How to Build a Go to Market Pitch Deck Slide That Gets Funded

Investors spend 2 minutes and 41 seconds on an average pitch deck. That's roughly 15-20 seconds per slide. Your go to market pitch deck slide either earns a follow-up meeting in that window or it doesn't.

Most founders know their GTM channels. They just can't show a repeatable, fundable motion on a single slide. One r/startups founder captured the problem perfectly - $70K in revenue, three LOIs, a product 85% built, and still stuck trying to visualize a GTM strategy that wasn't just a list of channels. That gap between "knowing your plan" and "proving it on a slide" is where most decks die.

Why Most GTM Slides Fail

Waveup reviewed 300+ pitch decks from pre-seed to Series C. The GTM slide was mishandled or skipped entirely in roughly half. A recurring theme on r/Entrepreneur from practitioners who've reviewed 20+ decks: polished gradients and icons can't save a slide with no strategy underneath.

The same mistakes show up constantly:

Channel list, not strategy. "Social media, trade shows, content marketing, partnerships" isn't a GTM plan. It's a brainstorm. Investors immediately question whether you've thought past the tactics.

No CAC math. Saying "we'll run paid ads" without expected acquisition cost, conversion rate, or optimization target is a red flag every time.

PR masquerading as GTM. Press coverage isn't a repeatable revenue channel. It's a spike, not a slope.

Fake partnerships. Unless you've signed a deal or can explain the rev-share structure, "strategic partnerships" reads as wishful thinking.

No funnel. Discovery, evaluation, purchase, retention - if your slide doesn't show this progression with conversion assumptions at each stage, you're asking investors to take your word for it. They won't.

What Investors Actually Want

Stop copying Airbnb's deck. Their GTM context - 2008, marketplace, pre-mobile - has almost nothing in common with your B2B SaaS motion. Raw user counts mean nothing without growth rate and ARPU. Investors want math based on your customer segments, not Statista numbers.

Here's what belongs on the slide:

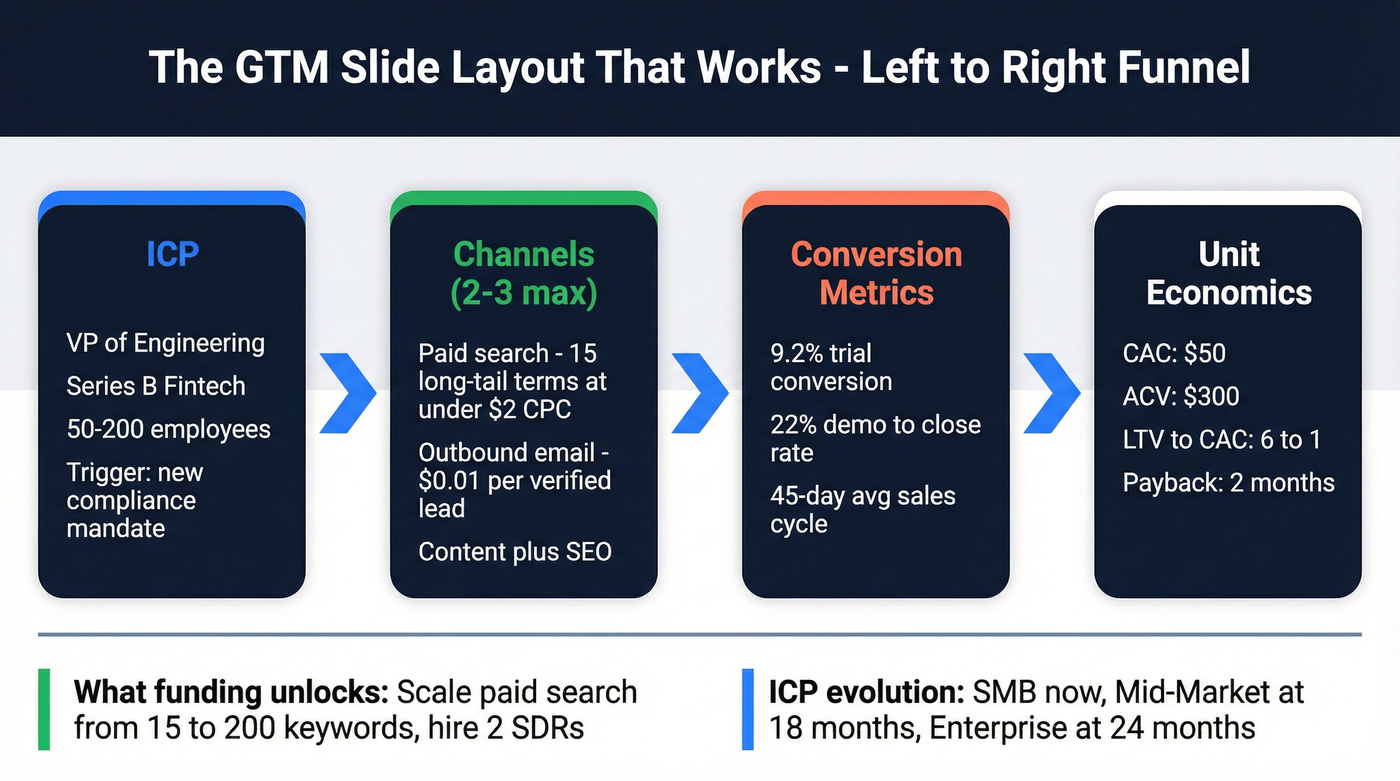

- ICP with specifics, not demographics. "VP of Engineering at Series B fintech companies with 50-200 employees" beats "tech decision-makers." (If you need a starting point, use an Ideal Customer Profile template.)

- 2-3 focused channels with evidence. Not a wish list. Evidence means you've tested it, have early data, or can point to comparable benchmarks.

- Funnel logic with conversion assumptions. Show the math from top-of-funnel to closed deal. (A simple sales funnel view helps investors follow the logic fast.)

- Unit economics. CAC and LTV with benchmark context. As OpenVC puts it, "a GTM slide with no numbers is unacceptable."

Pair a leading indicator - like pipeline at proposal stage - with the result it drove. Two metrics tell a better story than ten. Your ICP evolution timeline matters too: where you're focused now, at 6 months, at 18 months, and what funding specifically unlocks.

Counterintuitively, showing one known weakness with a credible plan to fix it builds more investor trust than a slide with zero gaps. Investors know your plan isn't perfect. Proving you know where the risks are signals maturity.

GTM Expectations by Stage

What counts as a credible go to market strategy slide changes dramatically depending on your stage. A framework from the analysis of 85 winning decks totaling $375M raised calls this "Pitch-Investor Fit" - you're selling different things to investors as you scale.

| Pre-Seed | Seed | Series A | |

|---|---|---|---|

| Typical raise | $250K-$1M | $1M-$3M+ | $5M+ |

| Traction that counts | LOIs, waitlists, pilots | MRR, retention | Repeatable engine |

| GTM slide focus | Vision + early signals | Channel validation + CAC | Scalable channels + LTV:CAC |

At pre-seed, three LOIs and a logical channel hypothesis is enough. By seed, you need MRR and at least one validated acquisition channel. Series A investors expect a repeatable growth engine with defensible acquisition math.

One critical warning from TechCrunch: if your ACV sits below $4,000, layering on a sales-led motion can sink your cost structure before you've proven anything. (If you're building sales-led, it helps to understand B2B sales benchmarks by motion.)

Your GTM slide's CAC math is only as good as your data. Founders inflate outbound costs with tools that bounce 20-35% of emails. Prospeo delivers 98% email accuracy at $0.01 per lead - giving you a real, defensible acquisition cost to put on that slide.

Stop guessing your CAC. Start proving it with data that actually connects.

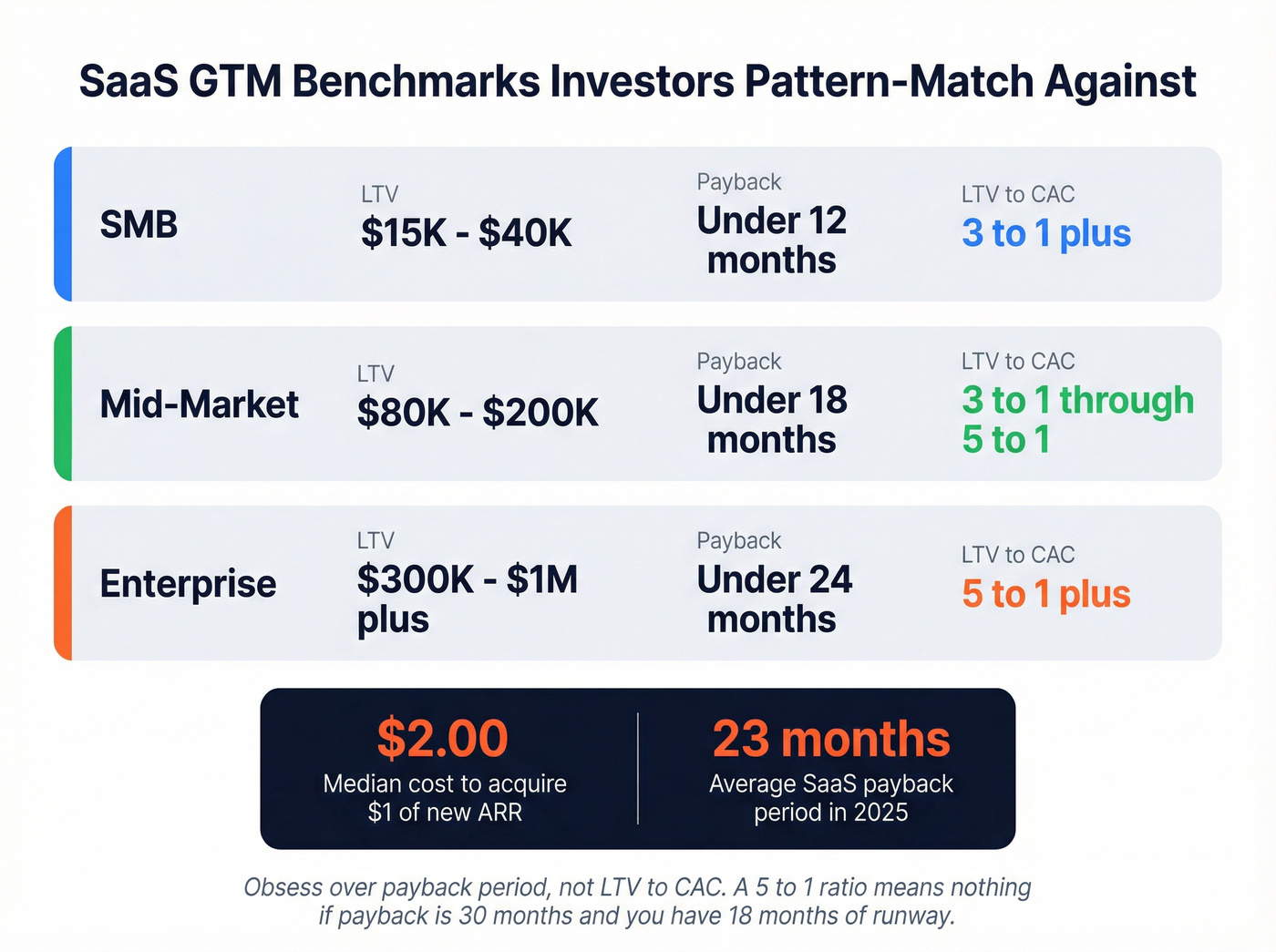

Benchmarks for Your GTM Slide

Investors pattern-match against benchmarks whether you include them or not. Better to frame your numbers proactively.

| Segment | LTV Range | Target Payback | LTV:CAC Target |

|---|---|---|---|

| SMB | $15K-$40K | <12 months | 3:1+ |

| Mid-Market | $80K-$200K | <18 months | 3:1-5:1 |

| Enterprise | $300K-$1M+ | <24 months | 5:1+ |

The trend isn't in your favor. Digital ad costs are up 5.13%, the median SaaS company now spends $2.00 to acquire $1 of new ARR, and average payback has stretched to 23 months. B2B SaaS CAC averages ~$1,200 per customer. If your slide shows a 3:1 LTV:CAC with a sub-12-month payback, you're in strong territory. At 2:1 or below, you need a clear story about how funding improves that ratio. (If you want to sanity-check your inputs, start with a clean CAC definition and formula.)

Here's the thing: most early-stage founders obsess over LTV:CAC ratios when they should obsess over payback period. A 5:1 ratio means nothing if your payback is 30 months and you have 18 months of runway. Payback period is the metric that determines whether you survive long enough to realize your LTV.

GTM Slide by Business Model

Enterprise B2B: Name your target accounts. Map the land-and-expand motion - pilot to department to enterprise license - with metrics at each stage. (This is easier to justify when you anchor it in an enterprise B2B sales motion.)

Product-Led Growth: Focus on install/activation costs by channel, retention curves by cohort, and viral coefficient. Investors want the self-serve engine, not a sales team bolted on. (Make sure you can explain your funnel metrics clearly.)

Phased approach: This is the most common for early-stage. Founder sales, then inside sales, then channel partners, with CAC, LTV, and payback tracked per phase. Two worked examples that show the specificity investors want: 15 long-tail paid search terms at <$2 CPC, 9.2% trial conversion, scaling to $50 CAC on $300 ACV. Or Meta ads at $17 CAC with $60 LTV. Sequencing matters too - start with end-customers to create leverage when approaching channel partners or enterprise buyers.

Structure your slide as a left-to-right funnel: ICP on the left, channels in the middle, conversion metrics flowing right, with CAC/LTV anchored at the bottom. One slide. Clean layout. Numbers that breathe.

Validate Before You Present

Your actual CAC is probably 2-3x what you're presenting. We've seen it over and over - founders undercount by ignoring sales time, tool costs, and data quality overhead. I watched a founder lose a follow-up meeting because his "outbound" CAC didn't include the $400/month he was spending on three different data tools, none of which gave him accurate emails.

Before you put numbers on a slide, validate your channels. Run customer interviews to confirm where your ICP discovers solutions. Reverse-engineer competitor acquisition using Semrush, SimilarWeb, or SparkToro. Run small-budget tests - $500-$1,000 per channel - to get real conversion data instead of projections.

If outbound is one of your GTM channels, your contact data quality directly determines whether your CAC numbers survive diligence. Email bounce rates above 5% destroy channel economics and tank domain reputation. (If you’re troubleshooting, start with email bounce rate benchmarks and fixes.) Prospeo finds verified emails across 300M+ professional profiles at 98% accuracy for roughly $0.01 per lead, with data refreshed every 7 days. That's the kind of cost structure that holds up when an investor asks "what's your actual cost per qualified meeting?"

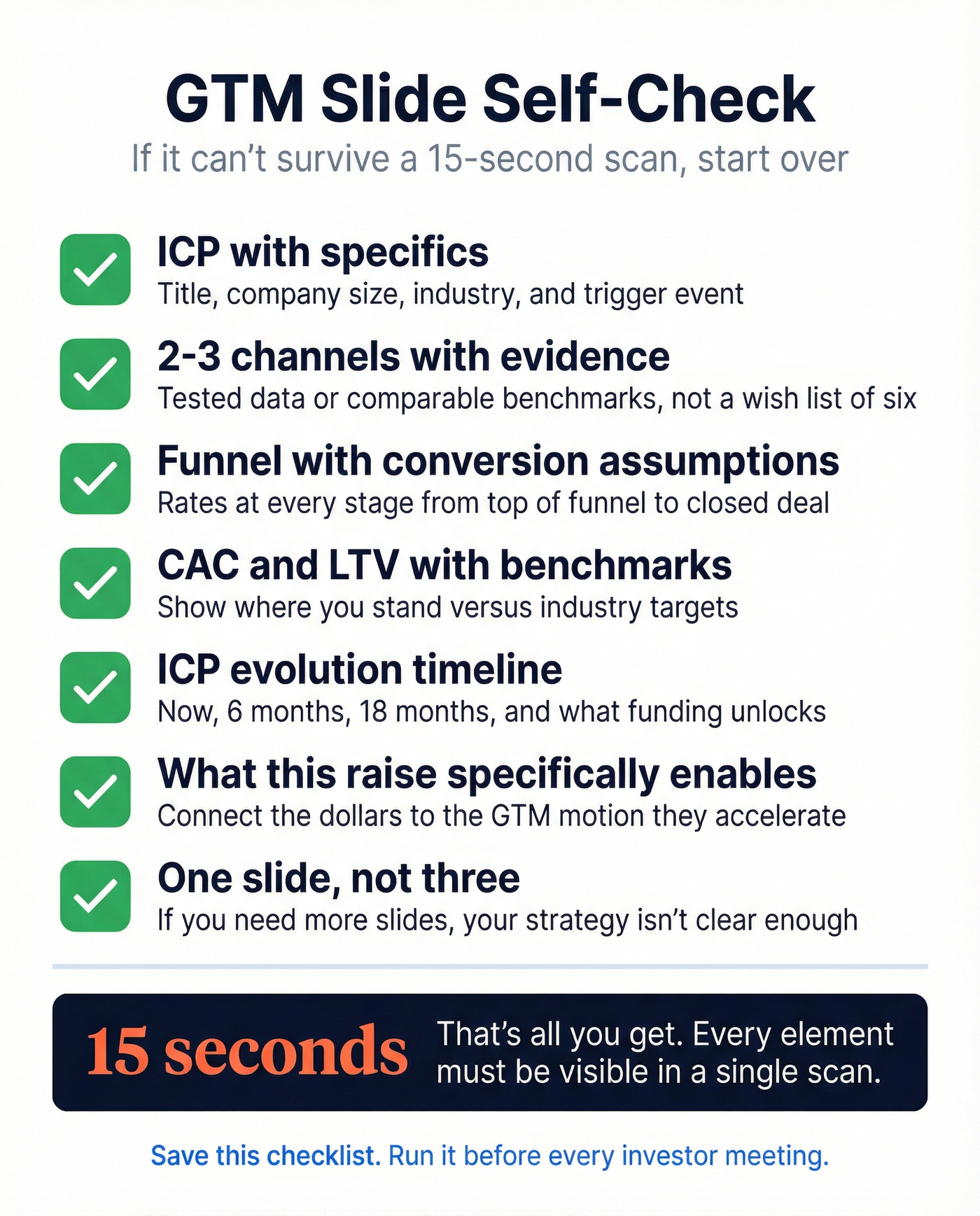

GTM Slide Self-Check

Before you present, run through this:

- ICP defined with specifics - title, company size, industry, trigger - not demographics

- 2-3 channels backed by evidence, not a wish list of six

- Funnel with conversion assumptions at each stage

- CAC and LTV with benchmark context showing where you stand

- ICP evolution over 6, 18, and 24 months

- What this funding specifically unlocks

- One slide. Not three.

If your slide can't survive a 15-second scan with all seven visible, cut everything else and start over.

For the actual slide design, Beautiful.ai auto-formats layouts (typically around $10-$20/user/month), Canva works for quick templates, and Pitch offers collaborative editing. The tool matters less than the content, but a clean layout helps your numbers breathe. Skip the fancy templates if they bury your metrics under decorative graphics - we've found that the simplest slides with the clearest numbers consistently outperform designed-to-death alternatives. (If you want the narrative to land, borrow a few sales deck storytelling patterns.)

Let's be honest about what a strong go to market pitch deck slide really is. It isn't about listing channels or dropping buzzwords. It's a single frame that proves you understand who buys, how they buy, what it costs to reach them, and why the math improves with funding. Nail that, and the follow-up meeting takes care of itself.

That founder who lost a follow-up meeting over $400/month in bad data tools? Prospeo replaces them all - 300M+ profiles, 125M+ verified mobiles, and 30+ ICP filters so your outbound channel validation runs on numbers investors can't poke holes in.

One platform. One line item. Unit economics that survive due diligence.

FAQ

How many slides should a GTM section have?

One slide for most decks. Series A may warrant two if you have channel-specific data, but a single slide with a clear funnel and metrics outperforms multi-slide overviews in investor reviews.

What if I don't have CAC or LTV data yet?

Use proxies: LOIs, pipeline value, pilot conversion rates, or vertical benchmarks. Even estimates with stated assumptions beat a blank. Pre-seed investors expect directional math, not audited financials.

Should I include outbound on my GTM slide?

Yes, if it's a core channel - but show the math: emails sent to replies to demos to closed, with conversion rates at each step. Keeping bounce rates under 5% and cost per verified contact under $0.02 is what makes outbound CAC defensible at early stages.

What's the biggest red flag on a GTM slide?

Listing five or more channels with no conversion data. Investors read this as "we haven't validated anything." Two channels with real numbers always beat six channels with none.