How to Build a Fintech Go-to-Market Strategy That Actually Works

Fintech revenues grew 21% in 2024 while incumbents managed 6%. Yet only 3% of global banking and insurance revenue has been penetrated by fintechs. The graveyard of startups that built great products and couldn't sell them keeps growing - and in 2026, a strong fintech go-to-market strategy is the difference between scaling and stalling.

One founder on r/fintech captured the pattern perfectly: strong traction during six weeks of door-to-door selling, then growth flatlined the moment they paused outbound. Six clients, roughly $20K ARR, and no idea how to reach banks efficiently. That's a GTM problem, not a product problem.

The Short Version

Your GTM motion depends on your buyer. PLG for SMB self-serve tools, SLG for enterprise and regulated workflows, hybrid as you scale. Compliance isn't a blocker; it's your moat. And budget for real CAC: enterprise fintech customers cost $13K-$17K to acquire, while SMB costs land around $1,400-$1,500.

What a Fintech GTM Strategy Actually Covers

It's not a marketing plan. It's a decision sequence: validate PMF, build compliance infrastructure, define ICP, choose your motion, select channels, build your sales process, then measure what matters. Each step constrains the next.

Here's the thing - generic advice is useless. A fraud detection company selling to banks has nothing in common with an expense management tool for SMBs. SMB deals can close in 1-3 months; enterprise fintech deals often run 9-18 months, sometimes longer if the compliance review gets ugly. The only useful framework forces you to make those distinctions early.

Prerequisites: PMF and Compliance

Validate PMF First

If you're pre-PMF, your only GTM motion is founder-led sales. Period. QED Investors' B2B fintech framework makes this explicit - the pre-PMF stage is about learning from customers, not scaling channels.

That Reddit founder who stalled at $20K ARR admitted underpricing "hurt perceived value." Banks associate price with seriousness. If your enterprise prospects aren't flinching at your pricing, raise it.

Compliance as GTM Infrastructure

Regulation is the product - not a constraint on it. Coinbase learned this the hard way with a EUR 3.3M fine from the Dutch Central Bank. Financial institutions have faced cumulative fines exceeding $56 billion for AML violations.

For MVP-stage fintechs: scope features to avoid triggering heavy regulation early, use sponsor bank or facilitator models, and narrow your geography before expanding. SOC 2 readiness and audit work often lands in the $30K-$150K range. That's not just a cost - it's a sales asset. We've seen early-stage teams close their first enterprise deal specifically because they could hand over a SOC 2 report when the competitor couldn't.

Define Your Ideal Customer Profile

B2B and B2C fintech GTM strategies share almost nothing. B2C is activation funnels and retention loops. B2B enterprise means navigating a stakeholder map that includes the CFO, CIO/CTO, compliance, legal, ops, and product teams - six or more people who can say no, and any one of them can kill the deal at the last minute.

Only 56% of people worldwide trust financial services companies, and 60% of consumers express concerns about data security and privacy. Your entire go-to-market approach should be engineered to reduce perceived risk faster than competitors.

Segment by buyer size because the economics differ dramatically. An SMB payments tool closes in 1-3 months; an enterprise lending platform takes 9-18 months. If your deal sizes sit below $15K, you probably don't need an enterprise sales motion at all. Build a self-serve product, invest in content and partnerships, and save yourself 12 months of painful sales cycles.

Geography matters too. LATAM fintech funding hit $2.6B in recent years, and non-US fintechs entering the American market face an entirely different regulatory and competitive landscape. Narrow your geography before expanding - the compliance burden alone justifies it.

You just defined your fintech ICP and chose your GTM motion. Now you need to reach those buyers. Prospeo's 30+ search filters - including funding stage, headcount growth, and technographics - let you build fintech-specific prospect lists with 98% email accuracy and under 4% bounce rates.

Stop burning domain reputation on bad data. Start with contacts that connect.

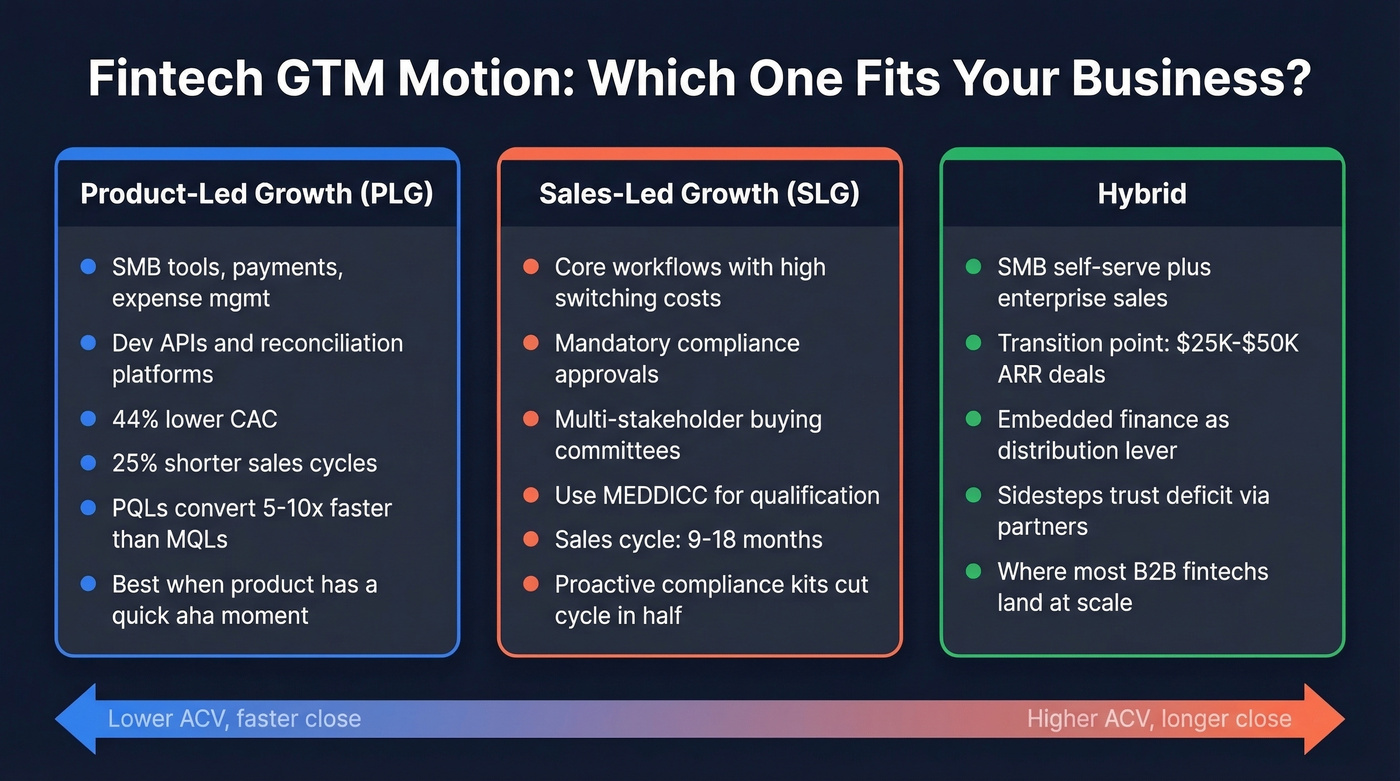

Choosing Your GTM Motion

Product-Led Growth fits SMB tools, payments, expense management, dev APIs, and reconciliation platforms. PLG companies report 44% lower CAC, 25% shorter sales cycles, and product-qualified leads that convert 5-10x faster than MQLs. If your product can deliver an "aha" moment inside a free trial, PLG is your strongest lever.

Sales-Led Growth fits core workflows with high switching costs, mandatory compliance approvals, and multi-stakeholder buying committees. Use MEDDICC for enterprise qualification. One fraud detection fintech cut their sales cycle from 18 months to 9 by proactively providing compliance readiness kits before prospects asked. The buyer readiness funnel runs: Trust Formation, Risk Reduction, Internal Alignment, Decision Justification. Skip a step and the deal stalls.

Hybrid is where most B2B fintechs land as they move upmarket. Let SMB customers self-serve while building enterprise sales for larger accounts. The transition point is usually when deal sizes cross $25K-$50K ARR. Embedded finance - distributing your product through a partner's platform rather than selling direct - is a powerful hybrid lever that sidesteps the trust deficit entirely.

Channel Strategy and CAC Benchmarks

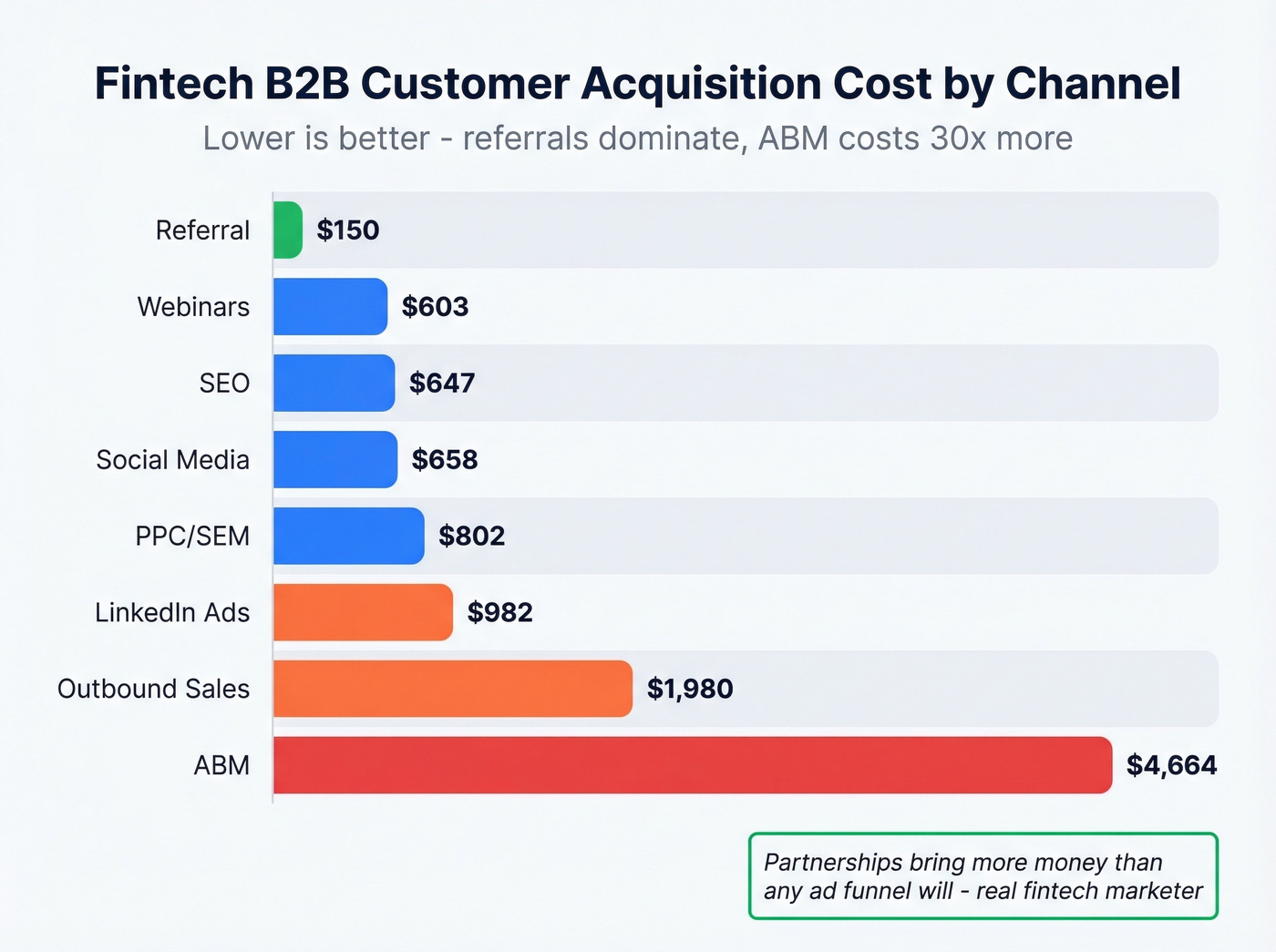

CAC has inflated 40-60% between 2023 and 2025, driven by competition, privacy regulations, and attribution challenges. A fintech marketing operator on r/growthmarketing put it well: "Partnerships will bring you more money than any of your ad funnels will." In our experience, the best-performing GTM motions lean heavily on ecosystem partnerships and referrals, not paid channels.

| Channel | B2B CAC |

|---|---|

| Referral | $150 |

| Webinars | $603 |

| SEO | $647 |

| Social Media | $658 |

| PPC/SEM | $802 |

| LinkedIn Ads | $982 |

| Outbound Sales | $1,980 |

| ABM | $4,664 |

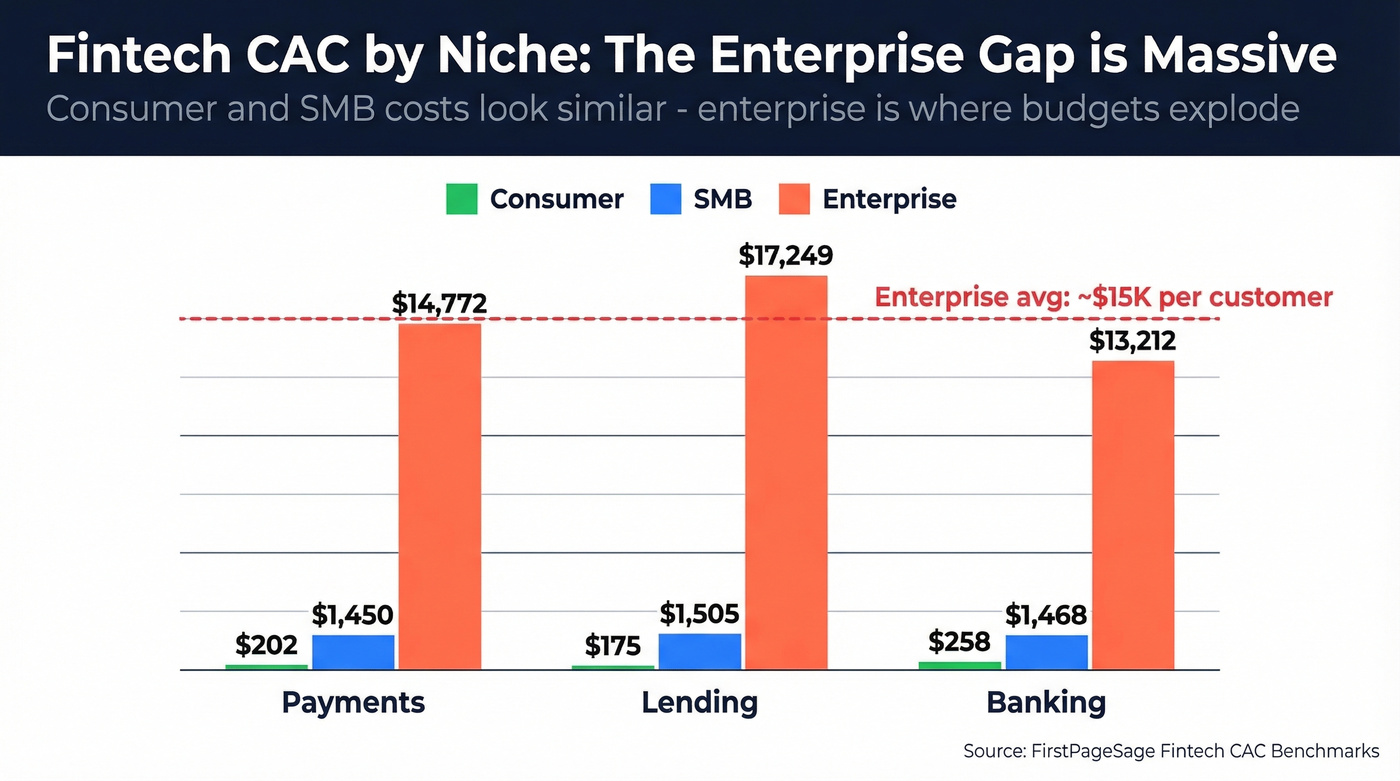

CAC by Fintech Niche

| Niche | Consumer | SMB | Enterprise |

|---|---|---|---|

| Payments | $202 | $1,450 | $14,772 |

| Lending | $175 | $1,505 | $17,249 |

| Banking | $258 | $1,468 | $13,212 |

These numbers from FirstPageSage explain why channel selection matters so much. An enterprise lending company burning $17K per customer can't afford to experiment with channels that don't convert.

Build Your Prospect List

After locking your ICP, the gap between strategy and execution is contact data. In fintech, bad data doesn't just waste money - it damages your domain reputation. When your GTM depends on trust, bouncing 15% of your outbound emails signals the opposite.

Prospeo's B2B database covers 300M+ professional profiles with 30+ search filters, including buyer intent across 15,000 topics, technographics, and job changes. The 98% email accuracy on a 7-day refresh cycle matters when fintech enterprise deals involve 6+ stakeholders - you can't afford to miss the compliance officer because their email bounced. The free tier (75 emails + 100 Chrome extension credits/month) is enough to test your ICP hypotheses before committing budget.

For inbound, set a speed-to-lead SLA: contact demo requests within 15 minutes during business hours. For outbound, plan 5-7 touches over 10 days (use these sales follow-up templates to stay consistent). Enterprise buyers interpret response time as a proxy for how you'll handle their account.

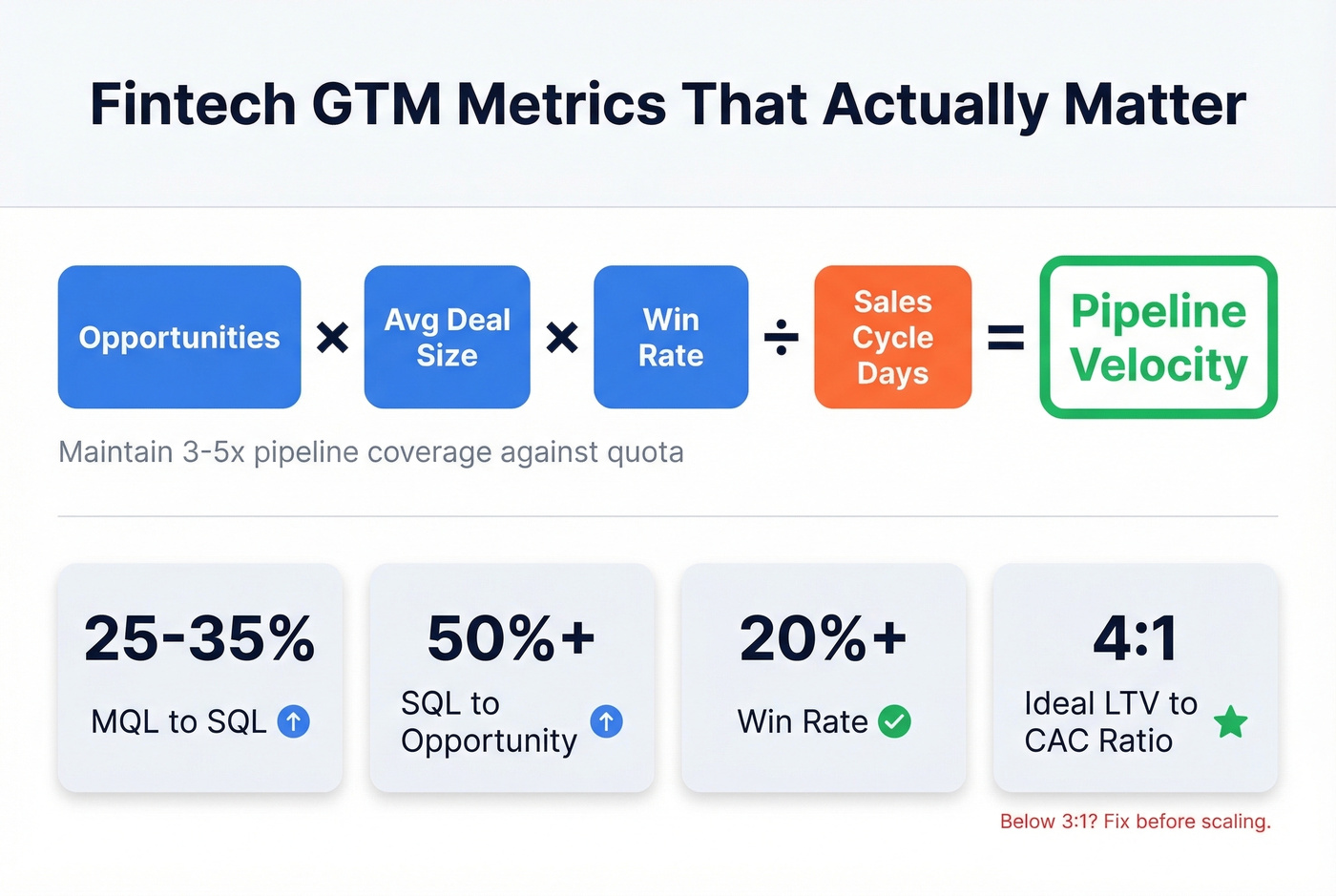

Metrics That Matter

Pipeline velocity ties everything together: (Opportunities x Average deal size x Win rate) / Sales cycle days. Maintain 3-5x pipeline coverage against quota.

Baseline conversion benchmarks: MQL to SQL 25-35%, SQL to Opportunity 50%+, win rate above 20%. But don't stop at MQLs. Track activation rates, CAC payback period, and - critically - conversion through compliance-heavy steps like security reviews and sandbox access. The ideal LTV:CAC ratio is 4:1. Below 3:1, your unit economics don't support scaling. Fix the denominator or the numerator before pouring money into channels.

If you need a tighter measurement layer, build a simple funnel metrics dashboard and review it weekly.

Five GTM Mistakes That Kill Fintechs

Pausing outbound. That Reddit founder's pipeline dried up in six weeks. Outbound isn't a campaign - it's a continuous motion. The moment you stop, your pipeline decays.

Underpricing to win early logos. $20K ARR with six clients means roughly $3,300 per customer. Banks don't trust cheap software. We've watched founders spend months trying to move upmarket after anchoring low - it's far harder than starting at the right price.

Treating compliance as a blocker instead of a moat. Narrative and perspective-driven content passes legal review far more easily than direct product claims. Build compliance into your messaging, not around it.

Scaling before PMF. This is the top fintech failure mode. Pouring money into channels before validating willingness to pay just accelerates the burn.

Sending outbound on bad contact data. In fintech, domain reputation is brand reputation. Whatever verification tool you use, verify before you send (see email bounce rate benchmarks and fixes). A single batch of bad emails can tank your sender score for weeks.

Enterprise fintech deals cost $13K-$17K to acquire. Every bounced email and wrong number inflates that CAC further. Prospeo refreshes 300M+ profiles every 7 days - not 6 weeks - so your outbound hits real decision-makers at banks, lenders, and payment companies right now.

Cut your fintech CAC by reaching verified buyers on the first touch.

FAQ

How long does it take to launch a fintech go-to-market strategy?

Pre-PMF fintechs should expect 3-6 months of founder-led sales before formalizing GTM. Post-PMF, building a repeatable motion takes another 2-4 months. Enterprise sales cycles add 9-18 months on top, so plan runway accordingly.

What's the biggest GTM mistake fintech founders make?

Scaling channels before validating product-market fit. The second most common is underpricing to win early logos - anchoring at $3K/customer tanks perceived value with enterprise buyers and makes moving upmarket significantly harder.

What channels work best for fintech customer acquisition?

Referral programs ($150 CAC) and partnerships consistently outperform paid channels. For enterprise, ABM is expensive ($4,664 CAC) but effective when deal sizes justify it. SEO ($647) and webinars ($603) offer the best mid-funnel economics for most B2B fintechs.

Should I use PLG or SLG for my fintech startup?

It depends on your buyer and deal size. If you're selling self-serve tools to SMBs with deal sizes under $15K, PLG is almost always the right call. For enterprise workflows with compliance requirements and multi-stakeholder committees, you need SLG. Most B2B fintechs end up running a hybrid motion as they scale upmarket past the $25K-$50K ARR threshold per account.