Involuntary Churn: The Silent Revenue Leak and How to Stop It

You just pulled your churn report and the number looks terrible. But when you segment it - voluntary vs. involuntary - you realize 35-40% of those "churned" customers never wanted to leave. They didn't cancel. Their card expired, or their bank flagged a $49 charge as suspicious, and your system quietly let them go. One SaaS founder on r/SaaS reported losing 4-7% of MRR monthly from payment declines alone. Another segmented their churn and found 38% of it was involuntary - customers they could've saved with the right recovery stack.

Involuntary churn is the highest-ROI retention problem you can solve. Faster, cheaper, and more predictable than fixing voluntary churn. Here's the complete playbook.

Quick Summary

Customers lost to payment failures - not dissatisfaction - account for 20-40% of all churn in most subscription businesses. The fix is a stack: pre-dunning notifications, a dunning email cadence, smart retries, card updaters, network tokenization, and a contact data quality audit. Recovered subscribers stick around ~7 more months on average. Below you'll find segmented benchmarks, a day-by-day dunning sequence, and the advanced tactics nobody else covers.

What Is Involuntary Churn?

This type of churn happens when a subscription ends because of a payment failure - not because the customer decided to leave. The customer still wants your product. Their card expired, their bank declined the charge for insufficient funds, a fraud filter tripped, or the issuer returned a "generic decline" code that tells you nothing.

These failures split into two buckets: soft declines and hard declines. Soft declines are temporary - insufficient funds, processor timeouts, rate limits. Hard declines are permanent - closed accounts, stolen cards, invalid numbers. That distinction drives your entire retry strategy.

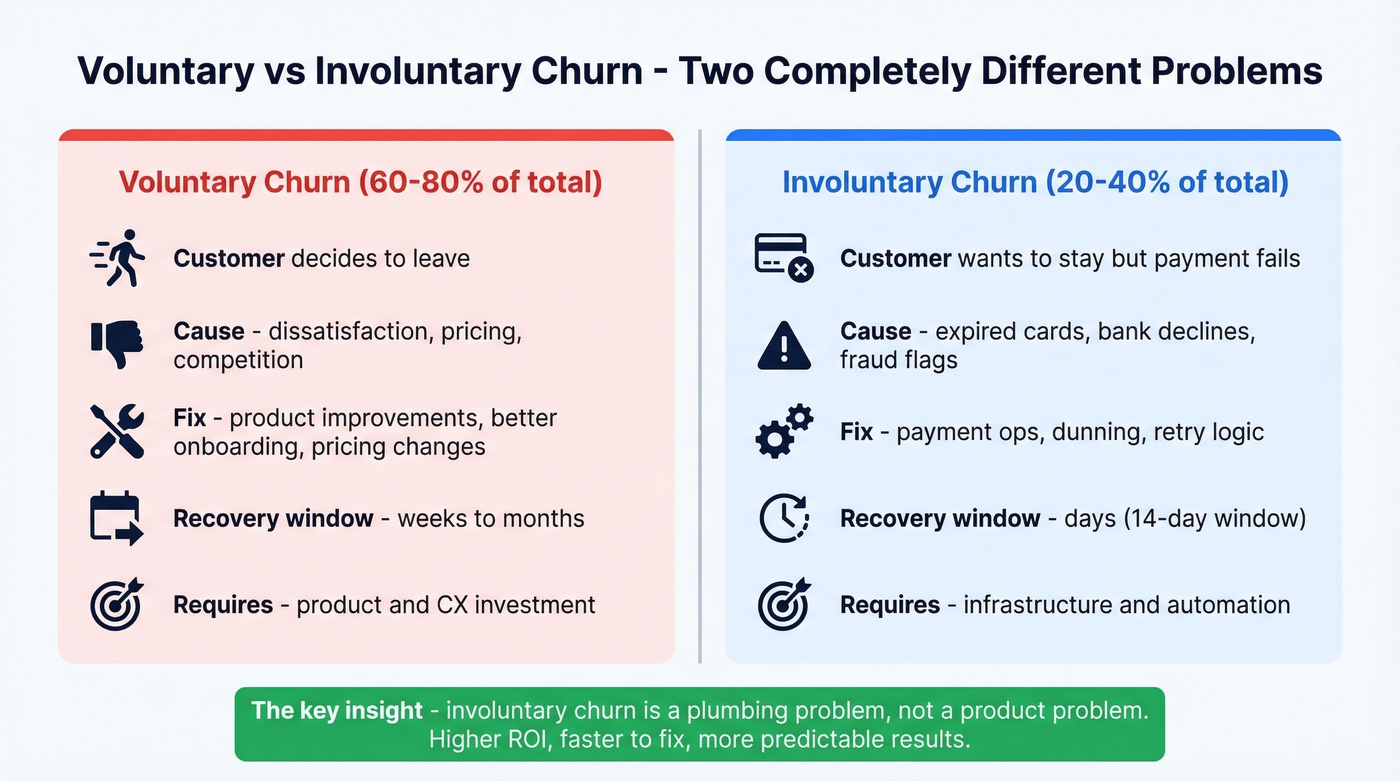

Understanding voluntary vs. involuntary churn matters because the fix for each is completely different. Voluntary churn requires product improvements, better onboarding, pricing changes. Payment-related churn requires infrastructure. You're solving a plumbing problem, not a product problem. And here's what makes it worse: customers locked out during payment failures often churn voluntarily afterward. The payment failure triggers the cancellation decision they wouldn't have made otherwise.

| Voluntary Churn | Involuntary Churn | |

|---|---|---|

| Cause | Customer decides to cancel | Payment fails |

| Customer intent | Wants to leave | Wants to stay |

| Fix | Product, pricing, CX | Payment ops, dunning |

| Recovery window | Weeks to months | Days (14-day window) |

| Typical share | 60-80% of total churn | 20-40% of total churn |

The fact that "generic decline" accounts for roughly 40% of all error codes tells you everything about how broken the payment failure ecosystem is.

Benchmarks by Segment

Let's ground this in numbers. Benchmark data across 1,500+ subscription sites shows an overall churn rate of 3.27%, split into 2.41% voluntary and 0.86% involuntary. That involuntary slice looks small as a percentage - until you realize it's pure preventable revenue loss. A broader survey of 1,200 subscription businesses shows companies risk losing 5.6-8.3% of their subscriber base each month to failed-payment churn.

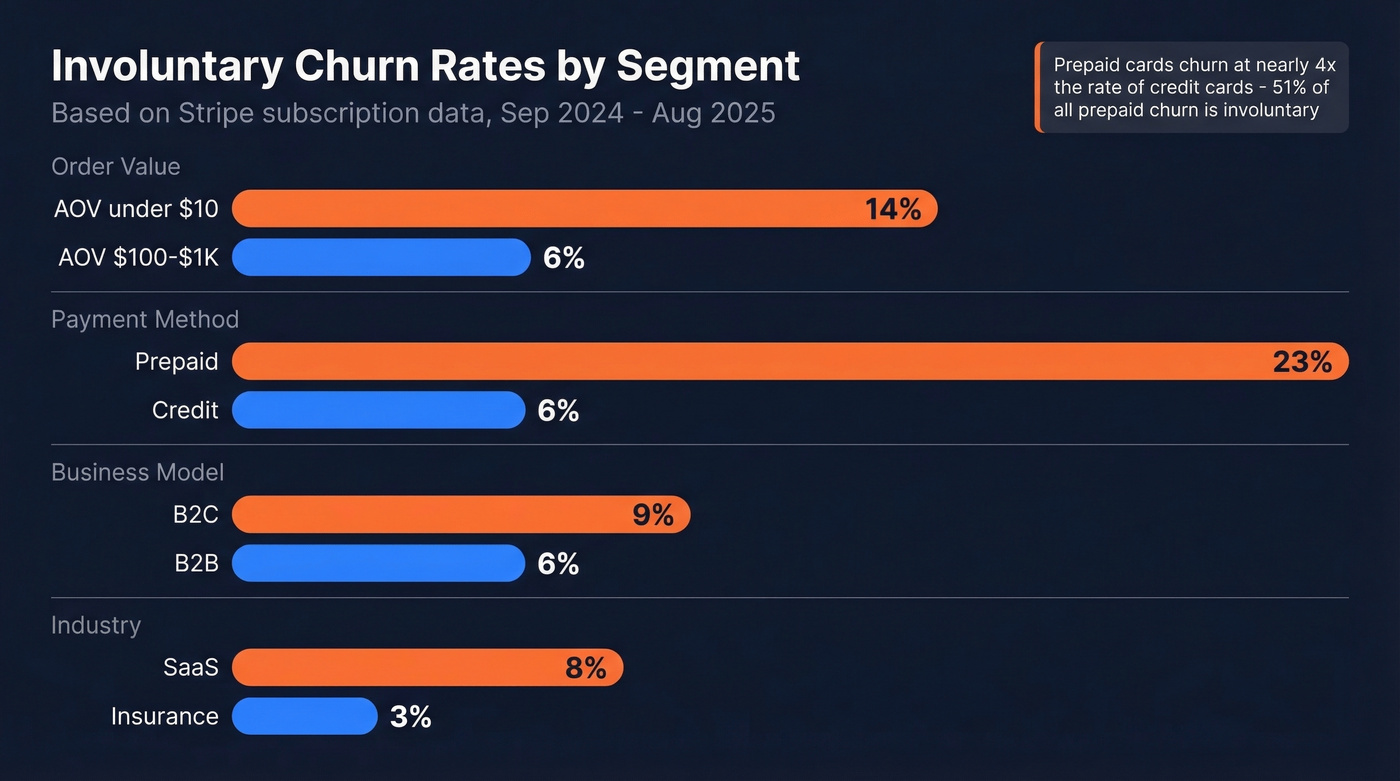

The more useful data comes from a FlyCode analysis of Stripe subscription transactions covering September 2024 through August 2025, which segments by the dimensions that actually matter.

| Segment | Dimension | Involuntary Churn Rate |

|---|---|---|

| AOV < $10 | Order value | 14% |

| AOV $100-$1K | Order value | 6% |

| Prepaid | Payment method | 23% |

| Credit | Payment method | 6% |

| B2C | Business model | 9% |

| B2B | Business model | 6% |

| SaaS | Industry | 8% |

| Insurance | Industry | 3% |

Two things jump out. First, prepaid card subscribers churn involuntarily at nearly 4x the rate of credit card subscribers - and 51% of all prepaid churn is involuntary. If your customer base skews toward prepaid or debit, this is your single biggest lever. Second, low-AOV subscriptions under $10 see 14% involuntary churn vs. 6% for $100-$1K subscriptions. Cheaper plans attract payment methods with higher failure rates.

We've seen this firsthand when helping teams segment churn for the first time - the reaction is almost always shock at how much of it is payment-related. The broader framing: DTC subscription businesses average ~6.5% total churn vs. ~3.8% for B2B. Anything above your segment benchmark signals a recovery gap worth closing.

You're fixing payment failures - but is outdated contact data killing your dunning emails? If your customer emails bounce, no retry logic or dunning sequence can save that subscriber. Prospeo's 7-day data refresh and 98% email accuracy ensure your recovery emails actually land.

Your dunning sequence is worthless if the email address is dead.

The Business Case

Here's the math that makes this worth prioritizing above almost everything else on your roadmap.

A recovered monthly subscription continues for ~7 months on average after recovery. If your average subscription is $50/month, every recovered customer is worth $350 in downstream revenue - for the cost of a few emails and a retry. Automated recovery features across major billing platforms helped merchants recover $6.5B in 2024, and churn management techniques deliver an average 16X ROI. In the real world, founders see big lifts fast - the same r/SaaS thread points to a benchmark showing that fixing payment-failure churn alone can boost revenue 8.6% in the first year.

If your average deal size is under $15K and you haven't segmented voluntary vs. involuntary churn yet, you're almost certainly leaving more revenue on the table from payment failures than from product dissatisfaction. Fix the plumbing before you redesign the kitchen.

Six Levers to Reduce Involuntary Churn

Most advice on this topic treats it as purely a payments problem. It's not - it's also a data problem. But let's start with the payment levers, then get to the layer everyone misses.

Pre-Dunning Notifications

The cheapest win in this entire stack. Send an email 30 days before a customer's card expires, asking them to update their payment method. This single step reduces failed payments by 20-30%.

Keep the email short, personal, and focused on one action. Include a direct link to update payment details. Don't bury it in a newsletter. One CTA, one link, done.

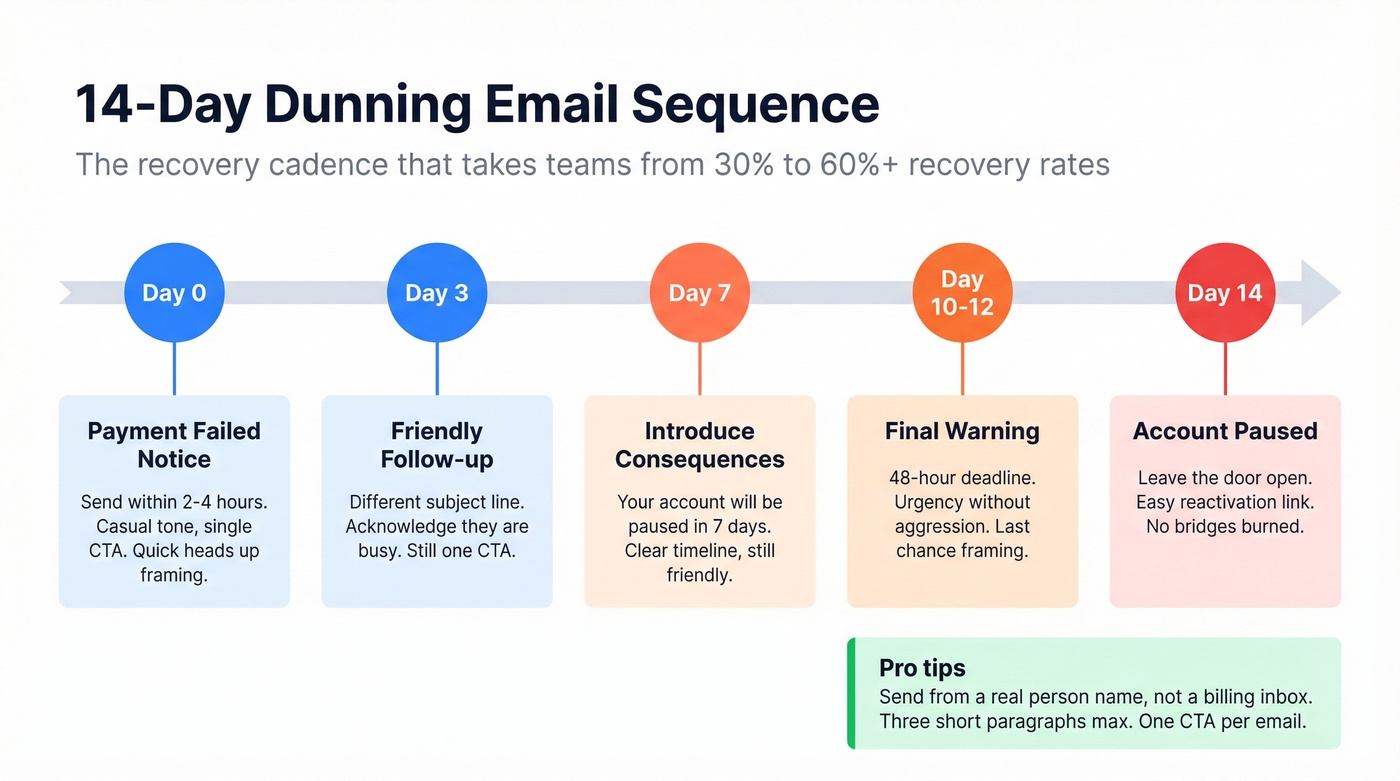

Dunning Email Sequence

Most teams either do nothing or send a single robotic "Your payment failed" email and hope for the best. That's not a strategy. Here's the cadence that works:

- Day 0 (within 2-4 hours of failure): Payment failed notification. Casual tone, single CTA to update payment. "Takes 30 seconds" framing.

- Day 3: Friendly follow-up. Different subject line. Acknowledge they're busy.

- Day 7: Introduce consequences with a timeline. "Your account will be paused in 7 days."

- Day 10-12: Final warning with a 48-hour deadline. Urgency without aggression.

- Day 14: Account paused notification. Leave the door open to reactivate.

Send from a real person's name, not a generic billing inbox. Use casual subject lines - "Quick heads up about your account" outperforms "Payment Failure Notification" every time. Three short paragraphs max, single CTA. Give customers a brief grace period after the final dunning email before hard-canceling; this catches the stragglers who update late.

Teams that rewrite their robotic dunning emails routinely improve recovery rates from ~30% to 60%+. The sequence stays the same. The words change. That's how much copy quality matters here. (If you want more subject line ideas, pull from these subject lines and adapt them to billing.)

Smart Retry Logic

The baseline retry schedule: retry at 1, 3, and 7 days after the initial failure. But static schedules leave money on the table.

ML-based smart retries analyze decline codes, time of day, day of week, and issuer patterns to pick the optimal retry moment. Solidgate's data shows 51-67% improvement in first-retry conversion and 23.6% faster revenue recovery. Here's the thing: soft declines - temporary failures like insufficient funds or processor timeouts - account for 70-90% of all failed card-not-present payments. These are retryable by definition. Most billing platforms offer smart retries as a toggle. Turn them on.

Don't overdo it, though. Excessive retries flag your Merchant ID with issuers, degrading your baseline authorization rate over time. Three to four retries over 7-14 days is the sweet spot. Beyond that, you're hurting yourself.

Account Updaters

Roughly 33% of cards are reissued every year. Account updaters automatically fetch updated card credentials from issuers before the old ones fail.

The mechanics are batch-based: you submit a file of cards to the network, and they return updated credentials. Target cards expiring within 30 days and high-value subscribers for regular batch updates. Visa, Mastercard, and Amex all offer updater services, and most modern billing platforms support them natively.

Network Tokenization

Network tokenization replaces stored card numbers with network-issued tokens that update automatically through the card's lifecycle. When a card is reissued, the token stays valid - no batch update needed.

Visa reports a ~6 percentage point improvement in transaction completion rates for tokenized payments, plus 40% lower fraud rates. Mastercard cites 3-6 percentage point approval rate lifts, and tokenized transactions can deliver a 42.5% improvement in customer LTV. Some card brands offer interchange reduction incentives for tokenized transactions in the US, Europe, and Australia.

Think of account updaters and network tokenization as complementary. Account updaters are batch - you proactively refresh credentials on a schedule. Network tokens are real-time - credentials update automatically through the token lifecycle. Run both.

Payment Method Diversification

Every payment method you don't accept is a customer you might lose. Accept Apple Pay, Google Pay, and PayPal alongside cards. Offer ACH in the US and SEPA in the EU for bank-to-bank payments that bypass card decline issues entirely. Prompt customers to add a backup payment method during onboarding, and make the payment update flow dead simple - one click from the dunning email to a pre-filled form.

Bank-to-bank methods have dramatically lower failure rates because there's no card expiration, no issuer fraud filter, and no "generic decline" black box to fight.

The Overlooked Layer: Contact Data Quality

Here's the contrarian take nobody in the payments world talks about: your dunning sequence is worthless if the emails bounce.

Industry estimates suggest 10-15% of email addresses go stale within 18 months. If that describes your customer database, your recovery emails are silently failing. The customer never learns their payment failed. They don't update their card. They churn. And your dashboard shows "dunning completed" as if everything worked fine.

Multi-channel recovery - SMS fallback, in-app notifications - has the same dependency. Bad phone number on file? Your SMS doesn't land either.

Run your customer list through a verification tool before launching dunning campaigns. Prospeo's real-time email verification catches bad addresses at 98% accuracy with a 7-day refresh cycle, so your dunning emails actually reach the customer instead of bouncing into the void. For stale CRM records, enrichment workflows can return updated contact data at a 92% match rate, filling in the gaps before your recovery sequence fires.

Implementation Priority Stack

You don't need to do everything at once. Here's the order, ranked by impact and ease:

- Segment your churn. Split voluntary vs. involuntary in your billing dashboard this week. If you skip this step, everything else is guesswork. (If you need a framework, start with a proper churn analysis.)

- Launch pre-dunning notifications. 30-day card expiry emails. Highest ROI, lowest effort.

- Build a proper dunning sequence. Day 0/3/7/10-12/14 cadence with human-sounding copy. (Treat it like sequence management, not a one-off email blast.)

- Enable account updaters + smart retries. Most billing platforms have these as toggleable features. Dedicated recovery tools like Churnkey and Butter often price on a revenue-share model, around 10-25% of recovered revenue.

- Add network tokenization. Requires more integration work but compounds over time.

- Audit contact data quality. Verify emails and phone numbers before every dunning campaign cycle. (If you're comparing vendors, see these data enrichment services.)

That Reddit founder who cut payment-failure churn by 60% in three months? They implemented steps 2-4 simultaneously. The stack works. The question is how fast you move.

Teams that segment involuntary churn always find the same hidden problem: stale CRM data. Expired emails, wrong contacts, outdated records. Prospeo enriches your CRM with 50+ verified data points per contact at a 92% match rate - so your recovery workflows reach real people.

Stop leaking revenue to contact data you haven't refreshed in months.

FAQ

What percentage of churn is involuntary?

Typically 20-40% of total subscription churn. Benchmarks show it at 0.86% monthly vs. 2.41% voluntary. The share varies by payment method - 51% of prepaid card churn is involuntary vs. 18% for credit cards.

What's a good involuntary churn rate?

B2B averages ~6%, B2C ~9%, and SaaS sits at ~8%. Credit card subscribers average ~6% while prepaid hits ~23%. Anything above your segment benchmark signals a recovery gap worth closing immediately.

How long should a dunning sequence last?

Fourteen days is the standard recovery window. Start with a pre-dunning email 30 days before card expiry, then escalate through Day 0, 3, 7, 10-12, and a final account-pause notification on Day 14. Most recoveries happen in the first 72 hours.

Can bad contact data cause subscription churn?

Yes. If the email on file is outdated, dunning emails bounce and the customer never learns their payment failed. SMS fallback fails the same way with bad phone numbers. Verifying your customer contact data before running dunning campaigns is one of the simplest ways to improve recovery rates.

What's the difference between voluntary and involuntary churn?

Voluntary churn happens when a customer actively cancels - they're unhappy, found an alternative, or no longer need the service. Involuntary churn happens when a payment fails and the subscription lapses without the customer's intent. Recovery strategies differ entirely: voluntary demands product improvements, while involuntary demands payment infrastructure like dunning, smart retries, and tokenization.