Monthly Recurring Revenue: The Practitioner's Guide to Getting MRR Right

You're prepping your Series A deck, and the first slide says "$85K MRR." But did you normalize that annual contract your biggest customer paid upfront? Did you back out the $3K setup fee? Are those 40 trial users inflating the number? A Paddle survey of 50 SaaS companies found that 1 in 5 subtract expenses from monthly recurring revenue, 2 in 5 include trialing or free users, and a majority mishandle annual and quarterly payment normalization. Your MRR number is probably wrong - and this guide is about fixing that before an investor's analyst does it for you.

The Short Version

- MRR = normalized monthly subscription value. Not cash collected, not bookings, not revenue recognized.

- Track momentum with Net New MRR: New + Expansion + Reactivation - Contraction - Churn.

- Write an MRR policy before you track anything. Definitions drift, and drifting definitions make historical comparisons meaningless.

- Median SaaS growth based on the latest 2026 data is ~26-28%. If you're still benchmarking against 2021 numbers, recalibrate.

- Expansion MRR is your most underrated growth lever. It accounts for 40% of total new ARR at the median - and over 50% for companies above $50M.

What Is MRR?

Monthly recurring revenue is the normalized monthly value of all active subscription plans at a given point in time. It's not the cash that hit your bank account this month. It's not what your billing system invoiced. It's a standardized metric that answers one question: if nothing changes, how much subscription revenue will we generate every month?

That distinction matters more than most founders realize. A customer who pays $12,000 upfront for an annual plan contributes $1,000 to MRR - not $12,000 in the month they paid. MRR strips out timing noise so you can see the underlying health of your business.

Why does this metric matter? Three reasons. First, forecasting - MRR gives you a clean baseline for projecting future revenue without lumpy cash distortions. Second, investor confidence - VCs and board members use MRR and its annualized cousin ARR as the primary lens for evaluating subscription businesses. Third, growth tracking - decomposing MRR into its component movements tells you where growth is coming from and where it's leaking.

MRR isn't a GAAP metric. It's not defined by ASC 606 or IFRS 15, which means there's no universal standard. Every company defines it slightly differently, and that's exactly why you need a written policy.

How to Calculate MRR

The Basic Formula

The simplest version:

MRR = Number of Active Paying Subscribers x Average Revenue Per User (ARPU)

Five customers each paying $200/month = $1,000 MRR. Simple enough.

The critical nuance is normalization. If a customer is on a quarterly plan at $600, their MRR contribution is $200. Annual plan at $2,400? That's $200/month. One-time setup fees, professional services charges, and variable consumption fees don't count. MRR captures only the recurring subscription component, normalized to a monthly cadence.

A Realistic Worked Example

Let's say you have four customers at the end of March:

| Customer | Plan / Billing | Contract Value | Discount | MRR |

|---|---|---|---|---|

| Acme Co | Pro / Monthly | $500/mo | None | $500 |

| Beta Inc | Enterprise / Annual | $18,000/yr | 10% off | $1,350 |

| Gamma LLC | Starter / Quarterly | $900/qtr | None | $300 |

| Delta Corp | Pro / Monthly | $500/mo + $2K setup | None | $500 |

Acme is straightforward - $500 monthly, no adjustments. Beta signed an annual contract at $18,000 but negotiated a 10% discount, so the effective annual value is $16,200; divide by 12 and you get $1,350 MRR. Gamma pays $900 quarterly, so $300 per month. Delta pays $500/month plus a one-time $2,000 setup fee - the setup fee gets excluded entirely because it's not recurring.

Total MRR: $2,650.

A quick spreadsheet with these four columns handles this calculation for most early-stage companies. Once you pass ~50 customers or start mixing billing intervals heavily, move to a dedicated tool like ChartMogul (free tier available, paid plans around ~$100-$599/mo), Baremetrics (~$108-$500+/mo), or ProfitWell (free core analytics). These pull directly from your billing system and handle normalization automatically.

The Five Types of MRR

New MRR

Revenue from brand-new customers who signed up this month. Three new customers each starting a $300/month plan = $900 in new MRR.

Expansion MRR

Additional revenue from existing customers who upgraded, added seats, or moved to a higher tier. If a customer goes from $100/month to $200/month, the expansion MRR is $100 - the incremental increase, not the total.

Here's the thing: this is the number most teams undervalue. Benchmarkit's 2026 data shows expansion accounts for 40% of total new ARR at the median. For companies above $50M ARR, it's over 50%. Expansion is cheaper than acquisition, compounds over time, and signals product-market fit in a way that new logos alone can't.

Contraction MRR

Revenue lost from existing customers who downgraded. A customer moving from $500/month to $300/month represents $200 in contraction MRR. They're still a customer - they're just paying less.

Churn MRR

Revenue lost from customers who cancelled entirely. If a $400/month customer churns, that's $400 in churn MRR. Don't confuse this with customer churn (logo churn), which counts the number of lost accounts regardless of their revenue contribution.

Reactivation MRR

Revenue from previously churned customers who come back. Someone who cancelled their $250/month plan three months ago and resubscribes? That's $250 in reactivation MRR.

Net New MRR Formula

The equation that ties everything together:

Net New MRR = New MRR + Expansion MRR + Reactivation MRR - Contraction MRR - Churn MRR

A complete example: this month you added $5,000 in new MRR, $2,000 in expansion, and $500 in reactivation. You lost $800 to contraction and $1,200 to churn.

Net New MRR = $5,000 + $2,000 + $500 - $800 - $1,200 = $5,500

That $5,500 is your growth signal. It tells you whether the business is accelerating, decelerating, or treading water - far more useful than looking at total MRR alone.

Common MRR Mistakes

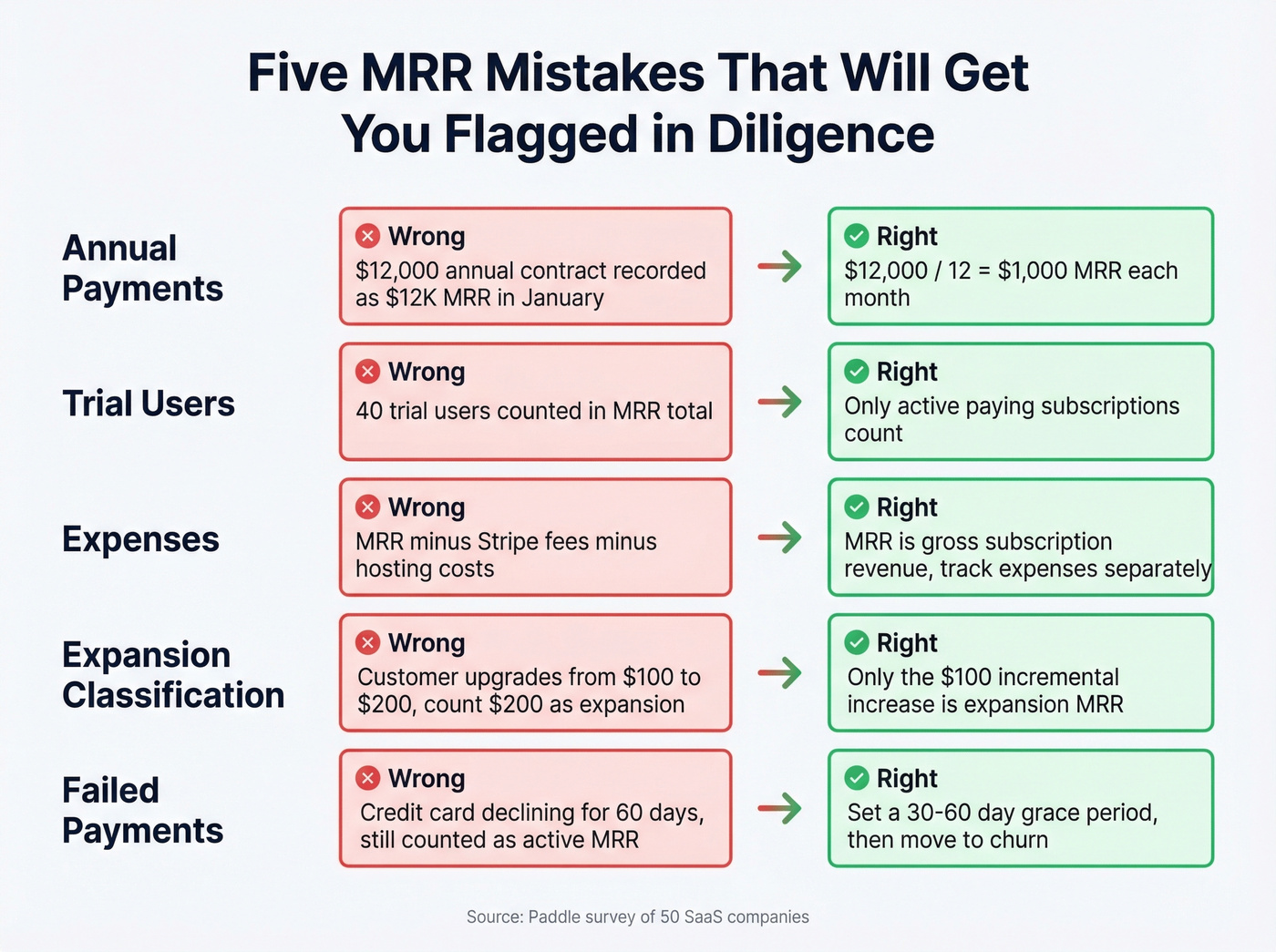

The Paddle survey numbers bear repeating: 1 in 5 SaaS companies subtract expenses from MRR, 2 in 5 include trial or free users, and a majority mishandle billing interval normalization. Here are the specific mistakes and how to avoid them.

1. Recording annual payments as a single month's MRR. A $12,000 annual contract is $1,000/month MRR - not $12,000 in January and $0 for the next 11 months. This makes your MRR chart look like an EKG. Reddit threads are full of founders confused about exactly this. Fix: Always divide by the subscription length in months.

2. Including trial and free-tier users. If they're not paying, they don't contribute to MRR. Period. Including them inflates your number and will get flagged in diligence. Fix: MRR counts only active, paying subscriptions.

3. Subtracting payment processing fees or other expenses. MRR is a gross subscription metric. Your Stripe fees, hosting costs, and support expenses don't belong here. Fix: Track expenses separately. MRR is top-line recurring revenue.

4. Misclassifying expansion vs. new MRR. When a customer upgrades from $100/month to $200/month, is that $100 in expansion MRR or $200 in total MRR for the account? Both numbers are useful, but they answer different questions. Many dashboards blur the line. Fix: Define expansion as the incremental increase from existing customers. Document this in your MRR policy.

5. Counting delinquent or failed charges as active MRR. A customer whose credit card has been declining for 45 days isn't really contributing to your recurring revenue. Fix: Set a grace period - typically 30 to 60 days - then move delinquent accounts to churn MRR.

Expansion MRR is your most efficient growth lever - but only if your team is talking to real decision-makers. Prospeo's 300M+ profiles with 98% email accuracy mean your outbound actually connects, so every rep drives net new pipeline instead of bouncing into the void.

Stop losing MRR to bad contact data. Start connecting at 98% accuracy.

MRR vs ARR vs Bookings vs Revenue

MRR vs ARR

ARR = MRR x 12. That's the math. The decision of when to use which is more nuanced.

Use MRR when you're tracking month-to-month operational performance - it's your heartbeat metric. Use ARR when you're reporting to investors, benchmarking against industry data, or when most of your contracts are annual or longer. A common founder confusion on r/SaaS: if all your customers pay multi-year upfront, does dividing total annual turnover by 12 to get "MRR" even make sense? Yes - because MRR isn't about cash timing. It's about the normalized run-rate of your subscription base.

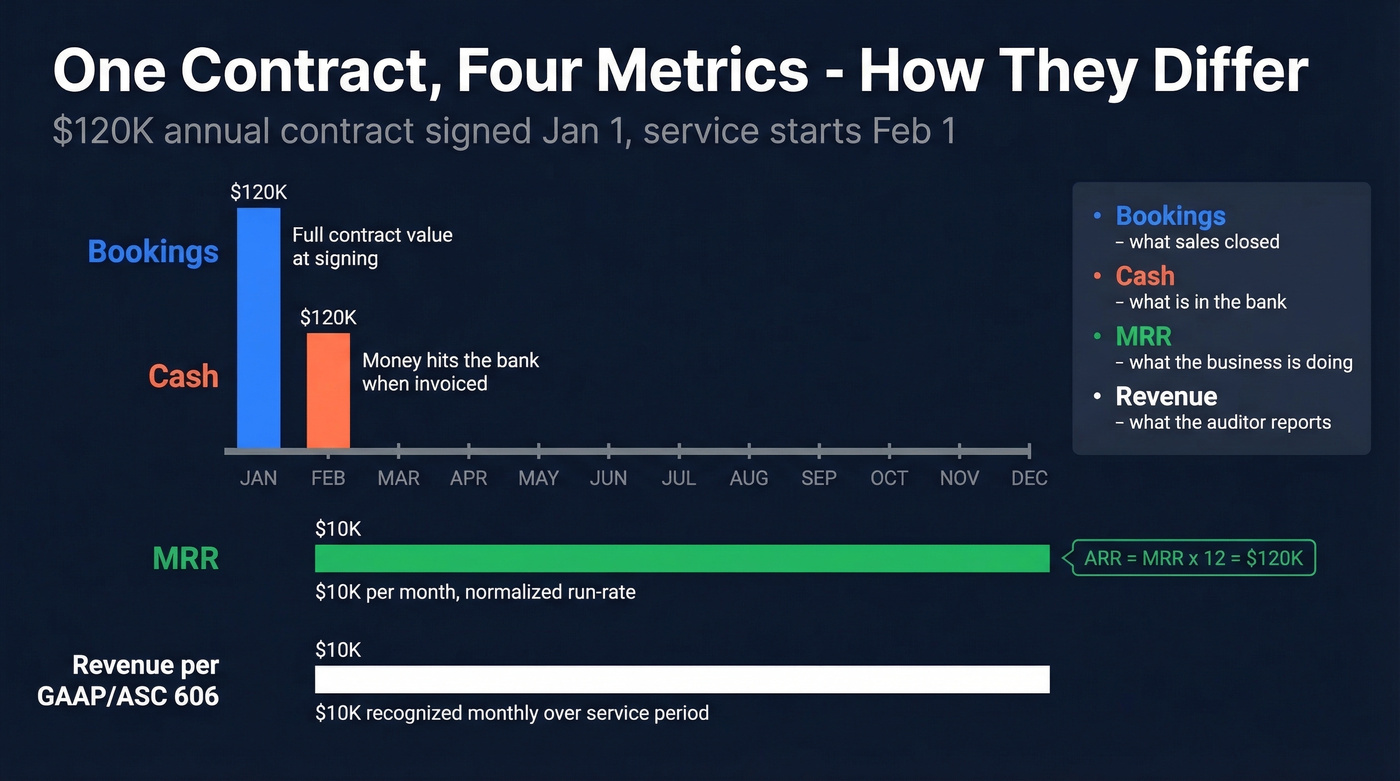

Cash, Bookings, and Revenue

These four metrics describe the same contract from different angles. Take a $120,000 annual contract signed January 1 with a February 1 go-live:

| Metric | Definition | Example |

|---|---|---|

| Bookings | Contract value at signing | $120K in Jan |

| Cash | Money received | $120K when invoiced |

| MRR | Normalized monthly sub value | $10K/mo ongoing |

| Revenue (GAAP) | Earned per ASC 606 | $10K/mo starting Feb |

Under ASC 606, revenue is recognized over the service period - not when the contract is signed or when cash is collected. That $120K sits as deferred revenue on your balance sheet and converts to recognized revenue at $10,000/month starting when service begins.

Bookings tell your sales team how much they closed. Cash tells your CFO what's in the bank. MRR tells your ops team what the business is doing. Revenue tells your auditor what you can report. They're all useful. They're all different. Confusing them is how you end up with a board deck that doesn't match your P&L.

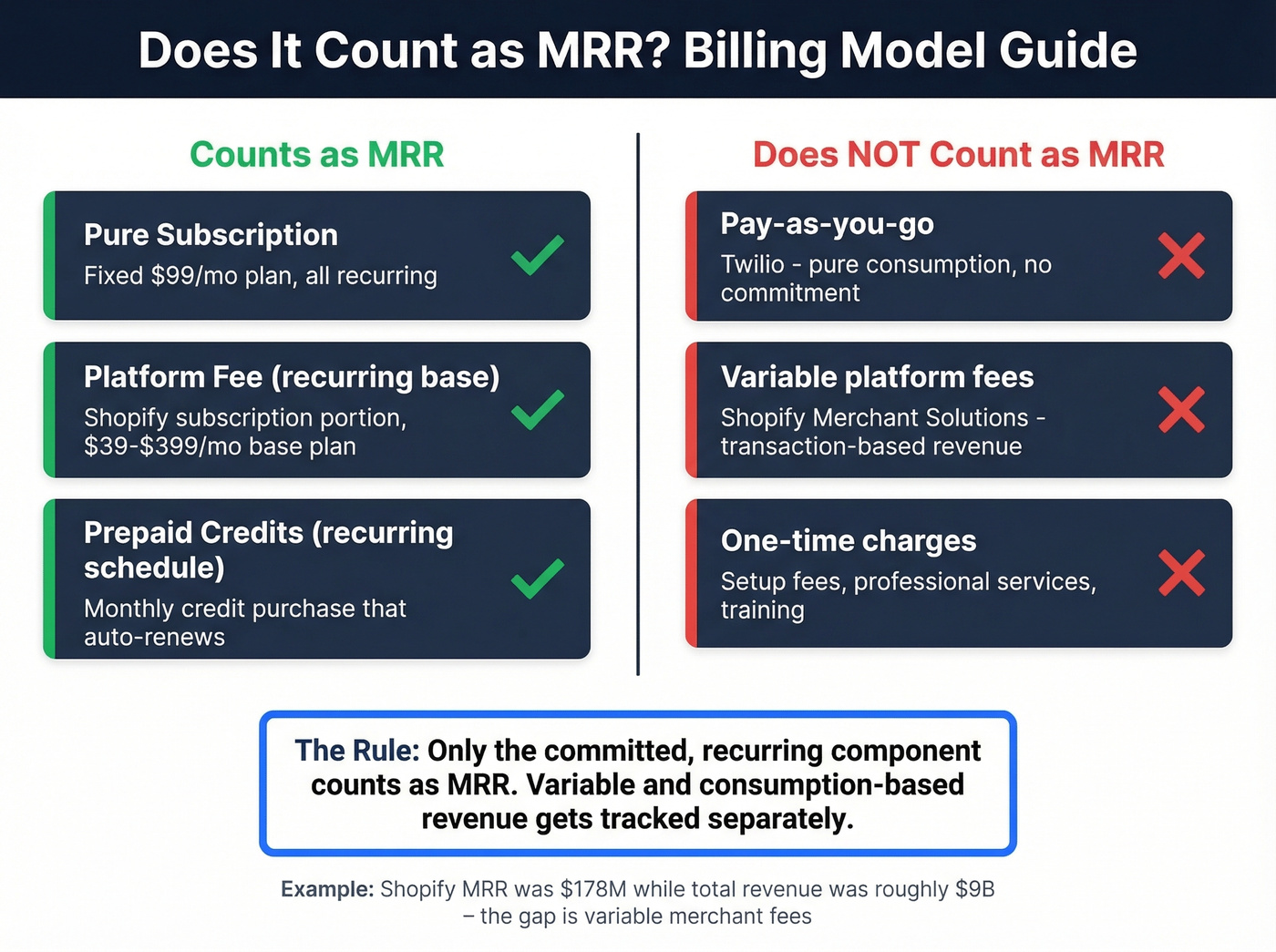

Hybrid and Usage-Based Billing

Not every SaaS company runs pure subscriptions anymore. Shopify is the clearest example: their MRR at the end of 2024 was $178M - implying ~$2B ARR - while total revenue was roughly $9B. The gap? Variable platform fees from their Merchant Solutions business, which Shopify explicitly excludes from MRR.

The rule: only the committed, recurring component counts as MRR. Variable and consumption-based revenue gets tracked separately.

Usage-based models come in several flavors, each with different MRR implications. Schematic's taxonomy is useful here:

- Pay-as-you-go (Twilio) - no MRR; it's all variable

- Prepaid credits (OpenAI) - the credit purchase is MRR if it recurs on a schedule

- Tiered usage plans (Mixpanel) - the tier subscription is MRR; overages aren't

- Base plan plus overages (Customer.io) - base is MRR; overages aren't

- Committed usage agreements (Stripe enterprise) - the committed minimum is MRR

For teams running a hybrid model, document exactly which components count as MRR and which don't. Investors will ask.

How to Build an MRR Policy

Before you track MRR in any tool, write down your definitions. We've seen teams where the CFO's spreadsheet, the ChartMogul dashboard, and the board deck all show different MRR numbers - because nobody wrote down the rules. Every SaaS company should document these decisions:

- Billing interval normalization: Annual / 12, quarterly / 3, semi-annual / 6. No exceptions.

- Discount treatment: Do you record MRR at the gross price or the discounted price? Most companies use net (after discount), but pick one and stick with it.

- Expansion vs. contraction classification: Expansion = incremental increase from an existing customer. Contraction = incremental decrease. Document the threshold and timing.

- Proration handling: Prorations are billing artifacts, not MRR movements. Exclude them.

- One-time charge exclusion: Setup fees, implementation fees, professional services - none of these are MRR.

- Multi-currency conversion: Pick a rate (spot rate at contract signing, monthly average, or fixed rate) and apply it consistently.

- Reactivation window: How long does a customer need to be churned before a return counts as reactivation vs. a new subscription? Common choices are 30, 60, or 90 days.

- Trial and free user exclusion: Only paying customers count. Full stop.

- Delinquent account grace period: How many days of failed payment before you reclassify to churn?

Write this down. Put it in a shared doc. Make sure your finance team, your analytics tool, and your billing system all agree.

2026 SaaS MRR Benchmarks

Growth and Efficiency

The growth environment has cooled significantly from the 2021-2022 highs. Here's where things stand:

| Metric | Median | Trend |

|---|---|---|

| Annual growth | 28.29% | Down from 47.25% prior year |

| Top quartile growth | 65.40% | Down from 87.55% |

| Revenue churn | 12.5% | Slightly up |

| Customer churn | 16.25% | Flat |

| NRR | 101% | Stable |

| New CAC ratio | $2.00 per $1 ARR | Up 14% YoY |

| S&M multiple | 3.19x | Down from 6.08x |

| Expansion % of new ARR | 40% | Up 5% YoY |

These numbers tell a clear story: growth is harder and more expensive. The median CAC ratio of $2.00 means you're spending two dollars in sales and marketing for every dollar of new customer ARR. That's real pressure on unit economics, and it's why expansion revenue matters more than ever. The annual growth, churn, and S&M multiple trend data come from Lighter Capital's 2026 benchmarks; NRR, CAC ratio, and expansion mix data from Benchmarkit.

One bright spot from High Alpha's benchmarks: companies that deeply embed AI into their product grow roughly 2x faster than those using AI as a supporting feature. The gap is most significant in the $1-5M ARR range, where AI differentiation drives ~70% faster growth.

If your average deal size is under $10K annually, skip the growth playbook designed for enterprise SaaS. Your MRR math is dominated by volume and churn, not expansion and NRR. Focus on reducing involuntary churn and shortening time-to-value before you invest in a complex upsell motion.

Net Revenue Retention by Segment

NRR is the single best predictor of long-term growth.

| Segment | Median NRR | Best-in-Class |

|---|---|---|

| Enterprise (>$100K ACV) | 118% | >130% |

| Mid-market ($25-100K) | 108% | >130% |

| SMB (<$25K) | 97% | >110% |

The venture-backed SaaS median sits at 106% in a widely cited benchmark dataset of 2,100 companies. SaaS Capital's research found that companies with NRR at or above 110% consistently grow faster than the median 24% rate, while those below 100% lag behind.

The NRR formula:

NRR = (MRR at end of period from customers who existed at start of period) / (Total MRR at start of period)

If your December 2025 cohort generated $100K MRR and those same customers generate $108K in December 2026, your NRR is 108%. The SMB segment's sub-100% median is a warning: if you're selling low-ACV subscriptions, your base erodes every month unless you fight harder on retention.

How to Grow Monthly Recurring Revenue

Reduce Revenue Churn

The 12.5% median revenue churn means the typical SaaS company loses an eighth of its revenue base every year. Two high-leverage tactics: implement dunning automation to recover failed payments before they become involuntary churn, and optimize your cancellation flow with save offers and pause options. Involuntary churn accounts for 20-40% of total churn at many companies - it's the easiest churn to fix because the customer didn't actually want to leave. (If you want a deeper framework, see our churn analysis guide.)

Double Down on Expansion

Expansion is 40% of total new ARR at the median. Build usage-based upsell triggers that fire when customers approach plan limits. Prompt seat expansion when new team members are detected. The best expansion motion feels like a natural next step for the customer, not a sales pitch. (For the mechanics, compare upsell vs cross-sell in SaaS.)

Optimize Pricing

Offer a 10-20% discount for annual commitments - it locks in MRR, reduces churn risk, and improves cash flow. Beyond discounting, align your pricing metric with the value customers actually receive. If you charge per seat but customers get value from usage volume, you're leaving expansion revenue on the table.

Fix Your Outbound Data

Your new MRR is only as good as your pipeline. We see this constantly: an SDR team generates 200 leads per week, but 35% of emails bounce. That leaves ~130 deliverable contacts, which at a 5% reply rate yields maybe 2 demos. Meanwhile, you're paying $2.00 in S&M for every $1.00 of new ARR and wondering why CAC keeps climbing. If you're diagnosing this, start with email bounce rate benchmarks and fixes.

Look, bad contact data is the silent killer of new MRR. Prospeo's 98% email accuracy on a 7-day refresh cycle means your team spends time selling instead of chasing dead addresses. At ~$0.01 per verified email, it's a fraction of the cost of a wasted SDR hour - and teams like Snyk cut bounce rates from 35-40% to under 5% after switching, adding 200+ new opportunities per month. To systematize the top of funnel, use a lead generation workflow and tighten your sales prospecting techniques.

Meritt tripled their weekly pipeline from $100K to $300K by switching to verified contact data. When your New MRR depends on outbound, a 35% bounce rate kills growth. Prospeo keeps it under 4% - at $0.01 per email, no contracts.

Fix your pipeline inputs and watch Net New MRR compound.

FAQ

Is MRR a GAAP metric?

No. MRR is a non-GAAP operating metric not defined by ASC 606 or IFRS 15. Companies define it internally, which is why a written MRR policy is essential for consistency and investor confidence.

How do I handle annual contracts in MRR?

Divide the annual contract value by 12. A $12,000 annual contract equals $1,000 MRR per month, regardless of when cash was collected. Never record the full annual amount in a single month.

What's a good MRR growth rate in 2026?

Median annual growth for private B2B SaaS is ~26-28%. Top quartile sits around 65%. Early-stage companies should target 10-20% month-over-month growth, though that rate naturally decelerates as your base grows.

Should I include free trials in MRR?

No. MRR counts only paying customers on active subscription plans. Including trials inflates your number and will mislead investors - yet 2 in 5 SaaS companies make this mistake.

How can I improve outbound's contribution to new MRR?

Start with data quality. If your bounce rate exceeds 5%, you're wasting pipeline. Verify your contact lists before every campaign, use real-time validation to catch stale records, and refresh your data at least monthly. Teams that prioritize email accuracy consistently see higher reply rates, shorter sales cycles, and lower CAC - all of which feed directly into new MRR growth.