How to Sell to Banks Without Wasting 18 Months

Banks will spend $857.5 billion on IT in 2026 - up 9.5% year-over-year. Seventy-five percent of bank CFOs expect tech budgets to keep rising, with nearly half planning increases above 10%. The opportunity is massive. The execution is where everyone stalls.

A founder on r/fintech launched a product for banks and loan brokers, landed six clients in six weeks, then watched growth flatline. The problem wasn't product-market fit - it was $20K ARR spread across six accounts. Underpricing killed perceived value, and the team had no playbook for bank procurement. That's the pattern we see constantly: founders build something banks genuinely need, then lose 12-18 months figuring out how banks actually buy.

The short version: Start with community banks, not Tier 1 globals. Price your initial engagement at $500-$2K/month to stay under procurement escalation thresholds. Get SOC 2 Type II before you start serious outbound, not after a bank asks.

How Bank Procurement Actually Works

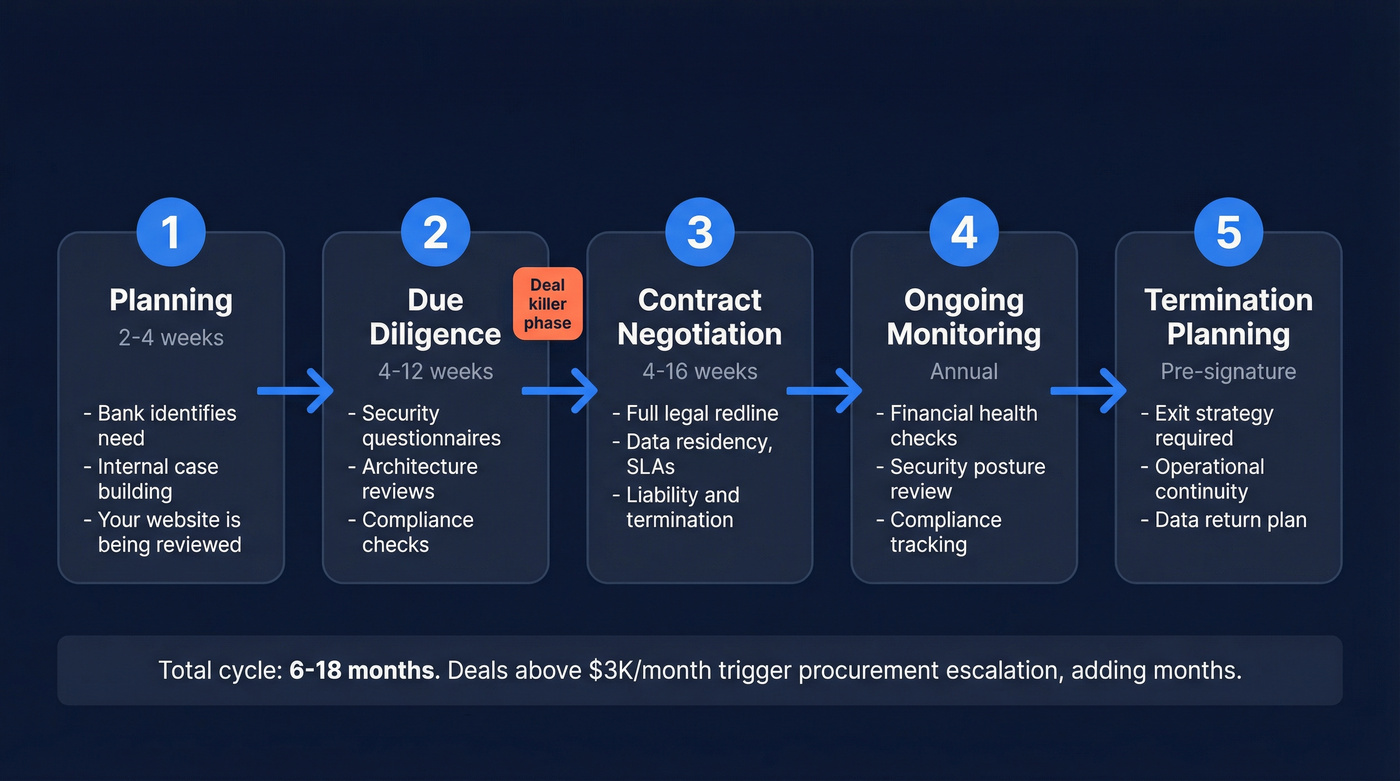

Bank procurement isn't a sales funnel. It's a regulatory process. The June 2023 interagency guidance from the Fed, FDIC, and OCC established a five-phase third-party risk management framework that most banks now follow:

1. Planning (2-4 weeks). The bank identifies a need and assesses whether a third party is the right path. Your champion is building the internal case. You won't be involved - but your website, security page, and case studies are being scrutinized right now.

2. Due diligence (4-12 weeks). Security questionnaires, architecture reviews, compliance checks. Expect IT to tear apart everything from your encryption standards to your incident response plan. This is the phase that kills unprepared vendors.

3. Contract negotiation (4-16 weeks). Banks don't use your standard SaaS agreement. They'll redline everything - data residency, SLAs, liability caps, termination rights. Their legal team has done this a thousand times. Yours probably hasn't. (If you need a negotiation baseline, start with the concept of an anchor before you walk into redlines.)

4. Ongoing monitoring. Post-signature, the bank tracks your financial health, security posture, and compliance annually.

5. Termination. Banks plan exit strategies before they sign. They need to know they can unwind without operational disruption.

The full cycle runs 6-18 months. Anything above $3K/month in vendor spend often triggers procurement escalation, adding months. Stay under that threshold initially.

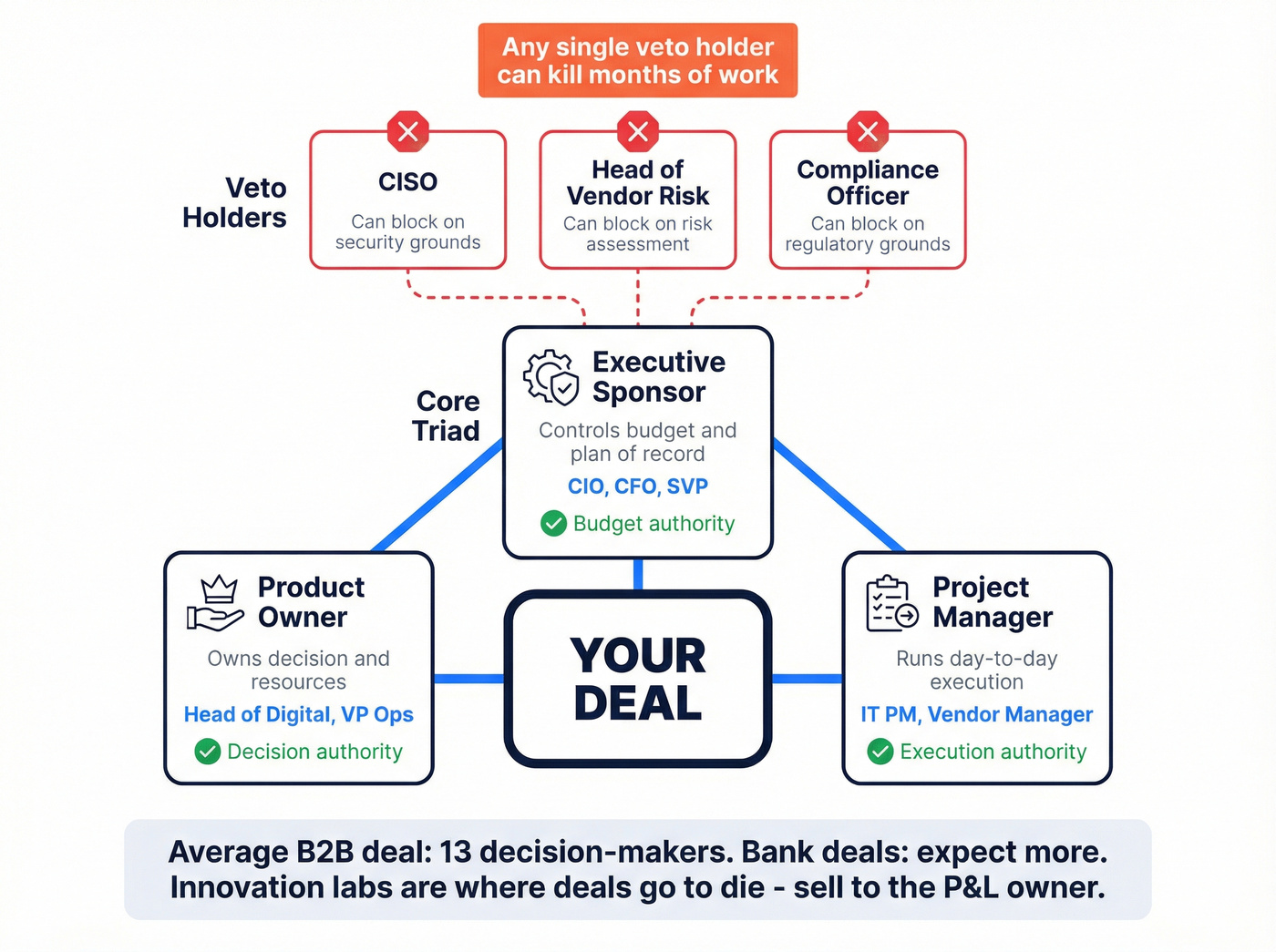

The Stakeholder Map

Bank deals don't close because one person said yes. They close because nobody said no. Martal's research puts the average B2B deal at 13 decision-makers. In banking, expect more.

Here's the core triad you need:

| Role | What They Control | Typical Titles |

|---|---|---|

| Executive Sponsor | Budget, plan of record | CIO, CFO, SVP |

| Product Owner | Decision, resources | Head of Digital, VP Ops |

| Project Manager | Day-to-day execution | IT PM, Vendor Manager |

Beyond the triad, the CISO, Head of Vendor Risk, and a compliance officer can each veto the deal independently. Any one of them can kill months of work with a single "no."

A word on innovation labs: they're where deals go to die. They'll run a pilot, write a report, and shelve it. Sell to the line of business that owns the P&L, not the team that runs experiments. (This is also why team selling matters more in banks than most verticals.)

Qualifying Deals with MEDDPICC

Long sales cycles punish unqualified pipeline. Two MEDDPICC elements matter most when selling to banks:

Metrics. Banks expect 5-10x value delivered vs. product cost. "We'll save you time" isn't a metric. "We'll reduce compliance processing time by 40%, saving $380K annually" is. Build the P&L business case before the bank asks for it - because they will ask, and they'll want hard numbers, not hand-waving. (If you want a tighter qualification flow, use MEDDIC discovery questions as your base.)

Competition. Your biggest competitor often isn't another vendor. It's the bank's internal team deciding to build it themselves. Every large bank has a build-vs-buy bias baked into its culture. Ask your champion directly: "Is there an internal team that could take this on?" If the answer is yes, reframe from "our product" to "your team's time is better spent elsewhere."

Decision Process. Ask: "Walk me through every approval this needs before a contract gets signed." That list typically includes risk assessment, vendor risk review, compliance review, IT/security assessment, CFO approval, committee or board approval, and legal review. If your champion can't map this, they aren't a real champion.

For complex deals, plan for 12-24 months. Expect 20-40% pilot-to-paid conversion depending on champion strength. If you're qualifying correctly, you'll kill half your pipeline early. That's the point. (More broadly, this is standard enterprise B2B sales math.)

Compliance and Security

SOC 2 Type II is table stakes, not a differentiator. No cert means no conversation. ISO 27001 is increasingly expected in bank vendor reviews. PCI DSS is mandatory if you touch card data.

Before you start outbound, have these ready:

- SOC 2 Type II report (current, not expired)

- Documented incident response plan with tested RTO/RPO

- Data residency clarity - where exactly is customer data stored?

- Encryption standards for data at rest and in transit

Fintech compliance costs jumped roughly 30% worldwide between 2023 and 2024. Budget for compliance before you budget for sales headcount. We've watched founders treat this as a "later" problem, then lose a deal six months in because they couldn't produce a current SOC 2 report. It's infuriating to watch, and it's entirely preventable.

Let's be honest about the math: if your deal size is under $50K annually, compliance prep will cost more than your first year of revenue from any single bank. Do it anyway. The alternative is building pipeline you can never close. (If you're pressure-testing the economics, model it alongside your cost to acquire customer.)

Mapping 13+ stakeholders per bank deal takes months - unless you have the data. Prospeo gives you verified emails and direct dials for CIOs, CFOs, CISOs, and Heads of Vendor Risk across 300M+ profiles with 98% email accuracy. Filter by industry, job title, and company size to build your bank stakeholder map in minutes, not weeks.

Stop guessing who controls the budget. Start with verified contacts.

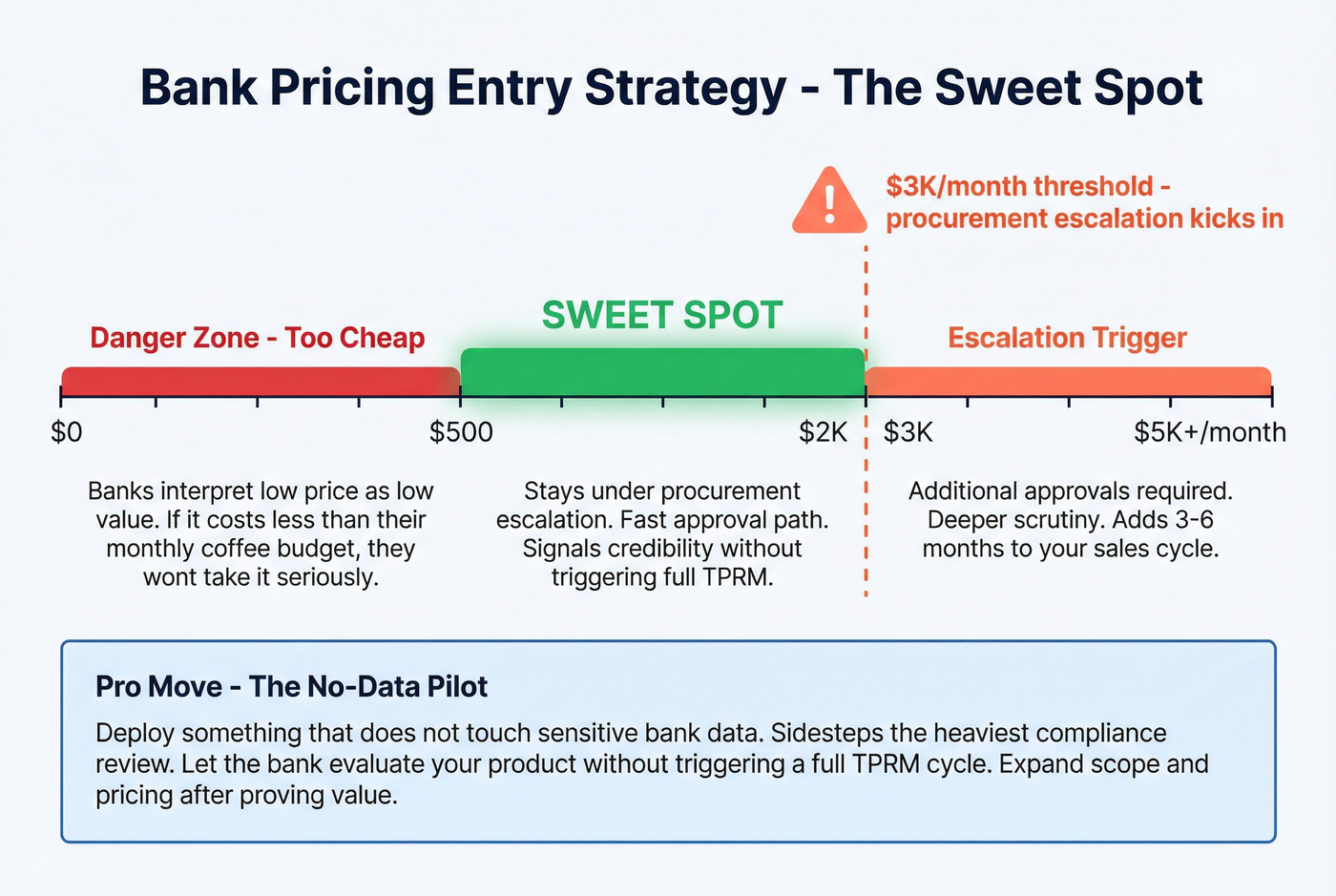

Pricing and Entry Strategy

The $500-$2K/month range is the sweet spot for initial bank engagements. Above $3K/month triggers procurement escalation - additional approvals and deeper scrutiny that can add 3-6 months to your cycle.

One tactic from a Reddit thread worth stealing: start with a "no-data pilot." Deploy something that doesn't touch sensitive bank data. This sidesteps the heaviest compliance review and lets the bank evaluate your product without triggering a full TPRM cycle. Once you've proven value, expand scope and pricing. This works especially well when you're selling fintech solutions to institutions that haven't adopted your product category before.

Underpricing is just as dangerous as overpricing. That founder who landed six clients at ~$20K total ARR? Banks interpreted the low price as low value. Price signals credibility in financial services more than almost any other vertical. If a compliance officer sees your product costs less than their monthly coffee budget, they'll assume it isn't serious. (If you need a clean framework for pricing conversations, use walk away point thinking before you discount.)

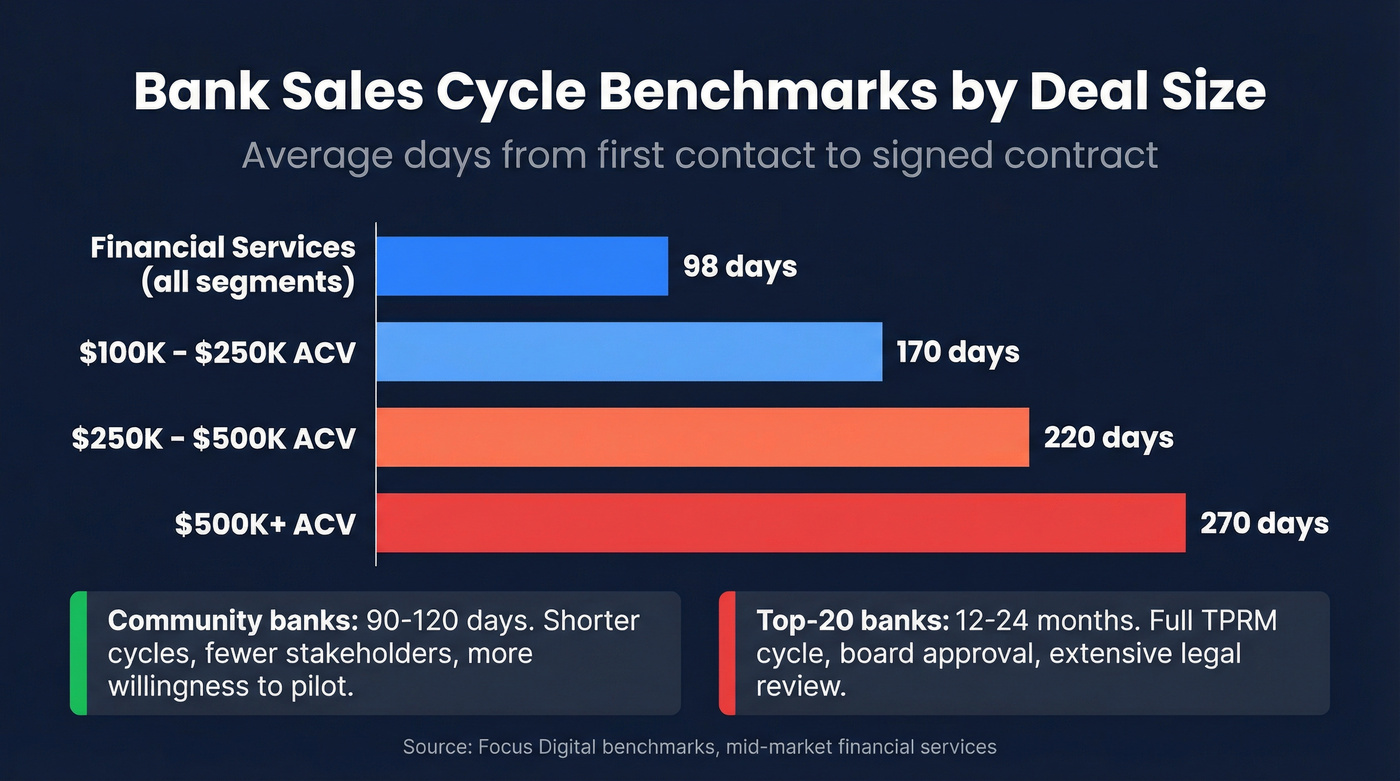

Cycle Benchmarks by Deal Size

| Segment | Avg. Cycle Length |

|---|---|

| Financial services (all) | 98 days |

| $100K-$250K ACV | 170 days |

| $250K-$500K ACV | 220 days |

| $500K+ ACV | 270 days |

These Focus Digital benchmarks reflect mid-market financial services broadly. Community banks close in 90-120 days; a top-20 bank deal easily stretches past 12 months.

Start with regional banks. Shorter cycles, fewer stakeholders, more willingness to pilot. Win three to five regionals, build case studies with hard metrics, then approach enterprise banks with proof. Skip this step and you'll burn through runway pitching Tier 1 institutions that won't close for a year. (To keep the motion consistent, document your sales activities and review them weekly.)

Finding Bank Decision-Makers

Bank org charts are opaque. Titles vary wildly - one bank's "VP of Digital Transformation" is another's "Director of Innovation." The three core banking providers (FIS, Fiserv, Jack Henry) serve over 70% of depository institutions, so channel partnerships through those ecosystems can shortcut months of cold prospecting.

For direct outbound, verified contact data isn't optional. When your sales cycle is already 6-18 months, a bounced email wastes weeks of momentum. In our experience, the biggest time sink in bank outreach isn't writing the email - it's finding the right person and confirming they're still in that role. Bank executives rotate frequently, and generic databases go stale fast. Tools like Prospeo with a 7-day data refresh cycle and 30+ search filters (including technographics to find banks running specific core platforms) help solve that "first 30 days" problem before the long procurement slog begins. (If you're building lists at scale, start with a clear ideal customer profile and then layer in firmographic filters.)

Bank deals take 6-18 months. Every week spent hunting for the right VP of Operations or Head of Digital is a week your competitor is already in conversation. Prospeo's 30+ search filters - including headcount growth, funding, and technographics - let you pinpoint banks actively investing in your category. At $0.01 per email, building pipeline costs less than a single hour of your SDR's time.

Find every decision-maker at your target banks before your next meeting.

Mistakes That Kill Bank Deals

Skipping compliance prep. Showing up without SOC 2 Type II is like showing up to a job interview without a resume. You won't get a second chance.

(If you're running outbound while you prep, keep your deliverability clean with an email deliverability guide.)

Pitching too broad. "We're a platform that does X, Y, and Z" loses to "We solve this one painful problem, and here's the P&L impact." Selling to banks means leading with a single, quantifiable outcome tied to a line-of-business pain point. Save the platform story for the expansion conversation.

Ignoring bank timelines. Pushing for a 30-day close on a deal that structurally requires six months of procurement review destroys credibility. Your urgency isn't their urgency.

Single-champion dependency. Your champion just accepted a role at another bank. If you haven't built relationships across the full stakeholder triad, the deal dies with their departure. We've seen this happen three times in the last year alone with companies in our network. Always have at least two internal advocates.

FAQ

How long does it take to close a deal with a bank?

Community banks typically close in 3-6 months. Tier 1 globals take 12-24 months including security review, legal negotiation, and board approval. Deals above $250K ACV average 220 days across financial services.

Do I need SOC 2 to sell to banks?

Yes - get certified before you start outbound. The certification process takes 3-6 months, so waiting until a bank requests it means losing that deal entirely. Budget $30K-$80K for your first audit.

What's the best entry point for bank sales?

Community and regional banks under $10B in assets. Win three to five, build case studies with hard ROI metrics, then approach enterprise banks with proof. Regional deals close 3-4x faster than Tier 1 globals.

How should I price software for banks?

Stay at $500-$2K/month for initial engagements. Above $3K/month triggers formal procurement escalation at most institutions. Use a crawl/walk/run model - prove value first, expand pricing after ROI is documented.

How do I find verified contacts at banks for outbound?

Bank org charts are notoriously opaque, and generic databases often return outdated titles. You need a data source with frequent refresh cycles and filters for institution size, technology stack, and department. Prospeo's 30+ search filters and 7-day refresh cycle are built for exactly this kind of targeted outbound - the 75-credit free tier is enough to test a regional bank campaign before committing.