Fintech Customer Acquisition Cost: 2026 Benchmarks and How to Cut Them

Your fintech customer acquisition cost number is wrong. Not because your math is bad - because the formula most teams use ignores 30-50% of the actual spend. Once you add KYC verification, sign-up bonuses, card issuance, and onboarding drop-off, a neobank reporting a "$50 consumer CAC" is really spending $85-$105 per active customer. And it's getting worse: CAC jumped 40-60% between 2023 and 2025 across financial services.

Quick version: Your real CAC is 30-50% higher than the benchmarks say once you include KYC, bonuses, and onboarding drop-off. SMB fintech CAC averages ~$1,450; enterprise runs $13k-$17k+ depending on vertical. Below you'll find the full benchmark tables, a true-cost breakdown, and five tactics that actually move the number.

How to Calculate Fintech CAC Correctly

The standard formula is simple enough: Total Acquisition Spend / New Customers = CAC. The problem is what you put in the numerator.

Most fintech teams calculate "marketing-only CAC" - ad spend, content costs, maybe SDR salaries. That's a vanity metric. Fully-loaded CAC includes every dollar spent to get a customer from stranger to active account. We've reviewed dozens of fintech CAC models, and the gap between marketing CAC and fully-loaded CAC is where most teams fool themselves.

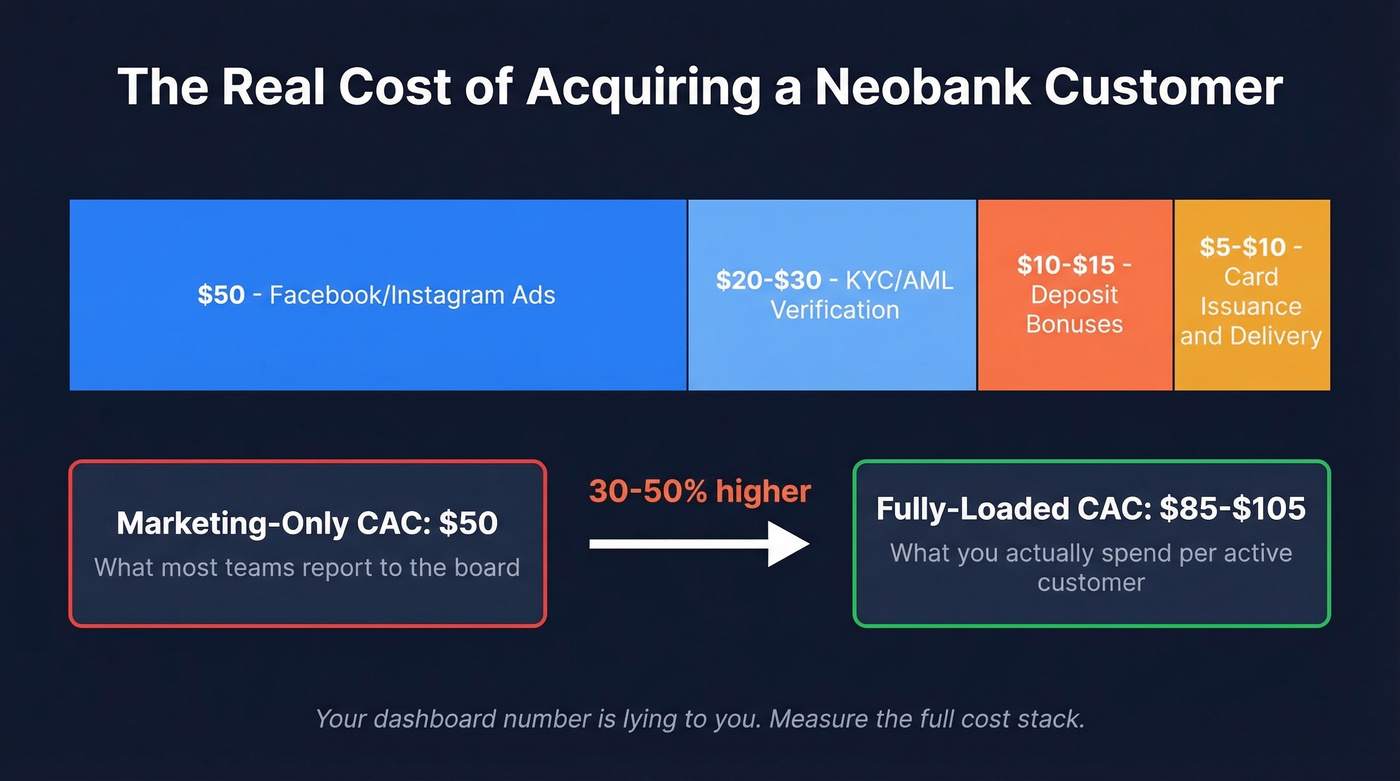

For a neobank, that cost stack looks something like this:

- $50 - Facebook/Instagram ads to drive the signup

- $20-$30 - KYC/AML identity verification

- $10-$15 - Deposit bonuses or cash incentives

- $5-$10 - Card issuance and delivery

That's $85-$105 in true cost per acquired customer, and the marketing-only number only captured $50 of it. If you're reporting a $50 CAC to your board but spending $105 to get each customer active, you're making decisions on bad data.

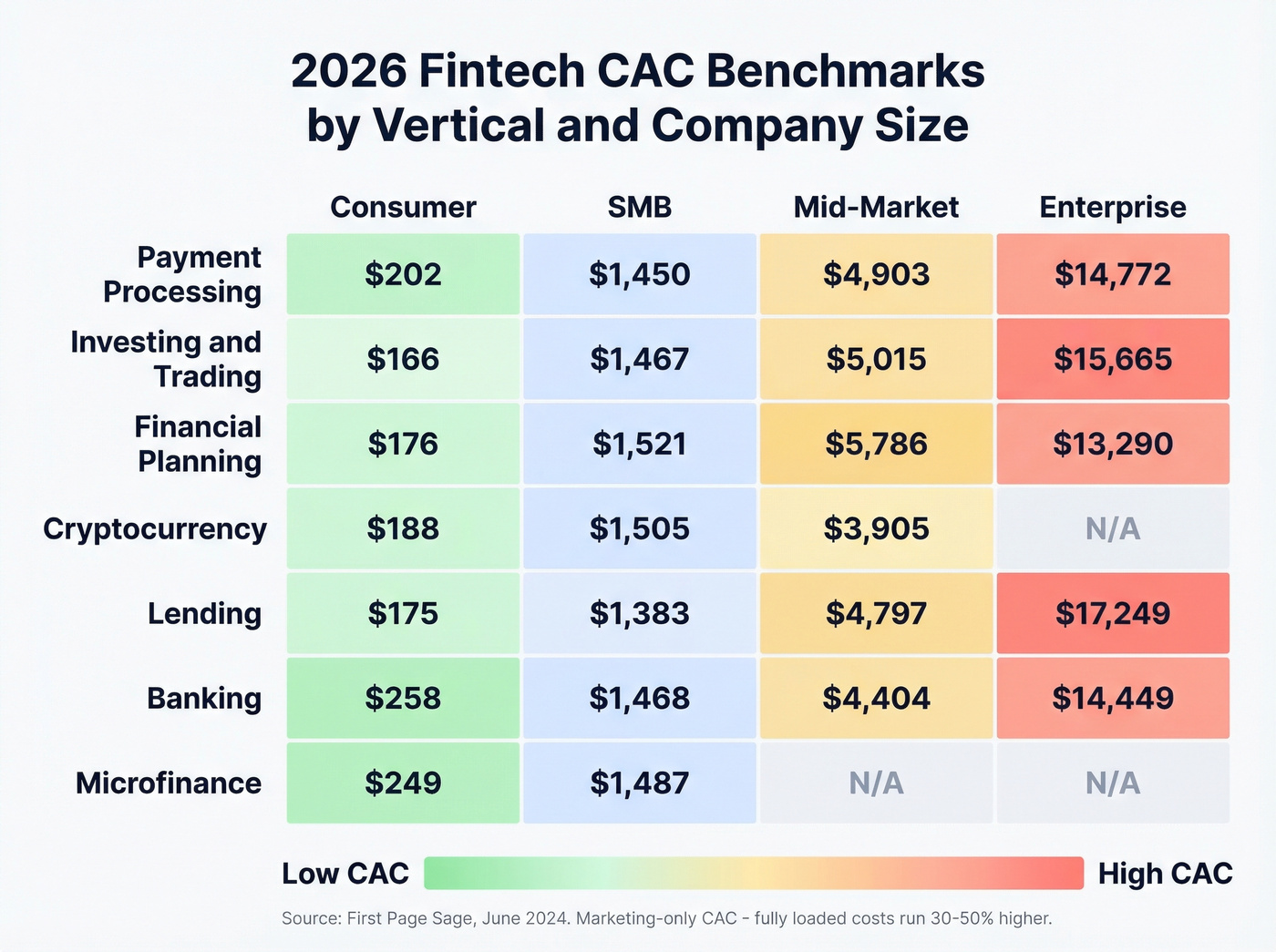

2026 CAC Benchmarks by Vertical

The most widely cited fintech CAC dataset comes from First Page Sage, published June 2024 and still one of the most thorough public datasets available. Two caveats: these are marketing-only CAC figures that exclude compliance and onboarding costs, and they skew toward companies investing in organic channels.

Average CAC by Vertical and Company Size

| Vertical | Consumer | SMB | Mid-Market | Enterprise |

|---|---|---|---|---|

| Payment Processing | $202 | $1,450 | $4,903 | $14,772 |

| Investing & Trading | $166 | $1,467 | $5,015 | $15,665 |

| Financial Planning | $176 | $1,521 | $5,786 | $13,290 |

| Cryptocurrency | $188 | $1,505 | $3,905 | N/A |

| Lending | $175 | $1,383 | $4,797 | $17,249 |

| Banking | $258 | $1,468 | $4,404 | $14,449 |

| Microfinance | $249 | $1,487 | N/A | N/A |

The SMB column clusters tightly around $1,450 regardless of vertical - that's the number you'll see cited everywhere as the average for fintech companies selling to small businesses. Enterprise lending stands out at $17,249, which makes sense given the sales cycle complexity and compliance overhead. At the other extreme, Cash App's CAC sits around $10 as Block scaled paid marketing spend, though replicating that kind of network effect is the hard part.

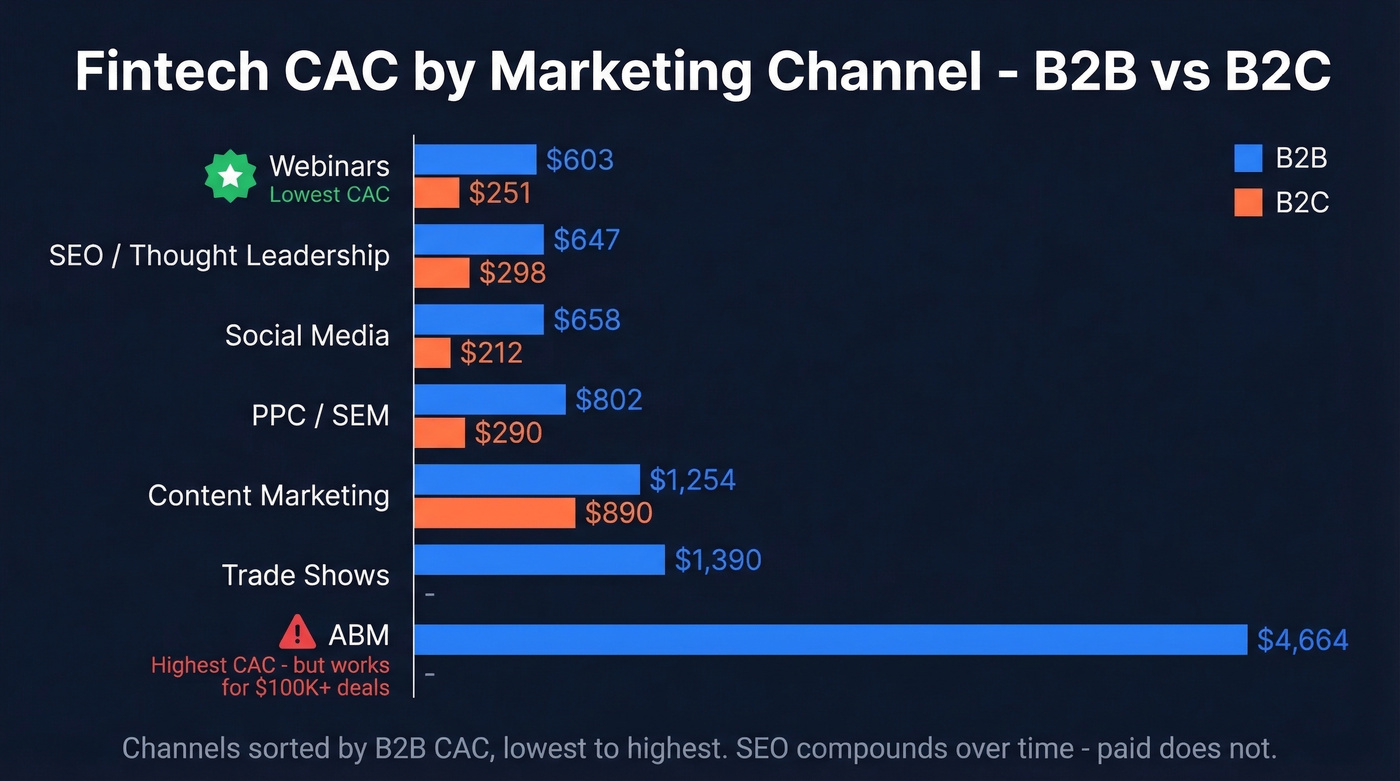

CAC by Marketing Channel

| Channel | B2B | B2C |

|---|---|---|

| SEO / Thought Leadership | $647 | $298 |

| PPC / SEM | $802 | $290 |

| Social Media | $658 | $212 |

| Content Marketing | $1,254 | $890 |

| Webinars | $603 | $251 |

| ABM | $4,664 | - |

| Trade Shows | $1,390 | - |

Webinars are the lowest-CAC channel in both B2B and B2C fintech in this dataset. SEO is close behind - and it's the channel that compounds the most over time. ABM is the most expensive at $4,664 per acquired customer, though for enterprise deals worth $100K+, that math still works.

ABM costs $4,664 per fintech customer. Most of that spend is wasted on bad contact data that never reaches decision-makers. Prospeo delivers 98% verified emails at $0.01 each - with 30+ filters including funding stage, headcount growth, and technographics to target the exact fintech buyers worth your CAC.

Stop inflating your CAC with bounced emails and dead-end contacts.

Why Acquisition Costs Keep Rising

Three forces are compounding, and none of them are slowing down.

First, across digital businesses broadly, acquisition costs have surged 222% over the past decade - and fintech isn't exempt. Digital ad costs climbed another 5.13% in 2025 alone.

Second, compliance costs keep stacking. The average large financial institution now spends $72.9M annually on AML/KYC operations. Even for smaller fintechs, identity verification adds $20-$30 per customer before they've generated a dollar of revenue. AI adoption in KYC workflows jumped from 42% to 82% in a single year, signaling that the complexity is growing even as automation tries to keep pace.

Third, incentive inflation is real. SoFi's referral bonuses - $75 to the referrer, $25 to the new member - combined with direct deposit incentives of up to $250 can push the acquisition cost to around $350 per banking customer. When every neobank is offering cash to switch, the floor keeps rising.

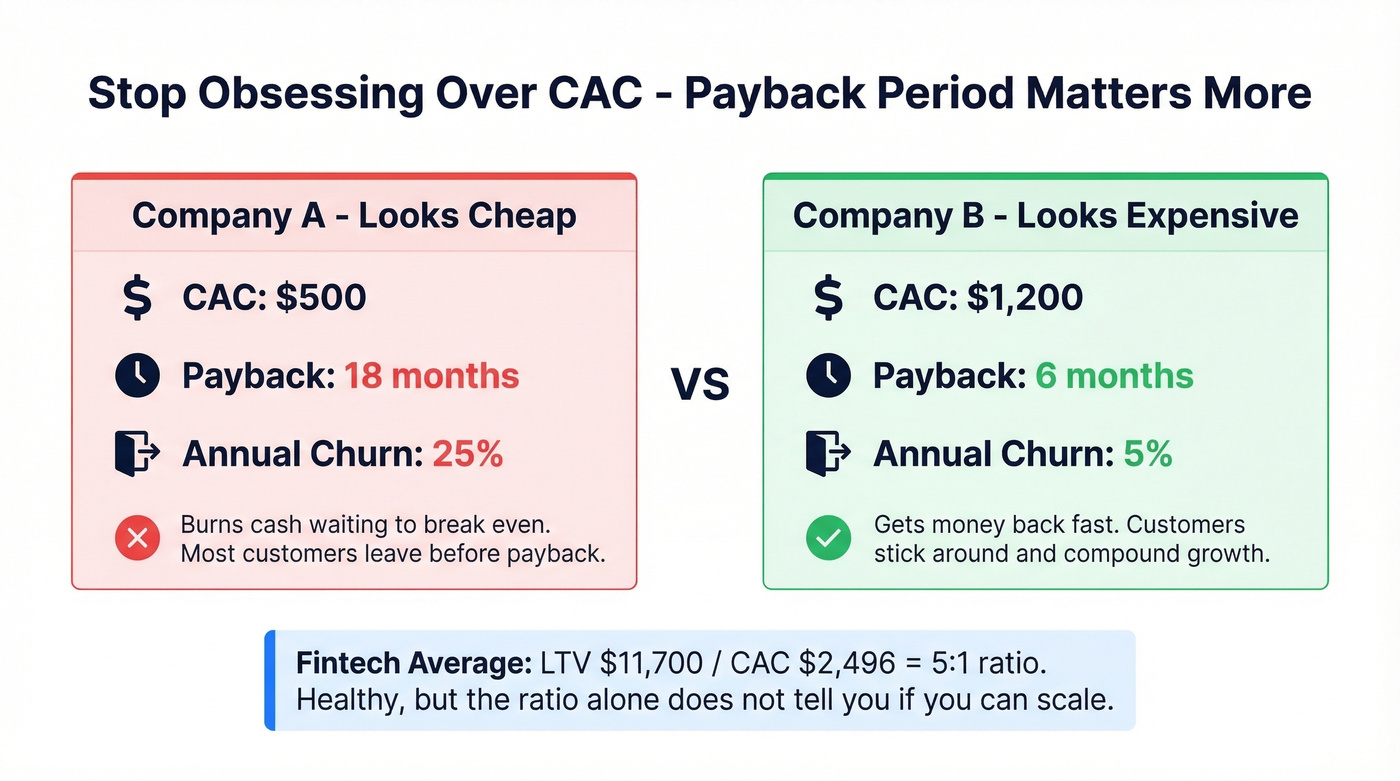

LTV:CAC Ratio and Payback Period

| Metric | Fintech Average |

|---|---|

| LTV | $11,700 |

| CAC | $2,496 |

| LTV:CAC | 5:1 |

A 5:1 LTV:CAC ratio looks healthy against the common benchmark of 3:1 minimum and 4:1 ideal.

Here's the thing, though: stop obsessing over CAC in isolation. A $500 CAC with an 18-month payback period and 25% churn is worse than a $1,200 CAC with 6-month payback and 5% churn. The second company gets its money back faster, retains more customers, and compounds growth. Payback period is the metric that actually determines whether your unit economics let you scale - especially if you're capital-constrained and can't afford to wait two years to break even on each customer.

Let's be honest: most fintech teams would grow faster by doubling their CAC on high-LTV segments than by trying to cut CAC across the board. The obsession with lowering the number leads to cheap, low-intent traffic that churns in 90 days. Spend more on the right customers.

5 Ways to Reduce Fintech CAC

Sequence matters here. Fix onboarding first (week 1-2), then build partnerships and referrals (month 1-2), then shift budget to SEO (month 2+).

Fix Your Onboarding Funnel First

70% of financial institutions lost clients due to slow onboarding in 2025 - up from 48% just two years earlier. Every customer lost to onboarding friction is a customer you already paid to acquire.

Do the math: if your onboarding completion rate is 80%, your effective CAC is 25% higher than your reported number. Reducing form fields or adding pre-fill can improve completion rates by around 15%. Fix the funnel before you spend another dollar on ads.

Build Partnership Distribution

One fintech founder shared on r/fintech how Affiniti Finance partnered with 17 trade organizations representing 2M+ small businesses and grew monthly GTV from $200K to $3M in three months. That's not a rounding error.

The US has 14,000+ trade organizations representing 20M SMBs. These partnerships let you borrow trust instead of buying attention, and the economics can approach negative CAC through revenue-share structures. If you're a B2B fintech ignoring trade associations, you're leaving the cheapest distribution channel on the table.

Structure Referral Programs That Don't Spiral

PayPal's early referral program - $10 to referrer plus $10 to the referred user - cost $10M+ total but seeded massive growth. SoFi's incentive stack, at around $350 per user, shows how quickly bonuses can inflate acquisition cost.

The lesson: tie referral rewards to funded accounts or high-LTV actions, not raw signups. A $25 bonus for an account that never gets funded is pure waste.

Flip Your Budget Toward SEO

Many fintechs still skew heavily toward paid channels. This is backwards if you care about compounding economics.

SEO sits among the lowest-CAC channels at $298 for B2C and $647 for B2B. Paid gets you volume today; SEO builds a compounding asset that reduces acquisition costs over time. In our experience, teams cut blended CAC by 30%+ within a year simply by shifting budget toward organic content. Affiliate and performance marketing channels deserve a look too - they're pay-for-results by design and remain underused in fintech compared to e-commerce.

Clean Up Your Outbound Data (B2B Fintech)

Picture this: your SDR team sends 500 emails on Monday. By Wednesday, 80 have bounced, 60 went to people who left the company months ago, and your domain reputation just took a hit that'll haunt deliverability for weeks. That wasted effort shows up in your CAC as meetings that never happened and pipeline that never materialized.

Prospeo verifies emails at 98% accuracy on a 7-day refresh cycle, starting free - at ~$0.01/email, the data itself costs almost nothing compared to the waste from bad data. One customer, Meritt, saw bounce rates drop from 35% to under 4% and tripled their pipeline from $100K to $300K per week after switching. Cleaning your contact list is the fastest single fix for B2B fintech outbound CAC.

Your fintech sales team is burning budget on prospects who never pick up. Prospeo's 125M+ verified mobile numbers hit a 30% pickup rate - 3x the industry average. Pair that with intent data tracking 15,000 topics to reach buyers already evaluating financial products, and your payback period shrinks fast.

Reach fintech decision-makers on the first dial, not the fifteenth.

Your real fintech customer acquisition cost is higher than your dashboard says. Measure the full cost stack first, fix onboarding leaks second, then rebuild your channel mix around the numbers that actually compound. The teams that get this right don't just lower CAC - they make every dollar of spend go further.

For a broader baseline on CAC definitions and what belongs in the numerator, see our guide to cost to acquire customer.

If you’re tightening the model, it also helps to track funnel metrics and run a proper churn analysis so CAC doesn’t get “optimized” into higher churn.

On the B2B side, improving email deliverability and using email reputation tools can prevent CAC creep from spam placement and bounces.

If you’re rebuilding outbound, start with sales prospecting techniques and a clean lead generation workflow so SDR time maps to pipeline.

FAQ

What is a good CAC for fintech?

SMB fintech averages ~$1,450; consumer runs $166-$258 depending on vertical. A "good" CAC depends on your LTV:CAC ratio - aim for at least 3:1 with payback under 12 months. A $2,000 CAC is perfectly fine if lifetime value exceeds $8,000 and churn stays below 10%.

What is the average CAC for fintech?

Average fintech CAC varies widely by segment: consumer products range from $166 to $258, SMB clusters around $1,450, and enterprise deals run $13,000-$17,000+. These are marketing-only figures - fully-loaded costs including KYC, bonuses, and onboarding run 30-50% higher.

Why is fintech CAC so high?

KYC/AML compliance adds $20-$30 per user, neobank incentive wars push costs up to $350 per customer at companies like SoFi, digital ad costs have risen 222% over the decade, and onboarding drop-off inflates fintech CAC 30-50% beyond what marketing-only benchmarks capture.

How can B2B fintechs reduce outbound acquisition costs?

Start with data quality - verified contact data eliminates wasted outreach and protects domain reputation, directly lowering cost per meeting. Then pair clean outbound with SEO ($647 B2B CAC) and trade-organization partnerships for long-term, compounding CAC reduction.