CLTV Explained: Customer Lifetime Value & Loan-to-Value

The probability of selling to an existing customer runs 60-70%. For a new prospect, it's 5-20%. That gap is the entire reason CLTV exists as a metric - it quantifies the long-term payoff of keeping customers around.

Here's the thing: "CLTV" means two completely different things depending on whether you're in a SaaS boardroom or a mortgage lender's office. Most articles only cover one. This one covers both.

What Does CLTV Stand For?

CLTV has two distinct meanings depending on your industry.

In marketing and SaaS, CLTV stands for Customer Lifetime Value - the total profit a customer generates across their entire relationship with your business. It tells you how much you can spend to acquire someone and still make money.

In real estate and mortgage lending, CLTV stands for Combined Loan-to-Value - the ratio of all outstanding loans against a property divided by that property's appraised value. It determines whether you qualify for a HELOC and at what rate.

If you're here for Customer Lifetime Value, the margin-adjusted SaaS formula is CLV = (ARPA x Gross Margin %) / Churn Rate. A healthy ratio of lifetime value to acquisition cost starts at 3:1, with the SaaS median sitting around 3.5x. Jump to How to Calculate CLTV for worked examples.

If you're here for Combined Loan-to-Value, most HELOC lenders cap it at 80-90%. Jump to Combined Loan-to-Value in Real Estate for the formula and a worked example.

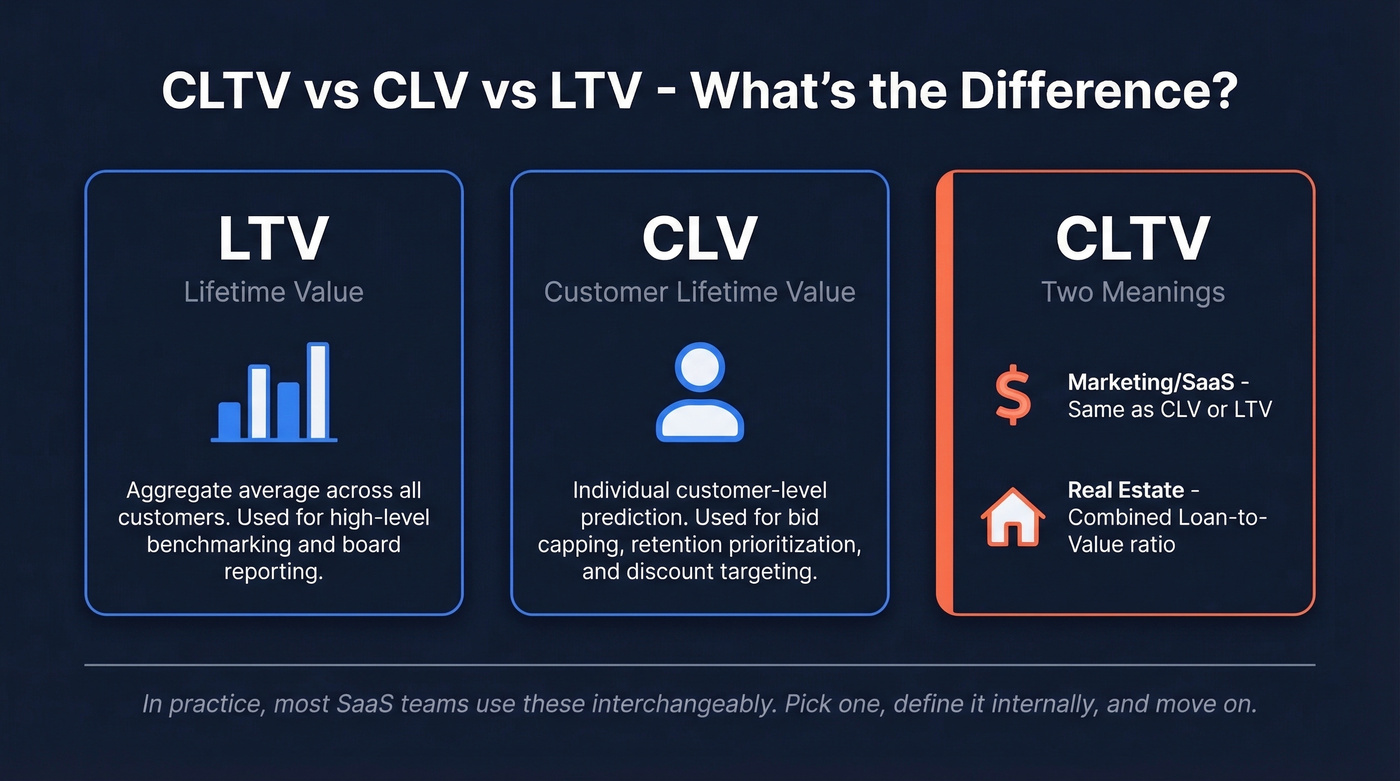

CLTV vs CLV vs LTV

These three acronyms cause more confusion than they should. The short version: they're interchangeable in most organizations. Peter Fader coined "CLV" to specify a particular calculation method, but in practice, marketing teams, finance teams, and SaaS operators use CLV, LTV, and CLTV to mean the same thing.

If you want to be precise, some teams draw a line between aggregate and individual measurement.

| Acronym | Common Usage |

|---|---|

| LTV | Aggregate average across all customers |

| CLV | Individual customer-level prediction |

| CLTV | Either - or Combined Loan-to-Value in real estate |

The individual-level distinction matters when you're doing bid capping, retention prioritization, or discount targeting - those require per-customer predictions, not averages. But don't lose sleep over the acronym. Pick one, define it in your internal docs, and move on.

Why Customer Lifetime Value Matters

CLV is the metric that connects retention to revenue. Without it, you're making acquisition and retention decisions in the dark.

A 5% increase in retention can drive 25-95% higher profits, per Bain & Company research. That's not a rounding error. It's a fundamental shift in unit economics that explains why the best SaaS companies obsess over net revenue retention before they obsess over new logo acquisition.

CLV gives you a single number to anchor budget decisions. How much can you spend to acquire a customer? Which segments deserve white-glove onboarding? Where should you invest in reducing churn? Every one of those questions starts with knowing what a customer is actually worth over time - not just their first invoice.

If you want to pressure-test the churn side of the equation, start with a simple churn analysis before you overcomplicate the model.

How to Calculate CLTV

The formula depends on your business model. Here are the two most common versions, followed by why you should always adjust for margin.

Ecommerce Formula

CLV = AOV x Purchase Frequency x Customer Lifespan

Worked example: your average order value is $65, customers buy 3.5 times per year, and the average customer sticks around for 4 years.

$65 x 3.5 x 4 = $910 revenue CLV

That's the top-line number. Not what you actually keep.

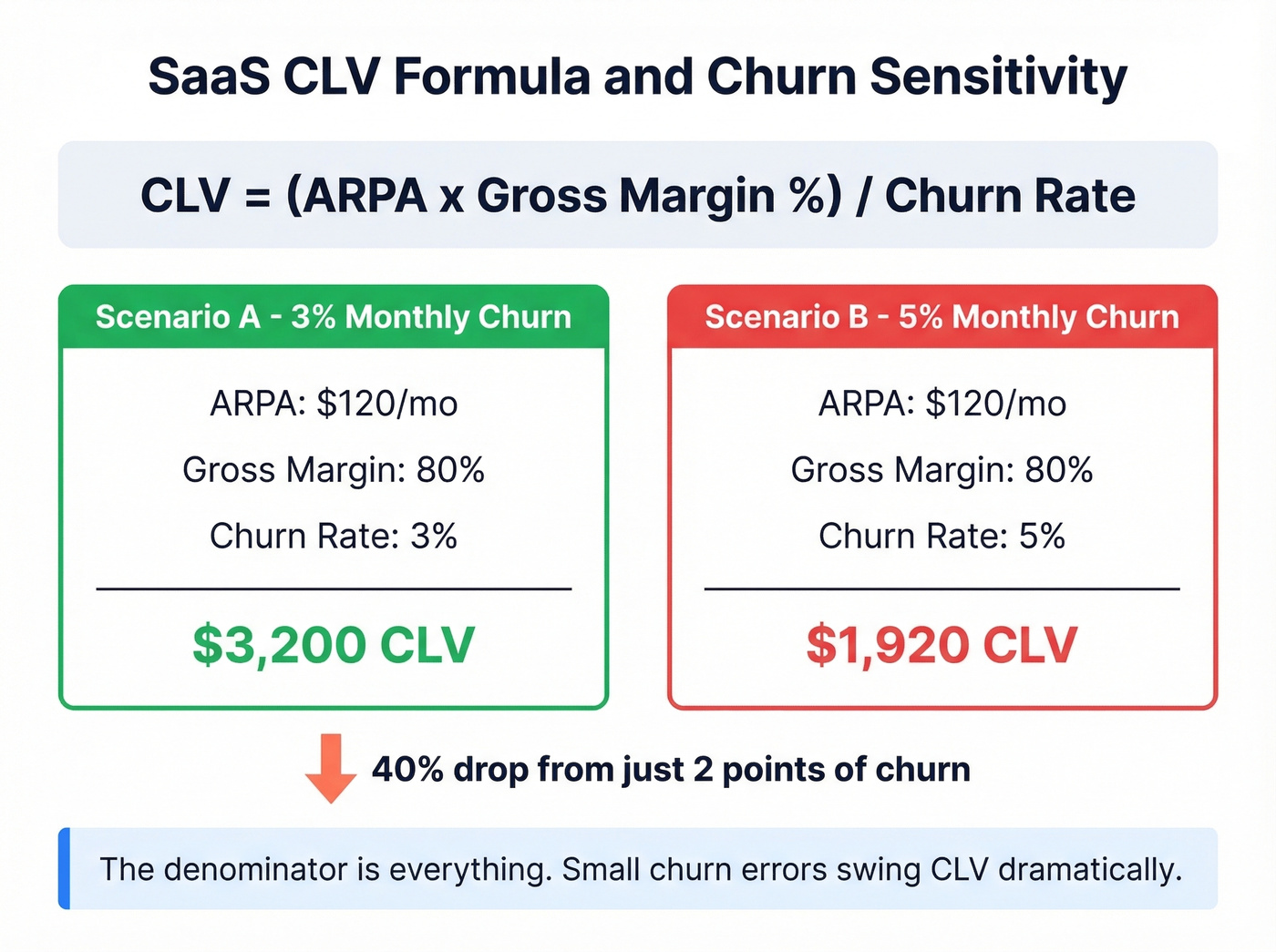

Subscription / SaaS Formula

CLV = (ARPA x Gross Margin %) / Churn Rate

Worked example: $120/month ARPA, 80% gross margin, 3% monthly churn.

($120 x 0.80) / 0.03 = $3,200 CLV

Change that churn to 5% and CLV drops to $1,920 - a 40% swing from a 2-point churn difference. We've seen this exact scenario play out with early-stage teams who underestimate how sensitive the denominator is.

The SaaS CFO recommends using cohort ACV rather than a blended average, and GRR-based dollar churn rather than logo churn. Small churn errors swing CLV dramatically, especially at companies where the denominator is tiny.

If you’re trying to connect CLV to acquisition spend, it helps to model cost to acquire customer alongside churn.

Revenue CLV vs Profit CLV

Revenue-based CLV is a vanity metric.

Take that $910 ecommerce example. At a 40% gross margin, your profit CLV is $364. That's a 60% gap between the number that looks good in a deck and the number that actually matters for budgeting.

In fintech, the gap is even wider because you need to subtract cost-to-serve, credit and fraud losses, funding costs, and partner revenue splits. Every CLV number shown to a board should be margin-adjusted. If your model doesn't account for gross margin at minimum, you're making acquisition decisions based on fiction.

Revenue CLV vs profit CLV matters - and so does acquisition cost. Prospeo cuts your cost-per-lead to $0.01 with 98% email accuracy, directly improving your LTV:CAC ratio without touching your product.

Fix the CAC side of your ratio before you overhaul retention.

Three CLV Calculation Methods

The right method depends on how much data you have and how volatile your customer behavior is.

Historical CLV

Sum up all the gross profit a customer has generated to date. It's backward-looking and assumes the future mirrors the past. Useful for quick segmentation, but the bigger risk is that historical CLV hides cohort shifts - which leads to budget misallocation when newer cohorts behave differently than older ones.

Cohort-Based CLV

Group customers by acquisition month, channel, or plan tier, then track revenue and retention curves per cohort. This reveals drop-off points and lets you compare customer quality across campaigns or time periods. In our experience, cohort-based CLV is the sweet spot for most teams with 12+ months of data. It's more accurate than historical and doesn't require a data science team to build.

Predictive CLV

For non-contractual businesses like ecommerce and marketplaces, the BG/NBD model uses purchase frequency, recency, and customer age to predict future transactions. For subscription businesses, survival analysis models churn timing. The discounted formula:

Predictive CLV = Sum of (Monetary Value x Retention Probability^t) / (1 + Discount Rate)^t

Practitioners on r/SaaS regularly debate whether the simple ARPA/churn formula is mathematically sound - and they're right to question it when churn is volatile or when you've got a mix of monthly and annual contracts. Predictive CLV requires clean transaction data and someone who knows how to validate these models. If you're at that stage, invest in the modeling. If you're not, the cohort approach will serve you well.

If you’re building a more advanced model, it’s worth aligning it with your funnel metrics so CLV ties back to pipeline reality.

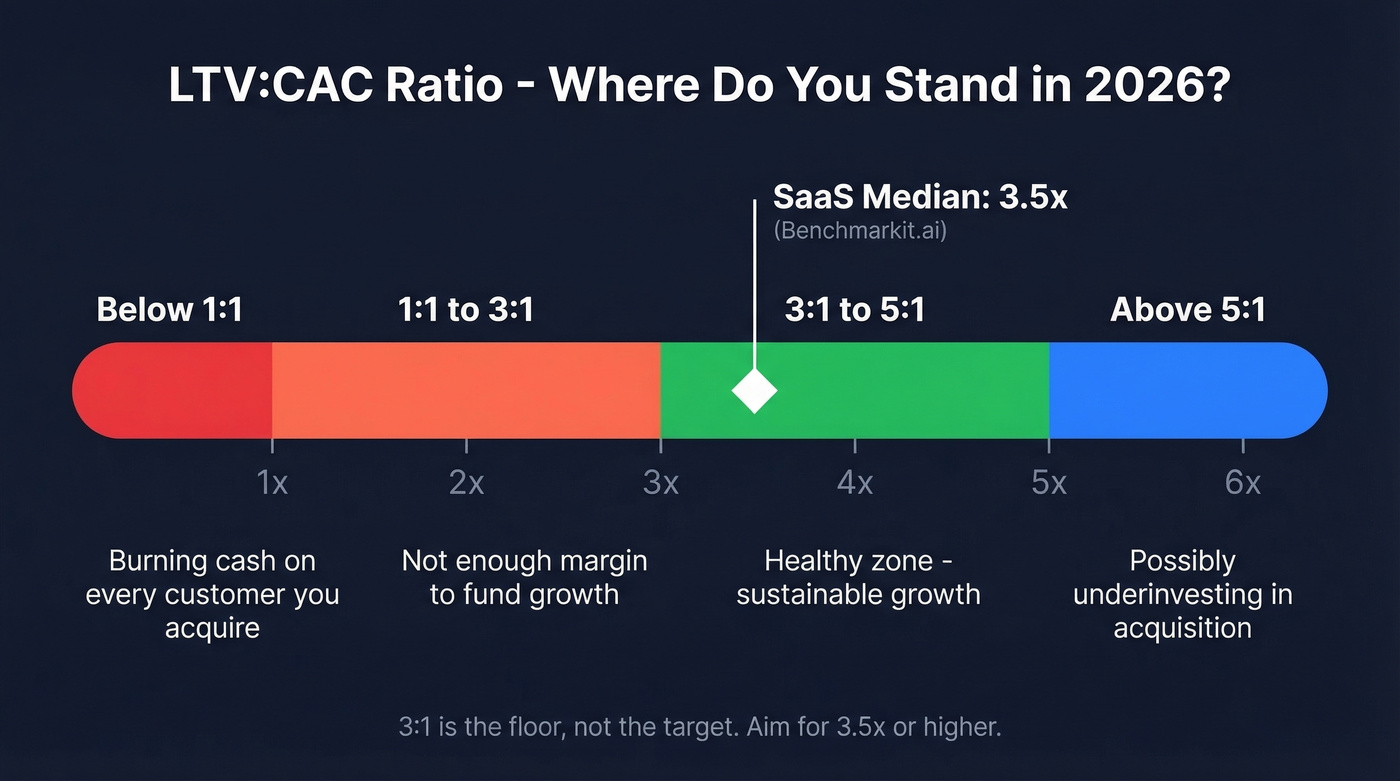

Ratio Benchmarks for 2026

The 3:1 ratio gets thrown around as the gold standard, but it's actually the floor, not the target. Benchmarkit.ai data suggests the SaaS median is closer to 3.5x.

Below 1:1 means you're burning cash on every customer you acquire. Between 1:1 and 3:1, you're likely not generating enough margin to fund growth. Above 5:1 sounds great, but it often signals you're underinvesting in acquisition - leaving revenue on the table because you're not spending enough to capture demand.

If you want to sanity-check whether your acquisition engine is healthy, compare against sales conversion rate benchmarks too.

Average CLTV by Industry

These benchmarks from CustomerGauge give you a sense of scale across B2B sectors:

| Industry | Average CLTV |

|---|---|

| Architecture firms | $1.13M |

| Business consultancies | $385K |

| Healthcare consultancies | $330K |

| Insurance companies | $321K |

| Software companies | $240K |

| B2B financial advice | $164K |

| Digital design brands | $90K |

If you're a software company and your CLV is $8K, you're either in a very different segment or you've got a retention problem worth investigating.

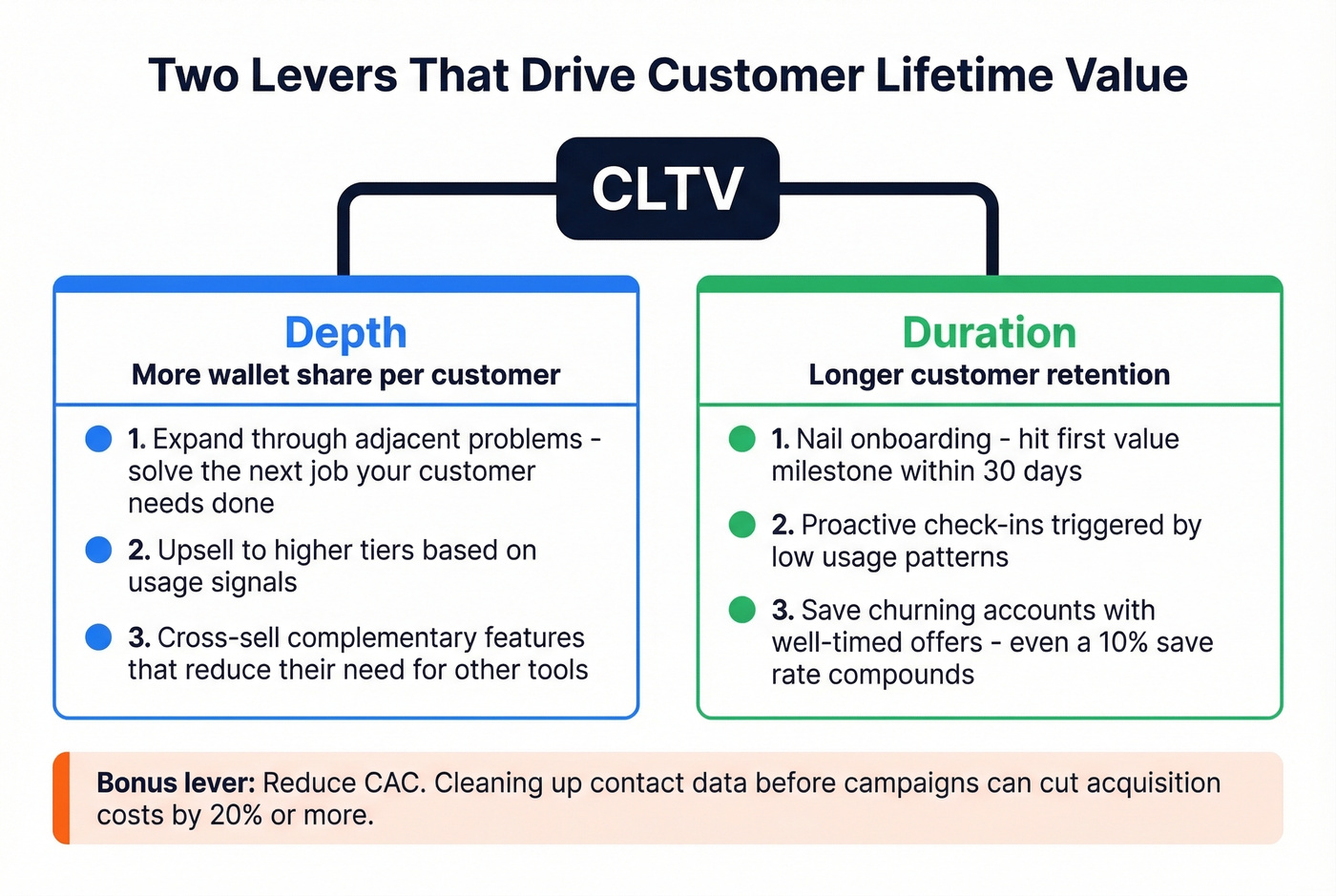

How to Improve CLTV

Two primary levers drive customer lifetime value: depth (more wallet share per customer) and duration (longer retention). Everything else is a tactic that feeds one of those two.

Let's be honest: if you're pre-product-market-fit with fewer than 100 customers, don't build a predictive CLV model. Track cohort retention curves, revisit quarterly, and focus your energy on the tactics below.

Nail Onboarding First

Most churn happens early. If a customer doesn't hit their first value milestone within the first month, the probability of renewal drops off a cliff. Invest in guided onboarding, proactive check-ins, and usage-based triggers that flag at-risk accounts before they ghost. One B2B team we spoke with cut Day-30 churn by 22% just by adding a single automated check-in email triggered by low product usage in week two.

If you’re operationalizing retention, track renewal rate alongside churn so you can separate expansion from saves.

Expand Through Adjacent Problems

The best expansion revenue comes from solving problems adjacent to the one that brought customers in. Map your product to the "money jobs" your customers are trying to do, and you'll find natural upsell and cross-sell paths that don't feel like a shakedown.

For a clean framework on expansion motions, see cross-selling and upselling.

Save Churning Accounts

A well-timed discount or plan adjustment can rescue accounts that would otherwise cancel. Even a 10% save rate on churning customers compounds meaningfully over time. Churn counteroffers aren't desperate - they're math.

Reduce CAC Through Better Data Quality

This one's underrated. If 15% of your outbound emails bounce, that acquisition spend is wasted - inflating your CAC without generating pipeline.

The lifetime-value-to-acquisition-cost ratio isn't just about increasing the numerator; a bloated denominator distorts the whole picture. We've seen teams cut CAC by 20%+ just by cleaning up their contact data before running campaigns. Prospeo's 98% email accuracy and 7-day data refresh cycle cut that waste at the source, at roughly $0.01 per email, with a free tier of 75 emails plus 100 Chrome extension credits per month. Verified contact data means higher reply rates, lower cost per opportunity, and a CAC number that actually reflects your go-to-market efficiency.

If you’re fixing bounce-driven waste, start with email bounce rate benchmarks and remediation.

Skip the CLV precision obsession. A directionally correct number you actually use beats a perfect model sitting in a Jupyter notebook nobody opens. Get the formula running, review it quarterly, and use it to make real decisions about where to spend.

A 3.5x LTV:CAC ratio means nothing if bad data inflates your acquisition costs. Teams using Prospeo book 26% more meetings than ZoomInfo users - driving down effective CAC and pushing that ratio above 5:1.

Stop leaking margin on bounced emails and wrong numbers.

Combined Loan-to-Value in Real Estate

CLTV means something entirely different in mortgage lending. If you're here from a real estate search, this section's for you.

What CLTV Means in Mortgages

CLTV = (All Loan Balances) / (Property Value)

Unlike LTV, which only considers a single mortgage, CLTV includes every lien against the property - first mortgage, second mortgage, HELOC draws, and any other subordinate financing. Lenders care about this ratio because in a foreclosure, second-lien holders only get paid after the first mortgage is satisfied. Higher combined loan-to-value means less equity cushion and more risk for subordinate lenders, which is exactly why they impose strict caps.

There's also HCLTV, which uses the full HELOC credit limit rather than just the drawn balance. Fannie Mae's guidelines specify that CLTV uses the drawn portion of a HELOC, not the full credit limit.

Typical Lender Caps

Most HELOC lenders set maximum thresholds around 80%, 85%, or 90%. An 80% cap is the most common for conventional HELOCs. Lenders offering 85% or 90% typically charge higher rates or require stronger credit profiles.

Some borrowers use a second mortgage strategically - keeping the first mortgage at 80% LTV to avoid PMI while accepting a higher combined ratio. It's a legitimate tactic, but you need to understand where your combined ratio lands before applying. Small changes in appraised value can push you over a cutoff, and if your home appraises $20K lower than expected, your ratio jumps and you lose access to better terms or get denied entirely.

Worked Example

You own a $400,000 home with a $240,000 mortgage (60% LTV). You apply for a $40,000 HELOC.

Total loans: $240,000 + $40,000 = $280,000

CLTV: $280,000 / $400,000 = 70%

That's well within most lender caps. But watch what happens if your home value drops to $350,000:

CLTV: $280,000 / $350,000 = 80%

You've just hit the cutoff where many lenders start tightening terms or reducing your available line. A modest market correction can change your borrowing position overnight - this is why sensitivity to property values matters far more than most borrowers realize.

FAQ

What is a good CLTV:CAC ratio?

3:1 is the minimum for sustainable growth, not a target. The SaaS median is 3.5x. Below 1:1 means you're losing money on every customer acquired. Above 5:1 often means you're underinvesting in acquisition and leaving growth on the table.

How do you calculate CLTV in Excel?

For subscription businesses: =(ARPA * Gross_Margin) / Churn_Rate. For ecommerce: =AOV * Purchase_Frequency * Customer_Lifespan. Always multiply by gross margin percentage to get profit CLV - the number that actually matters for budgeting decisions.

What's the difference between LTV and CLTV?

In marketing, they're interchangeable - most teams use them to mean customer lifetime value. In real estate, CLTV specifically means combined loan-to-value, which includes all liens against a property, not just the primary mortgage. Context determines the definition.

What CLTV do lenders require for a HELOC?

Most lenders cap combined loan-to-value at 80-90% for HELOC approval. An 80% cap is standard for conventional products. Lenders allowing 85-90% typically charge higher rates or require credit scores above 740. Small appraisal shortfalls can push borrowers over cutoffs unexpectedly.

How can bad data affect your CLTV:CAC ratio?

If 15% of outbound emails bounce, that acquisition spend is wasted - inflating CAC without generating pipeline. Verified email tools that deliver 98% accuracy at roughly $0.01 per lead directly improve the ratio by lowering your true cost per acquired customer.