How to Sell Technology to Banks (And Actually Close the Deal)

The demo went perfectly. The CIO nodded along, the innovation lab asked smart questions, and someone said "this could change everything." Then - nothing. Weeks of silence. If you've tried selling technology to banks, you've lived this exact scenario: enthusiasm up front, a black hole once risk and procurement show up.

Here's the truth: you don't lose bank deals on product. You lose them on process.

What You Need (Quick Version)

- Show up compliance-ready. SOC 2 Type II is table stakes, and it takes 6-12 months if you're starting from scratch.

- Start with a no-data pilot in one department. Enterprise-wide pitches create enterprise-wide delays.

- Sell to the bank's vendor-risk lifecycle. If you can't name the stage you're in, you can't control the deal.

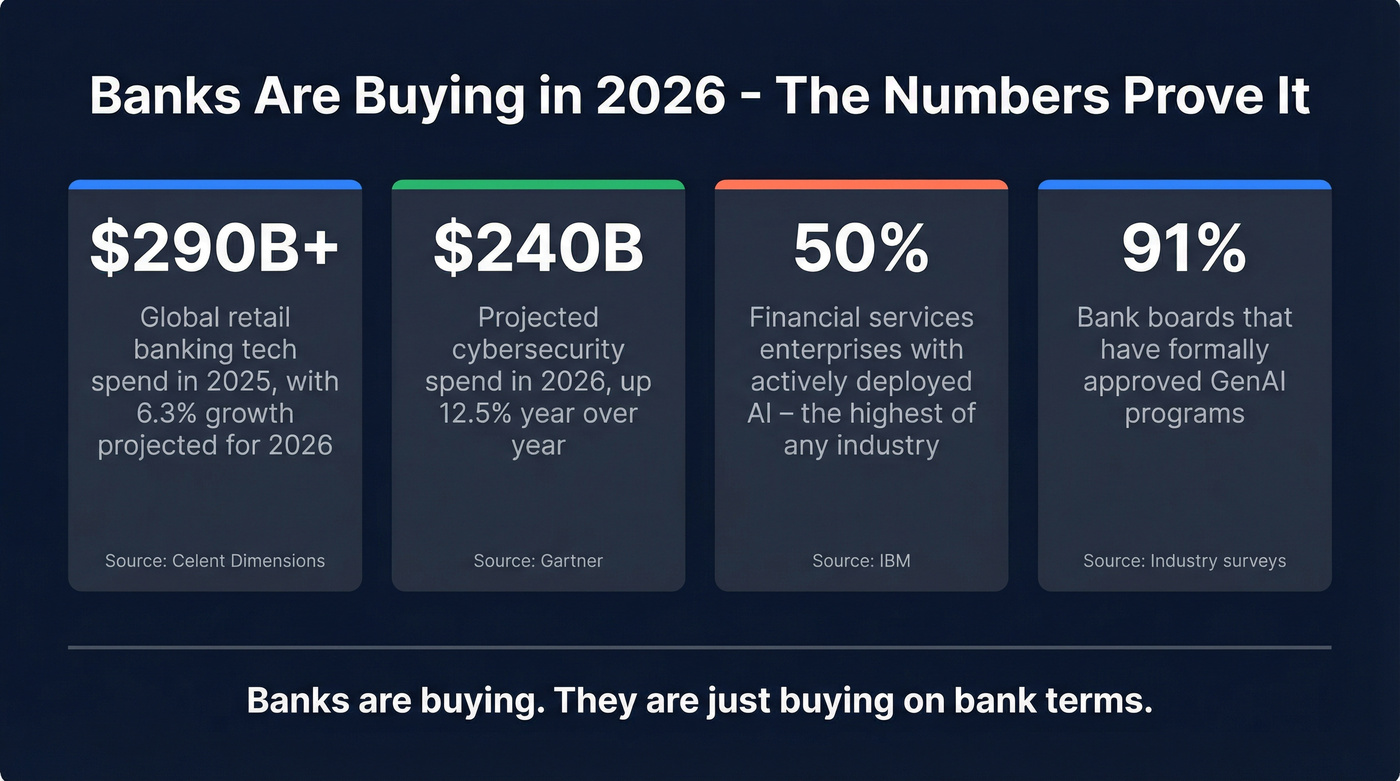

Why Banks Are Buying in 2026

Bank tech budgets aren't tightening - they're shifting toward platforms that reduce cost and risk. Celent's Dimensions program put global retail banking technology spend at $273B in 2024, forecast $290B in 2025, and projects 6.3% expansion in 2026. Security is grabbing an even bigger slice: Gartner forecast cybersecurity spend growing 12.5% to $240B in 2026.

AI is already past the pilot phase. IBM data shows financial services has the highest share of enterprises with actively deployed AI at 50%, and 98% of banking leaders either use generative AI now or plan to within two years. At the board level, 91% of bank boards have formally approved GenAI programs.

Banks are buying. They're just buying on bank terms.

Why Bank Tech Sales Are Different

Banks want outcomes, but they're built to avoid unforced errors. That means your real competitor usually isn't another vendor - it's "do nothing" and "we'll build it ourselves." Most banks carry a strong in-house build bias, and they'll default to it unless you make the risk and economics of buying painfully obvious.

Here's the thing: innovation labs are where deals go to die. Labs evaluate. Procurement buys. Risk approves. If you can't get past the "cool demo" crowd into the people who own vendor risk, you're not in a sales cycle - you're in a science fair.

Skip banks entirely if your deal size sits below $10K annually. The fixed cost of vendor risk assessment will crush your ROI. Either raise your price, bundle more value, or target a different segment.

Bank deals die when you can't reach the right stakeholder. With 30+ filters - including department headcount, job changes, and technographics - Prospeo helps you map every decision-maker in a bank's vendor-risk chain, from the CIO to the compliance officer who signs off last.

Stop pitching innovation labs. Start reaching the people who actually approve vendors.

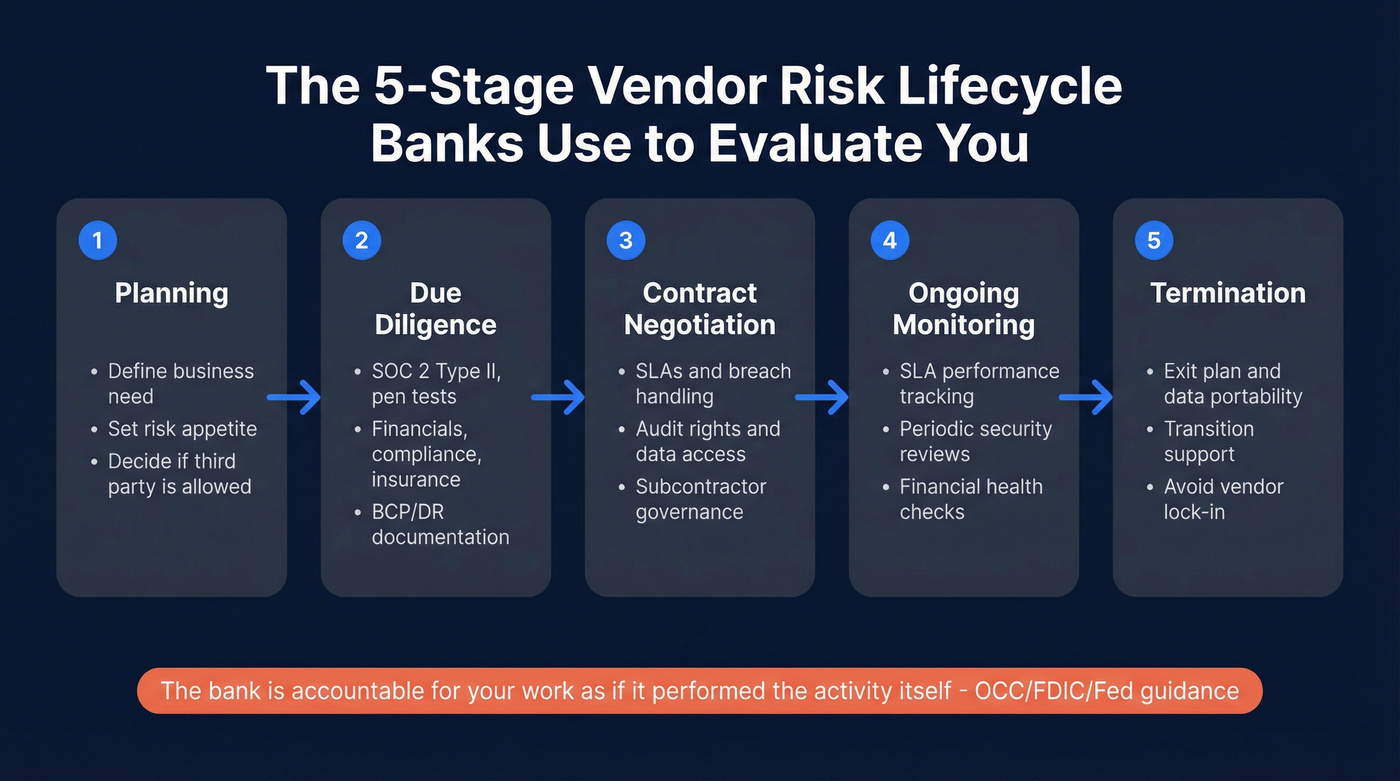

The Vendor-Risk Framework Banks Use

In 2024, the Federal Reserve, FDIC, and OCC released updated third-party risk management guidance that lays out how banks are expected to manage vendors. The headline is brutal and simple: the bank is accountable for your work as if it performed the activity itself.

Most bank vendor relationships follow a five-stage lifecycle:

- Planning - Business need, risk appetite, and whether a third party is even allowed for the use case.

- Due Diligence - Security, financials, compliance, resilience, insurance, and evidence like SOC 2 Type II, pen tests, BCP/DR documentation.

- Contract Negotiation - SLAs, breach handling, audit rights, data access, subcontractors, and governance.

- Ongoing Monitoring - SLA performance, periodic security reviews, financial health checks, complaint tracking.

- Termination - Exit plan, data portability, transition support, and how the bank avoids vendor lock-in.

If you sell like this lifecycle doesn't exist, you'll get blindsided by a 40-page questionnaire after you thought you "won."

The Playbook: How to Close Bank Deals

Get Compliance-Ready First

SOC 2 Type II is the fastest way to stop deals from dying in due diligence. ISO 27001 helps, and PCI DSS becomes mandatory if you touch payment data. The AICPA's SOC overview is worth bookmarking if you're starting the process.

Let's be honest - banks don't care about your slick UI. They care about uptime, incident history, auditability, and whether you'll still be around in five years. Put your reliability story on the first call, not the fifteenth.

Start Small: One Department, No Data

The cleanest first win is a department-level pilot that avoids sensitive data. Fewer stakeholders, fewer integrations, fewer reasons for risk to say no.

We've seen this pattern play out dozens of times, and the consensus on r/fintech backs it up: founders waste months pitching end-to-end solutions before realizing a smaller wedge would've gotten them in the door. Earn trust with a contained deployment, then expand. Every fintech startup selling software to financial institutions eventually learns this lesson - scope down first, scale up later.

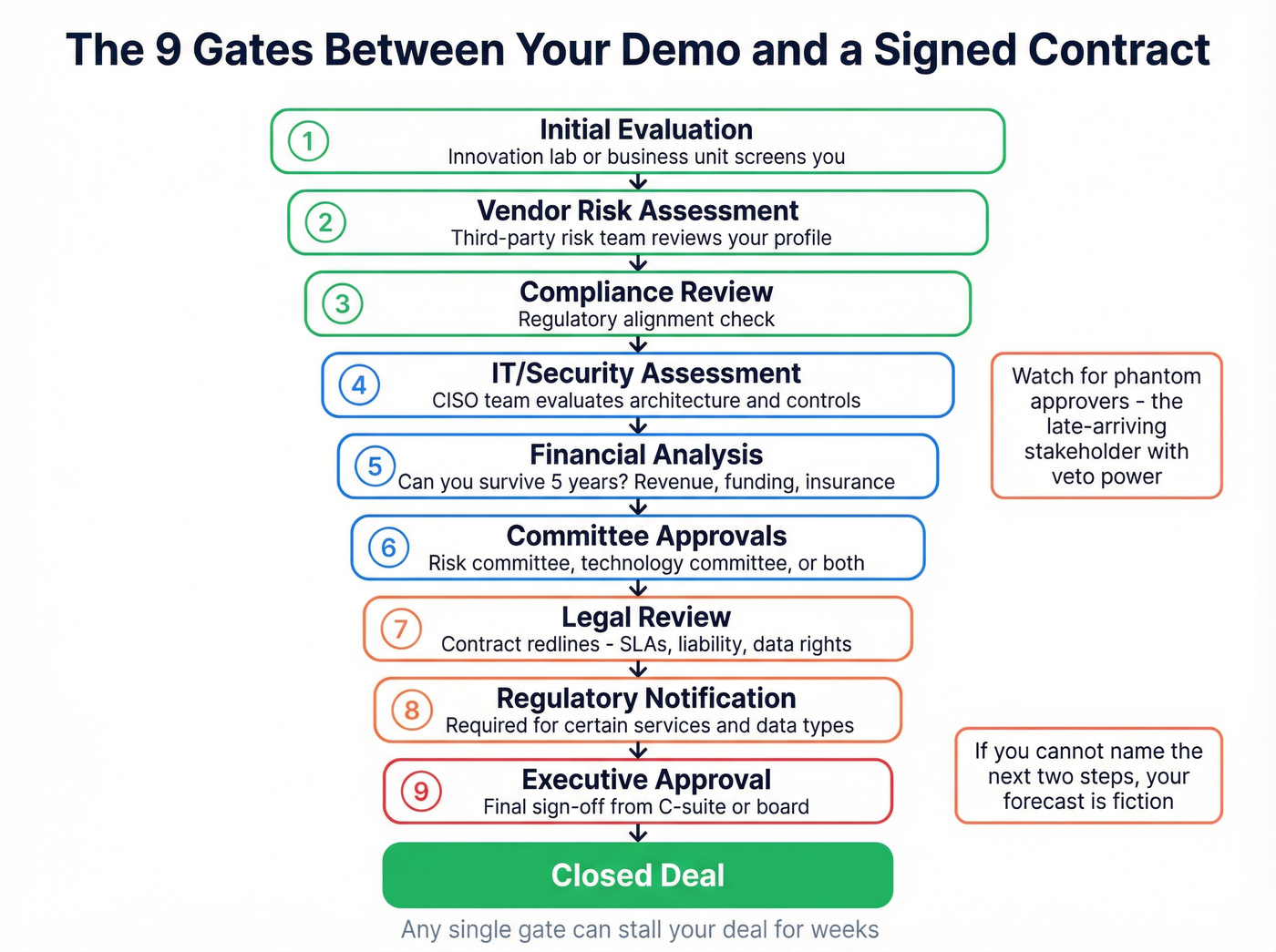

Run a MEDDPICC-Style Deal

You don't need to tattoo MEDDPICC on your forearm, but you need its discipline - especially around Decision Process. In banks, the real process usually looks like this:

Initial evaluation, then vendor risk assessment, compliance review, IT/security assessment, financial analysis, committee approvals, legal review, regulatory notification when applicable, and finally executive approval. That's nine gates, and any one of them can stall you for weeks.

Two practical rules. First, if you can't write down the next two steps in that chain, your forecast is fiction. Second, watch for phantom approvers - the late-arriving stakeholder with veto power, often someone in security, compliance, or a line-of-business exec who owns the budget but wasn't in the room during your demo.

Pick the Right Bank Tier

Don't start with JPMorgan.

| Community Bank | Regional Bank | Tier-1 Bank | |

|---|---|---|---|

| Economic Buyer | CFO / President | CFO / CTO / COO | CTO / CIO (via warm intro) |

| Typical Annual IT Budget | $500K-$5M | $50M-$500M+ | $500M+ |

| Stakeholders | 6-12 | 10-20 | 15-25+ |

| Sales Cycle | 6-18 months | 6-18 months | 12-24+ months |

| Entry Strategy | Direct outreach | Referral / ecosystem | Warm intro |

| Key Pain Point | Data silos, limited IT | Legacy modernization | Vendor consolidation |

Community banks often struggle with fragmented systems from years of adopting specialized tools that don't talk to each other. If you can simplify workflows or reduce operational risk without a massive rip-and-replace, you'll get real attention. For teams entering the banking market for the first time, this tier is almost always the smartest starting point - shorter cycles, fewer gatekeepers, and a genuine appetite for outside help that larger institutions rarely show until you've already proven yourself elsewhere.

Speak in Bank Math

Banks buy three things: efficiency ratio improvements (do more with the same headcount), risk reduction (fewer audit findings, fewer incidents, fewer exceptions), and revenue protection (retention, fraud reduction, faster underwriting, better cross-sell).

Bring a one-page ROI model to every second meeting. Not a deck - one page. If you can't quantify value, the bank will default to "build it" or "wait."

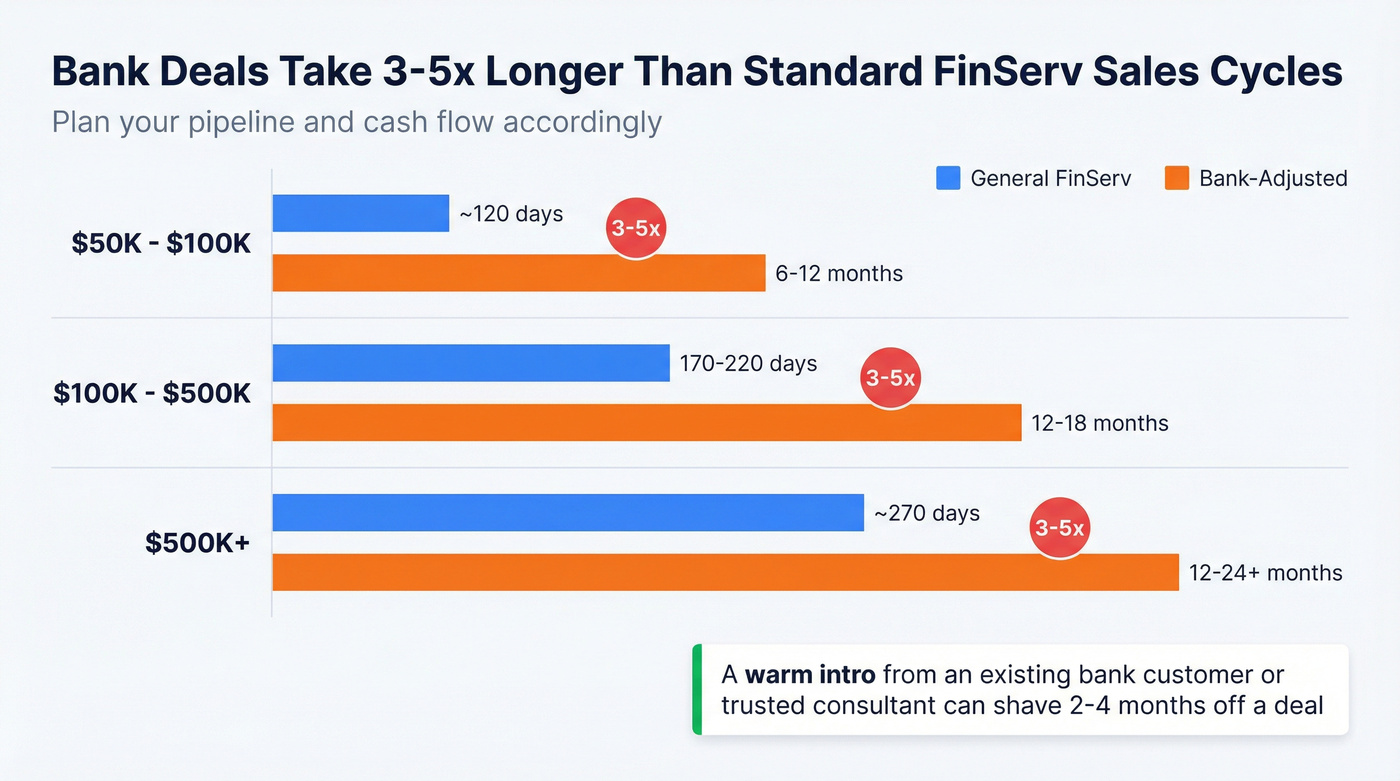

Timeline Expectations

A generic financial services sales-cycle benchmark floats around 98 days, but bank buying adds vendor risk, committees, and legal. Plan for 3-5x longer:

| Deal Size | General FinServ | Bank-Adjusted |

|---|---|---|

| $50K-$100K | ~120 days | 6-12 months |

| $100K-$500K | 170-220 days | 12-18 months |

| $500K+ | ~270 days | 12-24+ months |

Referrals still matter more than any outbound sequence. They don't just improve close rate - they cut calendar time by skipping trust-building steps you'd otherwise pay for in meetings. In our experience, a warm intro from an existing bank customer or a trusted consultant can shave 2-4 months off a deal.

Finding Bank Decision-Makers

Once you know the bank tier and the internal process, you still need the right people: CIO/CTO, CISO, Chief Risk Officer, procurement, and the line-of-business owner. In a 12-18 month cycle, bad contact data is a silent killer. Every bounced email and wrong title adds weeks.

This is where a B2B data platform earns its keep. Prospeo gives you 30+ filters to narrow by industry, department, seniority, and growth signals across 300M+ professional profiles, with 98% verified email accuracy and a 7-day data refresh cycle. It also layers Bombora intent data across 15,000 topics so you can prioritize banks already researching what you sell - instead of cold-calling institutions that aren't even in-market yet.

For banking outreach specifically, we've found the combination of financial services industry filters, C-suite seniority targeting, and intent signals cuts list-building time dramatically while keeping bounce rates under 4%.

Community banks have 6-12 stakeholders. Regionals have 20+. You need verified contact data for every one of them - not stale emails that bounce and torch your domain. Prospeo refreshes all 300M+ profiles every 7 days and delivers 98% email accuracy at $0.01 per lead.

Nine approval gates means nine contacts you can't afford to miss.

FAQ

How long does it take to close a bank deal?

Plan for 6-12 months at community banks, 12-18 months at regional banks, and 12-24+ months at tier-1 institutions. Vendor risk assessments, committee approvals, and legal review are the primary time sinks - build them into your forecast from day one rather than treating them as surprises.

What certifications do bank vendors need?

SOC 2 Type II is the baseline requirement for selling technology to banks. Expect requests for penetration test reports, business continuity/disaster recovery plans, incident response documentation, and appropriate insurance coverage. PCI DSS becomes mandatory if you handle payment data.

How do I find the right contact at a bank?

Map three core roles: Executive Sponsor (budget), Product Owner (requirements), and Project Manager (execution). Then identify veto players in security, risk, and procurement. Using a platform with financial services industry filters, C-suite seniority targeting, and verified contact data means you spend time on real stakeholders, not bounced messages.