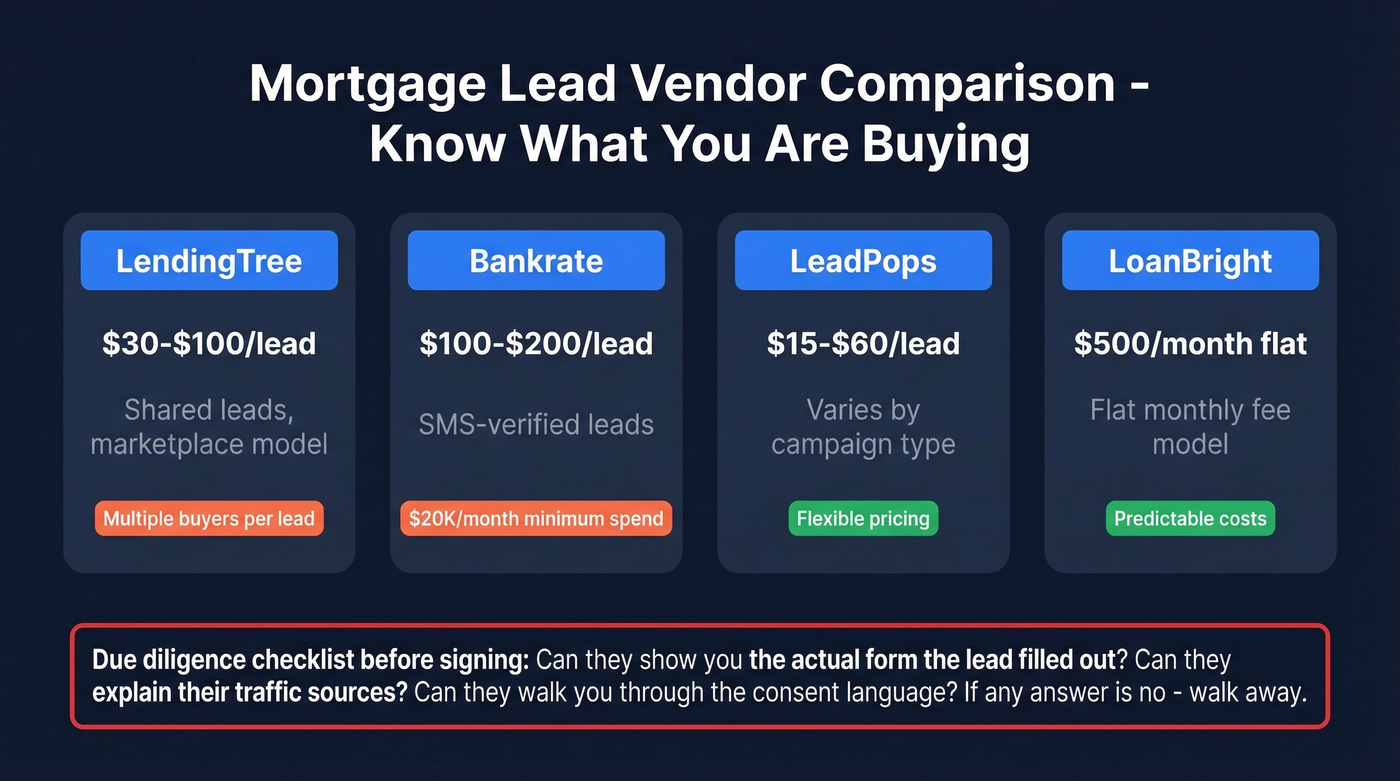

Buying Leads

Purchased leads are a volume stabilizer, not a growth strategy. That's a hill I'll die on. At 1-5% close rates on a $50-$150 CPL, you're paying $3,000-$15,000 per funded loan. That can work if your commission covers it, but it won't compound the way referrals and content do.

| Vendor | Cost/Lead | Notes |

|---|---|---|

| LendingTree | $30-$100 | Shared, marketplace |

| Bankrate | $100-$200 | SMS-verified, $20K/month minimum spend |

| LeadPops | $15-$60 | Varies by campaign |

| LoanBright | $500/mo | Flat monthly fee |

Before you sign with any vendor, run this due diligence checklist: Can they show you the actual form the lead filled out? Can they explain their traffic sources? Can they walk you through the consent language the borrower agreed to? If the answer to any of these is no, walk away. You're buying their compliance liability along with their leads.

Stop cold-walking into CPA offices. Prospeo gives you 300M+ professional profiles filtered by job title and location - find every CPA, estate attorney, and financial planner in your market with verified emails and direct dials. At $0.01 per email with 98% accuracy, one referral partner list costs less than a single aged lead.

Build your entire referral partner pipeline before your next coffee meeting.

The Lead Follow-Up Playbook

Speed kills - in a good way. Responding within 5 minutes makes you 100x more likely to connect with a lead. Most LOs wait hours. That gap alone is a competitive advantage.

We've seen the LOs who close the most purchased leads call within 3 minutes, not 5. Here's a cadence that converts:

- Day 1: Call + text + email within 5 minutes. Introduce yourself, reference their inquiry, offer a quick 10-minute call.

- Day 3: Follow up with value - a rate comparison, a loan estimate timeline, or a relevant market insight.

- Day 7: Share a resource like a first-time buyer guide or closing cost breakdown. Ask if their timeline has changed.

- Day 14: Final direct outreach. "I don't want to be a pest - if now isn't the right time, I'll check back in 30 days with a market update."

Segment your leads into hot (actively shopping), warm (interested but not urgent), and cold (long-term nurture). Tailor the cadence intensity accordingly. It takes 5-8 touches to convert a mortgage lead - "just checking in" doesn't count as a touch. Every contact should deliver something useful. If you need copy you can swipe, use these sales follow-up templates and adapt them to mortgage.

Compliance - What Most Guides Skip

Let's be honest: the line that should be tattooed on every LO's wall is "When you buy leads, you're buying the seller's compliance program." That's the most important sentence in this entire article.

TCPA risk doesn't come from malice - it comes from process gaps. Texting or dialing outside your approved systems. Not reviewing disclosure language. Having no proof-of-consent system of record. Failing to disposition opt-outs correctly, leading to repeat calls that generate complaints. We've seen LOs get burned by vendors who couldn't produce proof of consent when challenged - and the LO, not the vendor, took the regulatory hit.

The Homebuyer Privacy Protection Act is now in place, aimed at minimizing trigger leads. Exceptions exist for originating lenders and servicers, and opt-in changes the equation, but the compliance burden on trigger leads is real and growing. The CFPB's mortgage marketing guidance is worth bookmarking - it's updated regularly and spells out exactly where the lines are.

Your vendor audit should cover four things: map the path from ad to form to submission, confirm exactly when the lead is sold to you, validate the consent language at the moment of capture, and verify DNC list hygiene is happening on their end - not just yours. If you're doing any outbound texting, read up on cold texting rules and risk.

Pick 2-3 Channels and Go Deep

You don't need eight lead sources. You need two or three that you actually execute on with consistency and discipline. A new LO posting TikTok content three times a week and prospecting 10 CPAs per month will outperform someone dabbling in Zillow ads, buying aged leads, cold-calling realtors, and posting on Instagram once a month.

Look, if your average loan amount is under $250K and your market has more than 50 active LOs, you probably can't afford to make purchased leads your primary channel. The math just doesn't work at that price point. Build owned channels first - referrals, content, social - and use purchased leads to fill gaps, not carry the pipeline. If you want a system for staying consistent, borrow a 30-60-90 day plan and map it to your lead channels.

The metric that matters isn't cost per lead. It's cost per funded loan. Track that number for every channel you use to get leads for mortgage loans. Kill the ones that don't work. Double down on the ones that do. That's the entire strategy. For more ideas on what to test next, see these sales prospecting techniques.

Mortgage leads cost $50-$150 each from vendors - and half get shared with competing LOs. Prospeo lets you build exclusive prospect lists of homebuyer-adjacent professionals for $0.01 per verified contact. Filter by title, location, and company size across 300M+ profiles, then export direct dials and emails that actually connect.

Own your pipeline instead of renting someone else's recycled leads.

FAQ

How much do mortgage leads cost in 2026?

Mortgage leads range from $0.50 for aged leads over 366 days old to $150+ for high-intent exclusive leads. Live transfers run $50-$100+ per call. Budget $50-$150 per lead for quality exclusives, then calculate your true cost per funded loan - at a 3% close rate on $100 leads, that's roughly $3,300 per closed deal.

What's the best lead source for new loan officers?

Social media - specifically TikTok and Instagram - combined with non-traditional referral partners like CPAs and estate attorneys. You don't have a database or realtor network yet, so build visibility and relationships first. Buying leads before you have a follow-up system is burning money.

Are purchased mortgage leads worth it?

As a volume stabilizer, yes. As a primary growth strategy, no. At 1-5% close rates on $50-$150 per lead, you're paying $3,000-$15,000 per funded loan. Use purchased leads to fill pipeline gaps while building owned channels - referrals, content, SEO - that compound over time.

How fast should I follow up with a mortgage lead?

Within five minutes - three if you can manage it. You're 100x more likely to connect at that speed versus waiting an hour. Set up instant notifications from your CRM or lead source so you never miss that window. Most LOs wait hours, which means speed alone differentiates you.

How do I find referral partners without cold-walking into offices?

Use a B2B data platform like Prospeo to build targeted lists filtered by job title and location - CPAs, attorneys, financial planners in your market - with verified emails and direct dials. The free tier gives you 75 verified emails per month, enough to systematically prospect 15-20 referral partners weekly via personalized email outreach instead of random office drop-ins.