The 2026 SaaS Growth Playbook: Benchmarks, Strategies, and What Actually Works

January 2026 opened with a gut punch. SAP dropped 16%, ServiceNow fell 11%, and the S&P 500 Software & Services Index slid 8.7% to a nine-month low - amid rising concern that AI automation and agentic workflows could pressure traditional SaaS models. Meanwhile, Gartner forecasts $1.433 trillion in software spending this year, up 14.7% YoY. The money's still flowing. It's just flowing differently.

Median revenue expansion has settled at 26%, down from 30% in 2022. Growth-at-all-costs is dead. What replaced it is a sharper discipline where monetization beats acquisition, AI-native companies grow at twice the rate of traditional software, and efficiency separates compounders from stalls. The real struggle isn't knowing what to do - it's knowing what to do first when bandwidth is finite and every quarter matters more than the last.

Quick Version

Three things matter most right now:

- Monetization > acquisition. A 1% pricing improvement drives 12-13% more revenue - 4x the impact of a 1% improvement in acquisition. Most teams are CAC addicts: 10-person demand gen teams and zero people on pricing.

- AI-native companies grow 2x faster at nearly every ARR band. If you haven't operationalized AI by 2026, you're behind.

- Efficiency is the fundraising metric. The Rule of 40 is the benchmark investors anchor on. Growth alone doesn't cut it.

Stage-based priorities: under $1M, product-market fit. $1-5M, nail pricing. $5-20M, optimize CAC and expand existing accounts. $20M+, build the distribution machine.

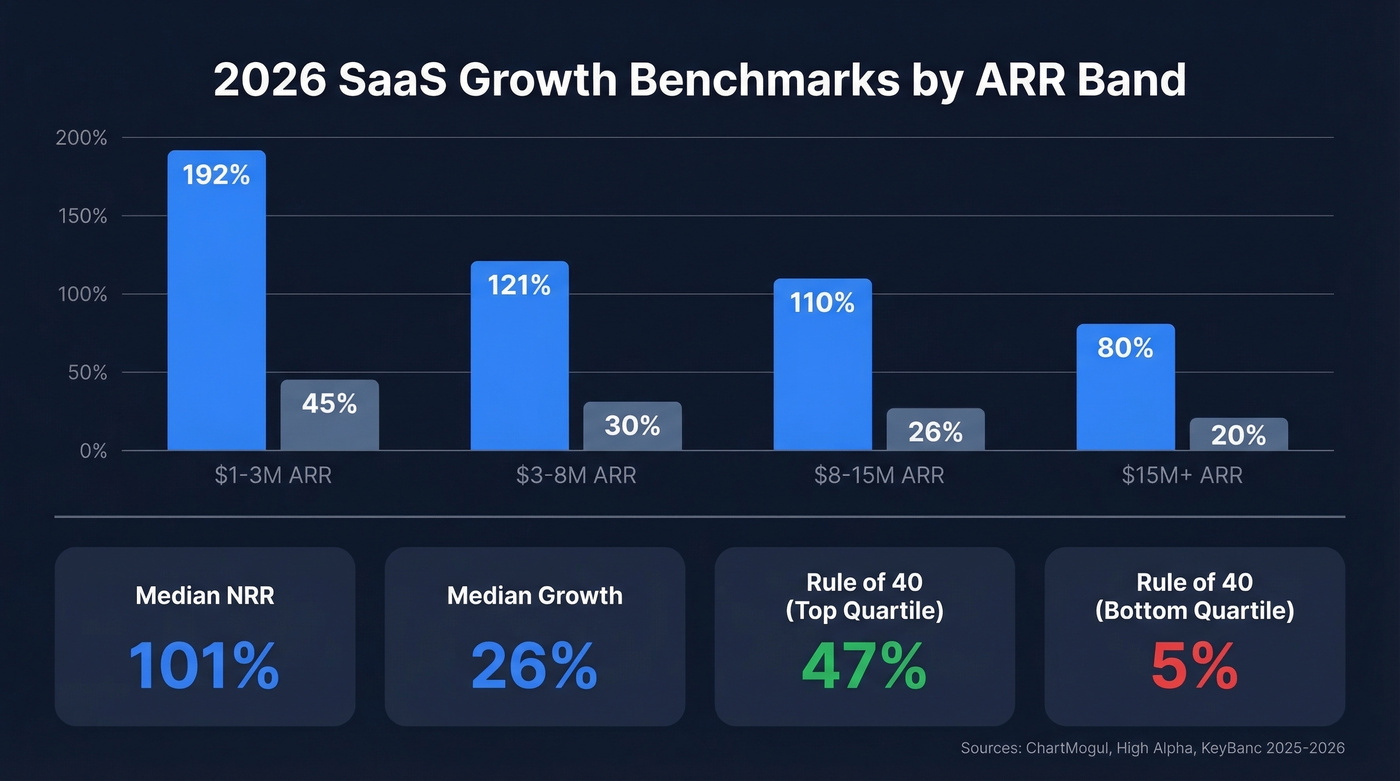

2026 SaaS Growth Benchmarks

Here's what the major benchmark datasets agree on:

- Median revenue growth: 26%

- Median NRR: 101%

- Bootstrapped ($3M-$20M ARR): 20% median growth, 51% at the 90th percentile, 104% median NRR, 92% median GRR

- Top-decile growth (ChartMogul): 192% at $1-3M ARR, 121% at $3-8M, 110% at $8-15M

- CAC payback varies heavily by ACV: 8 months (<$5K ACV), 14-18 months ($5K-$25K), 22 months ($25K-$50K), 24 months (>$50K)

The bootstrapped vs. VC-backed split matters less than people assume. Bootstrapped companies at $3M-$20M ARR grow at a 20% median with 90th-percentile performers hitting 51%, and that median is down from 30% the prior year, so the deceleration is real across cohorts. VC-backed companies push 25-30% median, with top-quartile performers clearing 50%.

Only 13% of SaaS startups reach $10M ARR even after 10 years. Best-in-class companies hit $1M ARR in 9 months. The median takes 2 years and 9 months. That gap compounds brutally.

The Rule of 40 tells the real story. High Alpha found that companies with strong NRR and efficient CAC payback average 71% growth and a Rule of 40 score of 47%. The low-NRR, high-payback cohort? 10% growth and a score of 5%. In our experience, teams that hit 104%+ NRR at $5M ARR rarely struggle to raise. Retention isn't a nice metric - it's the dividing line between companies that compound and companies that stall.

How AI Is Reshaping the Market

AI companies now represent 42% of the Cloud 100, up from 21% in 2024. That's not a trend. It's a takeover.

GenAI model spending alone is growing 80.8% this year. AI companies reach $100M ARR in 5.7 years versus 7.5 years for the broader Cloud 100. Cursor hit $100M in revenue in 12 months with 30 employees. The new ARR-per-employee benchmark for AI-native companies is $500K-$1M, compared to $200K-$400K for traditional SaaS - which means a 30-person AI company can outperform a 200-person legacy vendor on raw revenue output.

High Alpha's data shows 100% of companies founded in 2025 have AI as a core product component. Among sub-$1M ARR businesses, AI-native companies saw a 93% increase in revenue growth year-over-year. At the $1-5M band, AI differentiation drives 70% faster growth.

Bain's 2025 technology report maps four disruption scenarios: AI enhances SaaS, spending compresses, AI outshines SaaS, and AI cannibalizes SaaS entirely. The reality will be all four simultaneously, depending on the workflow. But enterprises don't rip and replace deeply integrated software overnight. Data gravity, security requirements, and compliance create switching costs that buy incumbents time. "Time" isn't "safety," though. If you're building SaaS in 2026 without AI at the core, you're building on borrowed time.

You just read that a 1% pricing improvement beats a 1% acquisition improvement by 4x. But when you do invest in acquisition, bad data destroys your CAC payback. Prospeo's 98% email accuracy and 7-day data refresh keep bounce rates under 4% - so every outbound dollar actually connects with a real buyer.

Stop burning pipeline budget on dead emails. Start with 75 free credits.

7 Strategies That Drive SaaS Growth

1. Monetization and Pricing

Use this if: you're past $1M ARR and haven't touched pricing in 12+ months. Skip this if: you're pre-PMF and still figuring out who your buyer is.

A 1% improvement in pricing drives 12-13% more revenue. A 1% improvement in acquisition? Roughly 3-4%. Most teams never run this math, which is why they keep hiring SDRs instead of hiring someone to fix their pricing page.

AI is forcing the issue. Variable inference costs mean you can't slap a per-seat price on an AI feature and hope the margins work. Metronome's field data shows the winning pattern: cost-plus credit systems with 30-50% markup, paired with annual credit buckets and spend caps to kill predictability anxiety. We've seen this play out firsthand - the companies that move to usage-based or hybrid pricing models almost always unlock expansion revenue they didn't know was there.

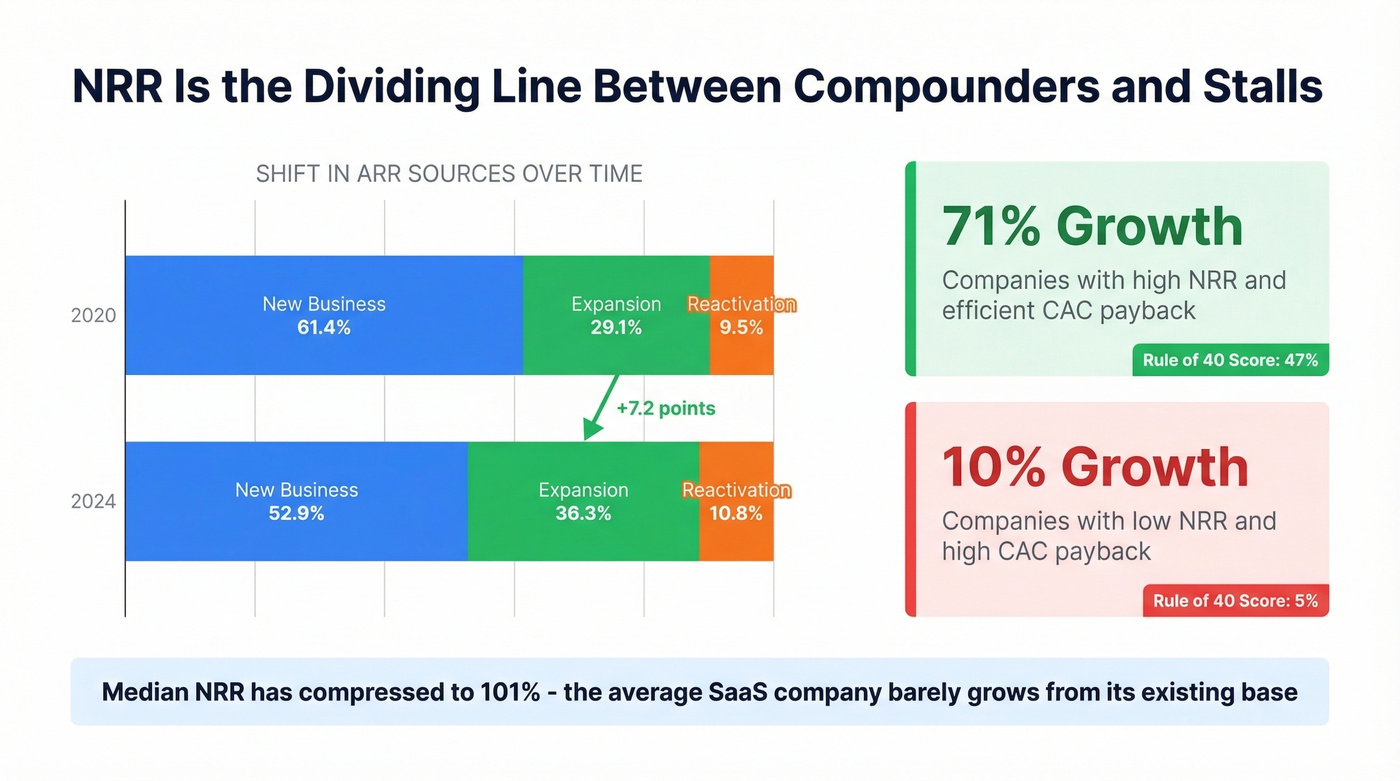

2. Net Revenue Retention and Expansion

Use this if: you're at $5M+ ARR and new logo acquisition is getting more expensive. Skip this if: you don't have enough customers to make expansion math work yet.

ChartMogul's data shows new business fell from 61.4% of ARR gained in 2020 to 52.9%, while expansion rose from 29.1% to 36.3%. Median NRR has compressed to 101%, meaning the average SaaS company barely grows from its existing base. High-NRR companies grow at 71%. Low-NRR companies grow at 10%.

Fix retention first. Expansion follows.

HubX used salvage offers that retained 63% of would-be churners and recovered $106K in revenue within three months. Most teams pour money into top-of-funnel while their existing customers quietly leave. That's the most expensive leak in software, and it's the one nobody wants to talk about in board meetings.

3. Product-Led Growth

Use this if: your product delivers value without a sales conversation. Skip this if: you're selling $100K+ enterprise contracts where PLG is a distraction.

PLG companies grow 1.9x faster and burn 50% less cash than sales-led peers, per OpenView's data. The mechanics that matter: time-to-value under 2 minutes, a 40% activation threshold (if fewer than 40% of signups hit your aha moment, redesign onboarding), and reverse trials that convert 25-40% better than pure freemium.

Here's the thing - PLG isn't a strategy you bolt on. It's an organizational commitment. Your product team, your marketing team, and your data team all need to be aligned around the self-serve funnel. Half-hearted PLG is worse than no PLG at all because it splits focus without delivering results.

4. Outbound Data Quality

Use this if: outbound is any part of your growth motion. Skip this if: you're purely inbound or PLG with zero outbound.

CAC rose 14% in 2024 alone. More money is chasing outbound, and more money gets wasted when the data underneath is garbage. Bad emails don't just bounce. They burn your sending domain, tank deliverability across every sequence, and inflate CAC in ways that don't show up in dashboards until it's too late.

Meritt's experience is instructive: they ran a 35% bounce rate before switching to Prospeo. After the switch, bounce rate dropped to under 4%, and pipeline tripled from $100K to $300K per week. With 98% email accuracy and a 7-day data refresh cycle versus the 6-week industry average, clean data turns outbound from a cost center into a growth engine.

The consensus on r/sales is blunt: if your bounce rate is above 5%, your data provider is the problem, not your copy. We'd agree. We've tested dozens of providers over the years, and the difference between 80% accuracy and 98% accuracy isn't 18 percentage points - it's the difference between a functioning outbound program and a domain reputation crisis.

If you're trying to diagnose the root cause, start with email deliverability and your sender reputation before you scale volume.

5. Distribution-First Thinking

Use this if: you're at $5M+ ARR and still spending 70% of budget on product. Skip this if: your product isn't ready for scale yet.

Five years ago, 70% of VC funding went to product and 30% to GTM. Today it's inverted. The average company now runs 106 SaaS apps, down from 112 - consolidation pressure is real. The best product with mediocre distribution loses to a good product with great distribution every time.

If your average deal size is under $10K and you're spending more on engineering than distribution past $5M ARR, you're optimizing the wrong side of the equation. At scale, distribution is the bottleneck, not product.

If you're rebuilding your motion, it helps to map your go-to-market strategy and tighten pipeline health metrics early.

6. Global Expansion and Localization

Use this if: you have product-market fit in one geography and want to expand. Skip this if: you haven't nailed your home market yet.

This one's underrated. Aithor saw a 9% revenue uplift simply by localizing payment methods. US and UK markets saw 14% revenue growth after localization. It's not glamorous work, but removing friction from the payment flow is pure margin - no additional CAC required. For teams between $8M and $20M ARR, localization is often the highest-ROI project nobody's prioritizing.

7. Community and Content Compounding

Use this if: you're building for a niche audience that congregates online. Skip this if: your buyers don't participate in communities.

Reddit has quietly become one of the best acquisition channels for SaaS. Threads rank on Google and compound like SEO - a helpful answer posted today drives signups for years. The playbook on r/microsaas is straightforward: value-first, pitch-second. Practitioners report 30%+ reply rates when they move quickly after a post goes live.

Let's be honest: most SaaS content marketing in 2026 is indistinguishable slop. The companies winning with content are the ones where actual practitioners write about actual problems. Community-driven content compounds because it earns trust, and trust is the one thing AI can't manufacture at scale.

If you want a tighter system, start with B2B content marketing and track the right funnel metrics so content actually ties to revenue.

The Metrics That Matter

Every guide tells you to "track your NRR" without telling you what good looks like at your stage. Here's what good looks like:

| Metric | 2026 Benchmark | Why It Matters |

|---|---|---|

| ARR Growth | 26% median | Core health signal |

| Rule of 40 | 40%+ (top: 47%) | The fundraising benchmark |

| NRR | 101-104% | Compound growth engine |

| GRR | 92% median | Floor under your business |

| CAC Payback | 8-24 mo by ACV | Capital efficiency signal |

| LTV:CAC | 3:1+ | Unit economics viability |

Gross margin target: 75%+ for software subscriptions. Below that, you're either spending too much on infrastructure or your pricing doesn't reflect your value.

Investors have shifted from "how fast can you grow?" to "show me the path to profitability." A company growing 20% with 25% margins is more fundable than one growing 40% while burning 30%. That's the new math, and the Rule of 40 is how they score it.

If you're pressure-testing retention, run a proper churn analysis and align on what is churn definitions before you present numbers to investors.

AI-native companies hit $500K-$1M ARR per employee because they eliminate waste. Your outbound should work the same way. Prospeo gives you 300M+ verified profiles with 30+ filters - buyer intent, technographics, headcount growth, funding - so you target in-market accounts instead of spraying cold lists.

Teams using Prospeo book 26% more meetings than ZoomInfo users.

Stage-by-Stage FAQ

What's a good SaaS growth rate in 2026?

Median revenue expansion is 26%, with top-quartile companies hitting 50%+. Bootstrapped companies at $3M-$20M ARR median 20%, while VC-backed companies push 25-30%. At the $1-3M ARR band, top-decile companies grow 192%.

How do AI SaaS companies grow faster?

AI-native companies grow 2x faster than traditional software at nearly every ARR band. They reach $100M ARR in 5.7 years versus 7.5 years on average, with ARR per employee of $500K-$1M compared to $200K-$400K for traditional SaaS. The efficiency gap is staggering and it's only widening.

What's the most impactful lever?

Monetization optimization. A 1% improvement in pricing drives 12-13% more revenue - 4x the impact of a 1% improvement in acquisition. Most teams over-invest in lead generation and under-invest in pricing. If you haven't revisited your pricing in the last year, that's your highest-leverage project right now.

What is the Rule of 40?

Your growth rate plus profit margin should exceed 40%. Top-performing companies in 2026 score 47% on this metric. It's become the primary benchmark investors use to evaluate SaaS businesses, replacing raw growth rate as the north star.

How long does it take to reach $10M ARR?

Only 13% of SaaS startups reach $10M ARR even after 10 years. Best-in-class companies hit $1M in 9 months and scale from there. The median time to $1M is 2 years and 9 months, and the gap compounds at every stage. Our advice at this phase: obsess over retention before you scale acquisition, because every percentage point of churn you eliminate accelerates the path to $10M dramatically.