Lead Generation for Insurance: 10 Strategies for 2026

You just spent $500 on 50 leads. Twelve were wrong numbers. Eight swore they never filled out a form. Three already had coverage. And the two who picked up wanted to argue about their current premium, not buy a new policy.

Lead generation for insurance has always been a grind, but the math is broken for most agents. The insurance industry was already pouring $12.51B into digital advertising by 2022, and the top 10 carriers eat 82% of that spend. GEICO alone spends roughly $4 for every $100 in premium revenue on marketing. You're not matching that budget. But here's the thing: 74% of consumers research insurance online, and only 25% buy online. The rest want a human. They want you. The question is whether you're generating leads in a way that doesn't bleed your budget dry.

What You Need (Quick Version)

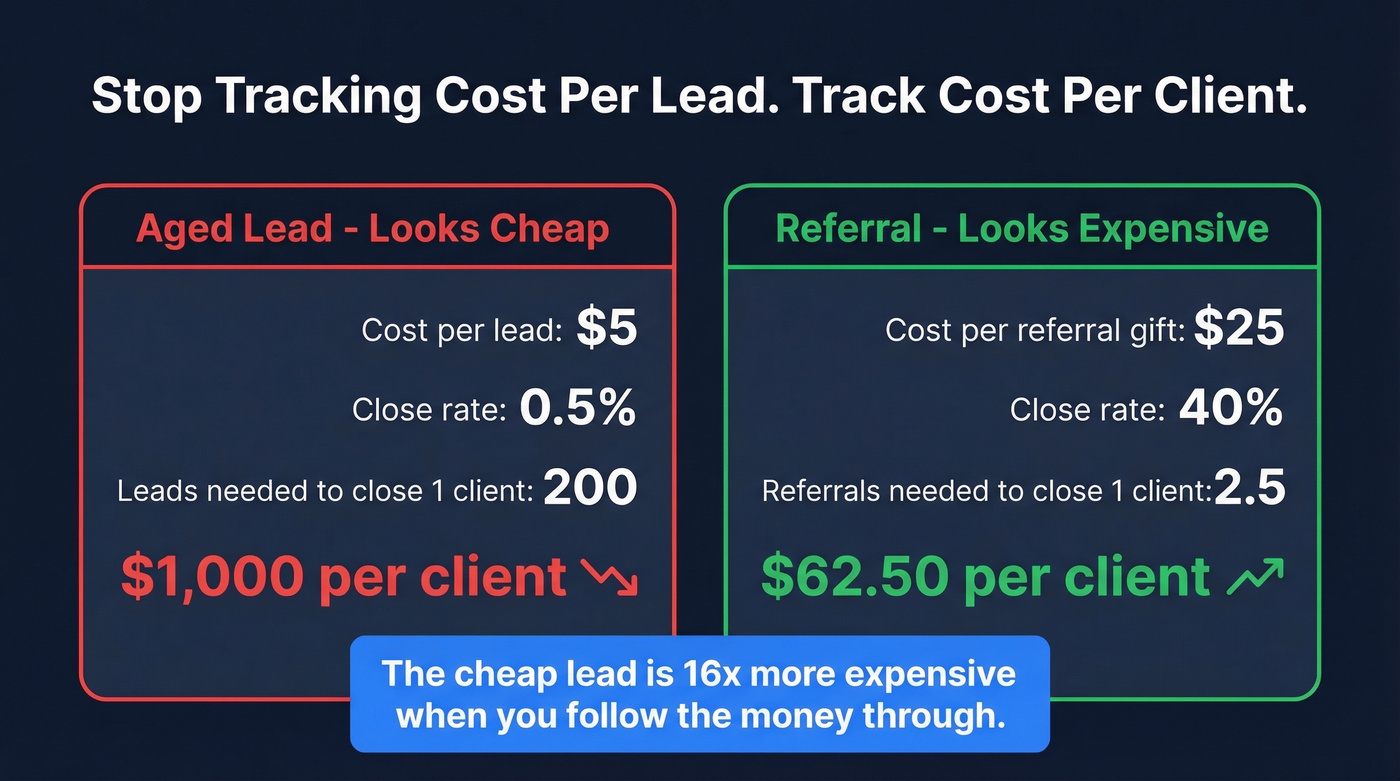

Stop obsessing over cost per lead. Start obsessing over cost per client.

The math: a $5 aged lead with a 0.5% close rate means you're spending $1,000 to acquire one client. A $25 referral gift card with a 40% close rate? That's $62.50 per client. The "cheap" lead is 16x more expensive when you follow the money all the way through.

$0/month: Build referral systems, optimize your Google Business Profile, publish locally-focused content. These are the highest-ROI channels and they cost nothing but time.

$1,000-$3,000/month: Layer in Google Ads targeting local long-tail keywords, plus email nurture sequences for leads that didn't convert the first time. This is where most independent agents should land.

$5,000+/month: Add Meta lead forms with aggressive follow-up automation, a lead vendor for volume, and contact management automation to keep nothing from slipping through the cracks.

How Much Do Insurance Leads Actually Cost?

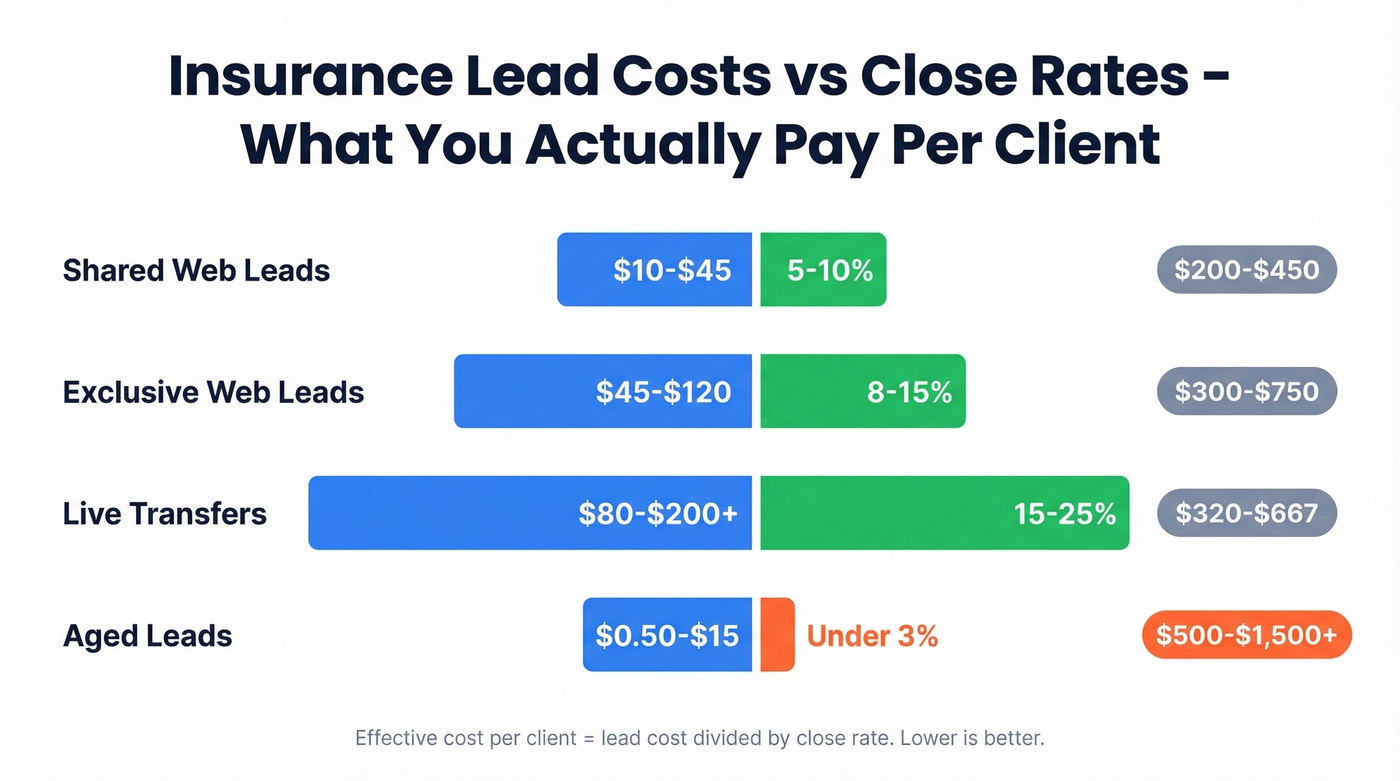

The range is enormous - from fifty cents to over $200 per lead - and the number that matters isn't what you pay per lead, it's what you pay per client who actually signs a policy.

General Lead Pricing

| Lead Type | Price Range | Typical Close Rate |

|---|---|---|

| Shared web leads | $10-$45 | 5-10% |

| Exclusive web leads | $45-$120 | 8-15% |

| Live transfers | $80-$200+ | 15-25% |

| Aged leads | $0.50-$15 | Under 1-3% |

Life Insurance Leads

| Lead Type | Price Range | Close Rate |

|---|---|---|

| Shared web | $20-$45 | 5-8% |

| Exclusive | $75-$150 | 8-12% |

| Live transfer | $80-$200+ | 15-25% |

| Aged | $5-$15 | Under 2% |

Exclusive leads cost roughly 2-3x what shared leads cost. That premium is worth it. When five agents are calling the same person within an hour, nobody wins.

Here's the real math on life insurance: purchased life leads close at 2-3%. If you're buying exclusive leads at $80 each and closing 2.5%, your actual acquisition cost per client is $3,200. At the low end - $65 leads, 3% close - you're at roughly $2,200 per client. The realistic range lands between $2,000 and $3,000 for most agents, and that's before you factor in your time making calls, running quotes, and following up for weeks.

This is why agents who build their own lead generation systems - referrals, SEO, content - consistently outperform those who rely on purchased leads. The upfront effort is higher, but the unit economics are dramatically better.

10 Strategies for Insurance Agencies

These are ordered from free/highest-ROI to paid/scalable. Start at the top and work down as your budget allows.

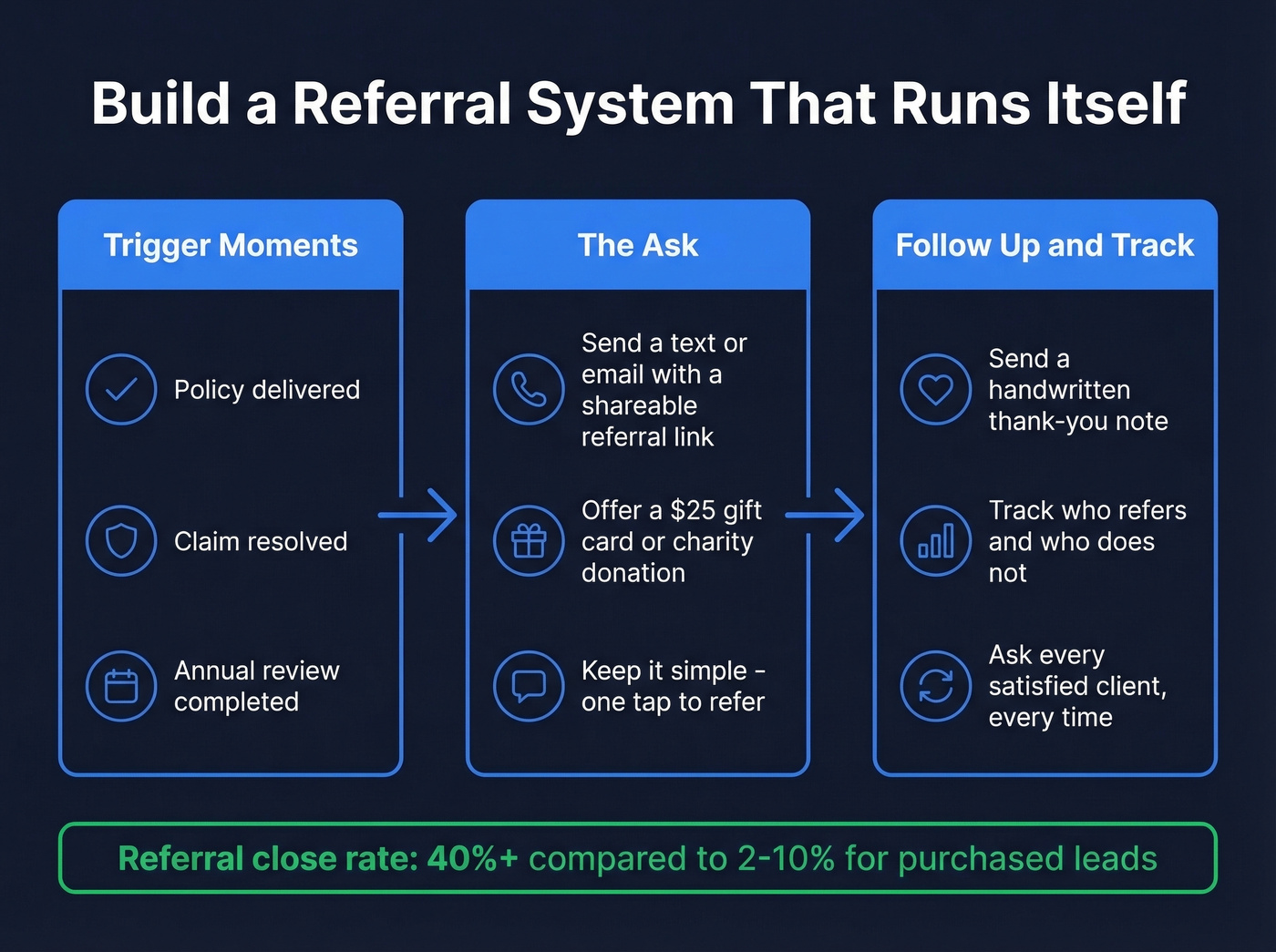

1. Referral Systems

Referrals aren't luck. They're a system.

The agents who get consistent referrals have a structured process: they ask at the right moment - after policy delivery, claim resolution, or an annual review. They make it easy with a simple text or email containing a shareable link. And they follow up with a thank-you that reinforces the behavior.

A warm referral closes at 40% or higher. Nothing else in insurance lead generation comes close. Build a referral incentive - a $25 gift card, a charitable donation in the client's name, a handwritten note - and create a cadence. Ask every satisfied client, every time. Track who refers and who doesn't. If you're wondering how to get clients without a massive ad budget, this is where you start.

2. Local SEO & Google Business Profile

National carriers can't outspend you on "best home insurance agent in [your city]." That's your territory.

The concept is geo authority - building local relevance through consistent NAP across every directory, local landing pages for each city and suburb you serve, and blog titles that mention specific neighborhoods, counties, and landmarks. Stack up Google reviews from real clients. Respond to every one.

Your E-E-A-T signals matter more in insurance than almost any other vertical. Add your license number to your author bio. List your designations, carriers, and years of experience. Share real claims stories (anonymized, of course). Google's AI Overviews favor structured, skimmable content with clear headings, Q&A sections, and schema markup - give them exactly that. Add a chat widget to your quote pages while you're at it. A simple "ask a question" option can capture leads that would otherwise bounce instead of finishing a full form.

3. Content Marketing & Blogging

Zero-click searches dominate. Most people will read your answer in Google's AI Overview and never visit your site. That's fine - visibility builds trust, and the people who do click through are high-intent.

Focus on long-tail keywords your competitors ignore. "Does homeowners insurance cover sump pump failure in [state]" will never get massive volume, but the person searching it is about to buy a policy. Structure content with clear H2/H3 headings and FAQ sections so Google can pull your answers into featured snippets. Webinars work well for commercial lines too - a 30-minute session on "Understanding Your Business Insurance Gaps" positions you as the expert and captures high-intent prospects with minimal ad spend.

4. Email Nurture Sequences

Your unconverted leads and existing book of business are sitting in your CRM doing nothing. Build nurture sequences for leads who quoted but didn't bind - a 7-touch sequence over 30 days with educational content, not just "ready to buy yet?" emails.

88% of insurance consumers demand a personalized experience, which means your sequences need to segment by line of business, not blast the same email to everyone. Cross-sell your existing clients with policy review campaigns: "You have auto with us - did you know bundling home saves an average of 15%?"

If you need a starting point, use proven sales follow-up templates and adapt them to each line.

5. Social Media

Don't try to be everywhere. Match the platform to the line of business. Commercial lines and group benefits? LinkedIn is where HR directors and CFOs spend their time. Personal lines - auto, home, renters? Facebook and Instagram, especially in local community groups.

One platform done consistently beats four platforms done poorly.

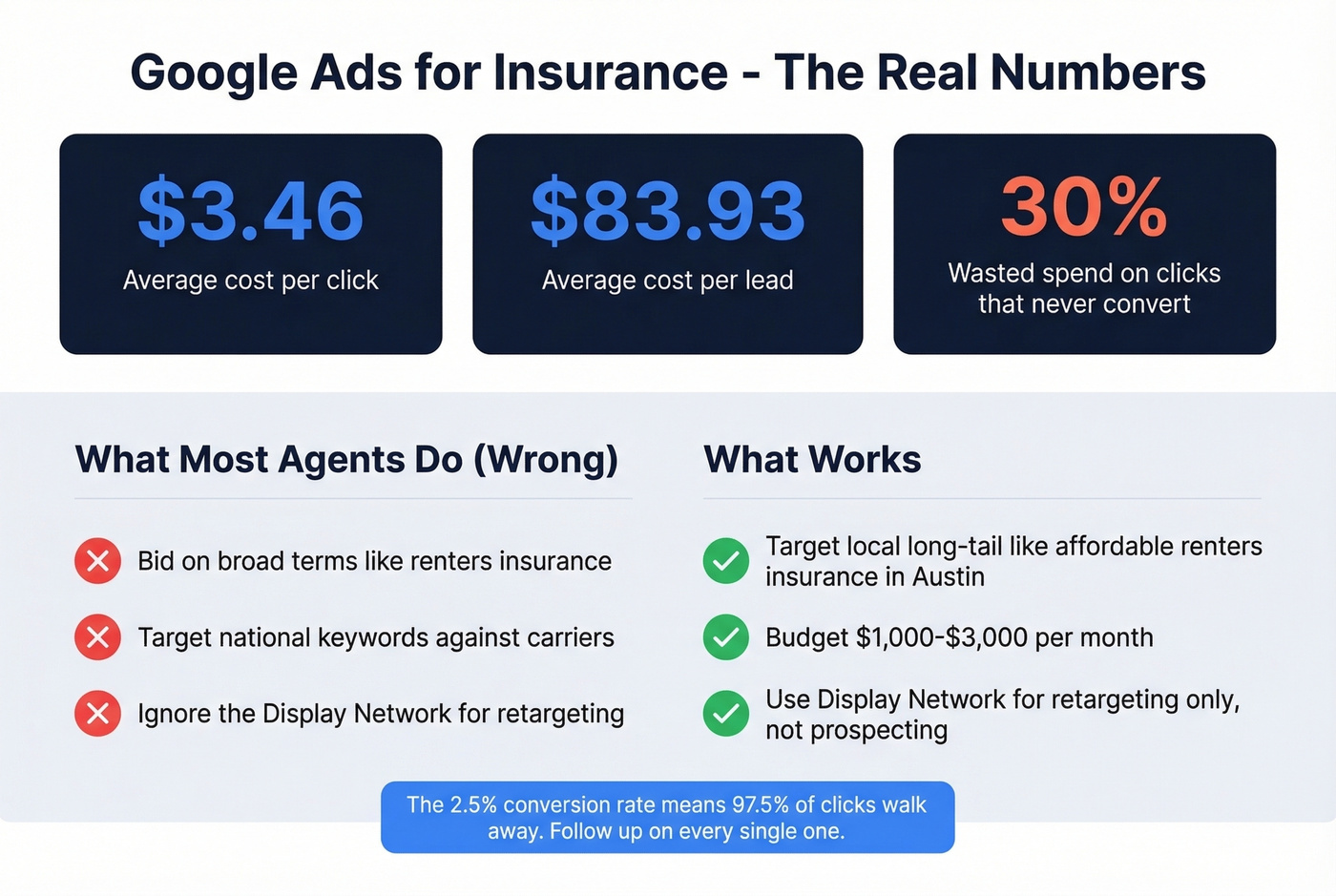

6. Google Ads / PPC

The Finance & Insurance benchmarks for Google Ads: $3.46 average CPC, $83.93 average cost per lead, 2.5% conversion rate. The waste rate sits at 30%, meaning nearly a third of your budget goes to clicks that never convert.

For independent agents, a $1,000-$3,000/month budget is the realistic range. Focus on local long-tail keywords - "affordable renters insurance in [city]" converts better than "renters insurance" and costs a fraction of the CPC. Use the Display Network for retargeting, not prospecting.

7. Facebook / Meta Ads

Meta ads can generate volume, but the lead quality demands aggressive follow-up. One final expense agent on Reddit described running high-intent lead form campaigns at $700/day on weekdays, $250/day on weekends - and was stuck at a 3% close rate after two months. They called it "not sustainable."

The agents who make Meta work pair it with automation tools like GoHighLevel for instant auto-texting and appointment pushes. If you're not following up within minutes - literally minutes - Meta leads go cold fast. Budget $500-$2,000/month to start, test video vs. static creatives, and track cost per client, not cost per lead.

8. Buying Leads from Vendors

Let's be honest: buying leads is useful when you're new and need reps - practice quoting, objection handling, closing. Long-term, it's a tax on agents who haven't built their own pipeline.

One agent on r/InsuranceAgent described working an aged lead sheet of 2,800 numbers that had been "ran into the dirt by every agent." Over 2,000 dials, five presentations, $1,000 in commission. Prospects were angry, claiming they never filled anything out. If you're buying leads, buy exclusive, verify the vendor's TCPA compliance, and treat it as a bridge - not a strategy.

9. Commercial Insurance Prospecting

For commercial lines, group benefits, or business insurance, the lead generation game is fundamentally different. You're not waiting for consumers to fill out a form. You're identifying businesses that fit your appetite and reaching the decision-maker directly - the HR director, the CFO, the business owner.

This is where a B2B data platform replaces the lead vendor entirely. Prospeo lets you search by industry, company headcount, job title, and location - plus 30+ other filters including buyer intent and technographics - to build targeted prospect lists of exactly the decision-makers you need. The free tier gives you 75 verified emails per month, enough to start filling a commercial pipeline without spending a dollar on leads. With 98% email accuracy and a 30% mobile pickup rate, you're reaching people on verified direct dials instead of guessing at email formats or calling main office lines.

For commercial prospecting, a verified contact list you build yourself is faster, cheaper, and more effective than buying names from a vendor who's selling them to five other agents. If you want more outbound ideas, borrow from modern sales prospecting techniques.

10. Upselling Your Existing Book

The cheapest lead you'll ever get is a client you already have.

Most agents ignore their existing book between renewal dates, and that's leaving money on the table - especially in a hard market where retention and wallet share matter more than ever. Run quarterly policy review campaigns. Identify clients with only one line and offer bundling. Flag clients approaching life events - new home purchases, business formation, growing families - and reach out proactively. Your CRM should be surfacing these opportunities automatically. If it isn't, that's a workflow problem worth fixing before you spend another dollar on new leads.

If you need to align the language internally, see the difference between cross-sell and upsell.

Insurance Lead Vendors Compared

If you're going to buy leads, at least compare your options.

| Vendor | Lead Type | Price Range | Exclusivity | Best For |

|---|---|---|---|---|

| EverQuote | Fresh shared | $15-$40+ | Shared | Multi-line agencies |

| QuoteWizard | Fresh shared | $10-$35+ | Shared | High-volume shops |

| Lead Heroes | Fresh + aged | $6-$30 | Both available | Budget-conscious new agents |

| NextGen Leads | Fresh exclusive | $15-$50+ | Exclusive | Agents wanting exclusivity |

| MediaAlpha | Fresh exclusive | $20-$75+ | Exclusive | Established agencies |

| Aged Lead Store | Aged (15-2,000+ days) | $0.15-$5.00 | Varies | Practice reps only |

Before you sign with any vendor, run through this checklist: Do they publish pricing transparently? How fresh are the leads - real-time, same-day, or aged? Can you filter by geography down to the zip code? What's their return policy for bad leads? Can they prove TCPA-compliant one-to-one consent for every contact? The consensus on r/InsuranceAgent is to walk away from any vendor who can't answer these questions clearly - and we'd agree.

You just read the math: $2,000-$3,000 per client from purchased leads. Prospeo gives you 300M+ professional profiles with 30+ filters - target business owners by industry, headcount, and location to build your own commercial lines pipeline. 98% email accuracy means your outreach actually lands.

Stop renting leads at $80 each. Own your pipeline for $0.01 per verified email.

The 5-Minute Rule

Speed kills in insurance lead generation - in a good way. Leads contacted within 5 minutes are 100x more likely to qualify than those contacted after 30 minutes. Within the first hour, they're 60x more likely to qualify compared to leads contacted after 24 hours.

The average response time across industries? 42 hours. 47% of businesses fail to respond within 24 hours at all. If you're responding in under five minutes, you're already beating almost everyone.

Set up auto-text responses in your CRM - GoHighLevel, HubSpot, or AgencyZoom can all trigger an immediate text the moment a lead comes in. Call within 60 seconds of the text. Then build a structured follow-up cadence for days 1 through 7: call, text, email, call, text, email, call. Most agents give up after two attempts. In our experience, the agents who follow up seven or more times close significantly more business than those who stop at three.

To tighten the process, map your lead generation workflow and remove handoff delays.

TCPA Compliance in 2026

The FCC's one-to-one consent rule, effective January 2025, changed the game for anyone buying insurance leads. The old model - where a consumer fills out one form and their information gets sold to a dozen agents - no longer provides legal cover for outbound calls.

Under the new rule, each seller or caller needs individual consent from the consumer. Blanket opt-ins don't protect you anymore. Penalties run $500-$1,500 per call.

The dangerous part: if your lead vendor can't prove individual consent for every contact they sell you, you're the one who's legally exposed. Not the vendor. You. Ask every vendor this question directly: "Can you provide proof of one-to-one consent for each lead?" If they hedge, deflect, or can't produce documentation, walk away. The cheapest lead in the world isn't worth a TCPA lawsuit.

If you're using SMS, review the risks around cold texting before you automate.

Mistakes That Burn Your Budget

Treating all leads the same. A live transfer and an aged lead require completely different follow-up cadences, scripts, and expectations. Segment by lead type and adjust accordingly.

Ignoring TCPA compliance. "My vendor handles that" isn't a legal defense. Verify consent documentation yourself.

Responding too slowly. Every minute past five drops your conversion probability. Automate the first touch.

Not disqualifying fast enough. If a lead doesn't match your appetite after two touches - wrong geography, wrong line, wrong coverage tier - stop calling and reallocate that time. Chasing unqualified prospects is the most expensive thing you can do with your day.

Optimizing to CPL instead of CPA. Cost per lead is a vanity metric. Cost per acquired client - factoring in close rate, follow-up time, and lifetime value - is the number that actually matters. (If you want the framework, start with cost to acquire customer.)

Ignoring seasonality. AEP, OEP, Q4 open enrollment - these windows drive massive demand spikes. Front-load your budget and content calendar around them instead of spending evenly across the year.

Failing to track attribution. If you can't tell which channel produced which client, you're flying blind. Tag every lead source in your CRM from day one. Lead management best practices start with knowing where your clients actually came from.

Tools for Insurance Lead Gen

You don't need a dozen tools. You need the right ones in four categories.

CRM & Automation: GoHighLevel is the insurance agent's Swiss Army knife - CRM, auto-texting, email sequences, and appointment scheduling in one platform. HubSpot works for a more traditional CRM with marketing automation. AgencyZoom is purpose-built for insurance workflows. (If you're evaluating options, here are real examples of a CRM.)

Data & Prospecting: For commercial lines, Prospeo covers the B2B prospecting gap - 300M+ professional profiles with verified emails and verified mobile numbers, searchable by industry, headcount, job title, and more. The 7-day data refresh cycle means you're not calling people who changed jobs two months ago.

Analytics: Google Analytics for channel attribution. Hotjar for heat maps on your quote pages - we've been surprised how often prospects abandon at the same form field.

Content: ChatGPT for first drafts of blog posts and email sequences. Canva for social graphics. Neither replaces expertise, but both save hours.

Your CRM is full of unconverted quotes and cross-sell opportunities sitting idle. Prospeo's enrichment engine returns 50+ data points per contact at a 92% match rate - fill in missing emails, direct dials, and firmographic data so your nurture sequences actually reach people.

Enrich your insurance book with verified contacts and never chase dead numbers again.

FAQ

How much should a new agent spend on leads?

Start with $0 strategies - referrals, local SEO, and content marketing cost nothing but time and consistently deliver the highest ROI. If you're buying leads, budget $500-$1,000/month for shared web leads and track cost per client, not cost per lead. Scale up only after you know your close rate.

Are aged insurance leads worth buying?

Rarely. At $0.50-$5 per lead they look cheap, but close rates often fall under 1% and prospects are angry from being contacted by multiple agents. Your effective cost per client usually ends up higher than exclusive leads. Skip aged leads unless you're brand new and need practice reps.

What's the best lead source for life insurance agents?

Referrals convert at 40%+ and cost almost nothing - they're the clear winner at any experience level. For paid channels, exclusive web leads at $75-$150 outperform shared leads despite the higher upfront cost. For commercial lines and group benefits, building targeted prospect lists with a B2B data tool beats buying shared leads every time.

How do I comply with TCPA when buying leads?

Ask your vendor to prove one-to-one consent for every contact they sell you. The FCC's January 2025 rule requires individual consent - blanket opt-ins no longer protect you. Penalties run $500-$1,500 per call, and the liability falls on the caller, not the vendor.

What close rate should I expect from purchased leads?

Shared web leads close at 5-10%, exclusive web leads at 8-15%, and live transfers at 15-25%. Life insurance purchased leads sit at 2-3%. These numbers vary based on follow-up speed, script quality, and lead freshness - agents who respond within five minutes consistently outperform these averages.