Fintech Lead Generation: The Practitioner's Playbook for 2026

Your SDR just burned through 2,000 credits on a "fintech companies" list. Bounce rate: 34%. Three compliance officers replied - to tell you to stop emailing them. The VP of Sales wants to know why pipeline is flat.

Fintech lead generation punishes lazy targeting harder than almost any other vertical, and most teams learn that the expensive way. Financial services buyers convert at just 1.9% from website visits. Sales cycles stretch 6-12 months. Compliance and legal sit on every buying committee, and they don't fill out your gated whitepaper form. As one practitioner on r/b2bmarketing put it, buyers "ghost generic outreach" because "secure and scalable" positioning is invisible - every fintech vendor says it. The teams that win pipeline here do three things differently: they narrow their ICP to a painful degree, they time outreach to trigger events, and they obsess over data quality because one bad bounce spike can torch a domain in a trust-sensitive industry.

Here's the thing: if your average contract value is under $25K, you don't need a $15K/year data platform. You need 50 perfect-fit accounts, verified contact data, and a trigger-based outreach motion. The rest is noise.

What You Need (Quick Version)

- Narrow your ICP by sub-vertical. "Fintech companies" isn't an ICP. "Mid-market payment processors handling 50k+ daily transactions who need real-time fraud detection" is. Use an Ideal Customer Profile scoring rubric so reps don’t “wing it.”

- Lead with triggers, not lists. A funding round, a compliance hire, a banking partner change - these create buying windows. Cold lists don't. If you need a system, borrow a framework for tracking sales triggers.

- Verify everything. A 35% bounce rate doesn't just waste credits. It damages your sender reputation in an industry where trust is the product. (More on email bounce rate benchmarks and fixes.)

Starter stack for a solo founder or small team: Prospeo for verified data and intent signals, Instantly for outreach sequencing, HubSpot for CRM - typically under $200/mo for a 1-3 seat setup.

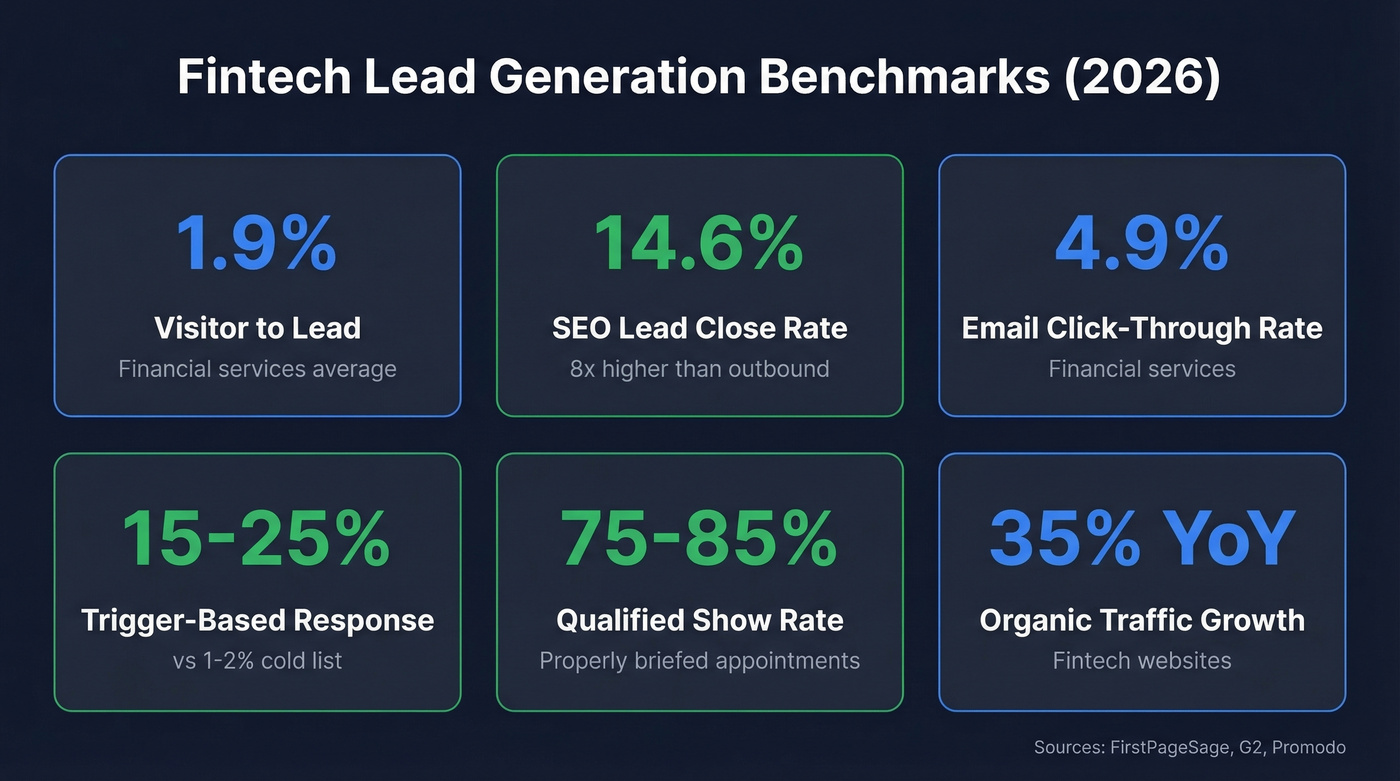

Benchmarks That Actually Matter

Before you build anything, calibrate your expectations. Fintech benchmarks look different from general B2B, and most teams set goals based on SaaS norms that don't apply here.

| Metric | Benchmark | Context |

|---|---|---|

| Website visitor to lead | 1.9% | Financial services avg |

| SEO lead close rate | 14.6% | vs 1.7% outbound |

| Email CTR | 4.9% | Financial services |

| Trigger-based response | 15-25% | vs 1-2% cold list |

| Show rate (qualified) | 75-85% | Properly briefed appointments |

| Organic traffic growth | 35% YoY | Fintech websites |

The standout number: SEO-driven leads close at 14.6% versus 1.7% for outbound. That's an 8x difference. It doesn't mean you skip outbound - it means you invest in content that compounds while running trigger-based outbound for near-term pipeline. (If you want the mechanics, see SEO sales leads.)

The 4.9% email CTR in financial services is actually strong compared to most B2B verticals. When fintech buyers open your email, they engage. The problem is getting them to open it in the first place. Top fintech sites average 6+ minutes per visit and 6.5 pages per session, with organic search driving nearly 20% of traffic - further proof that SEO compounds here.

7 Strategies That Fill Fintech Pipeline

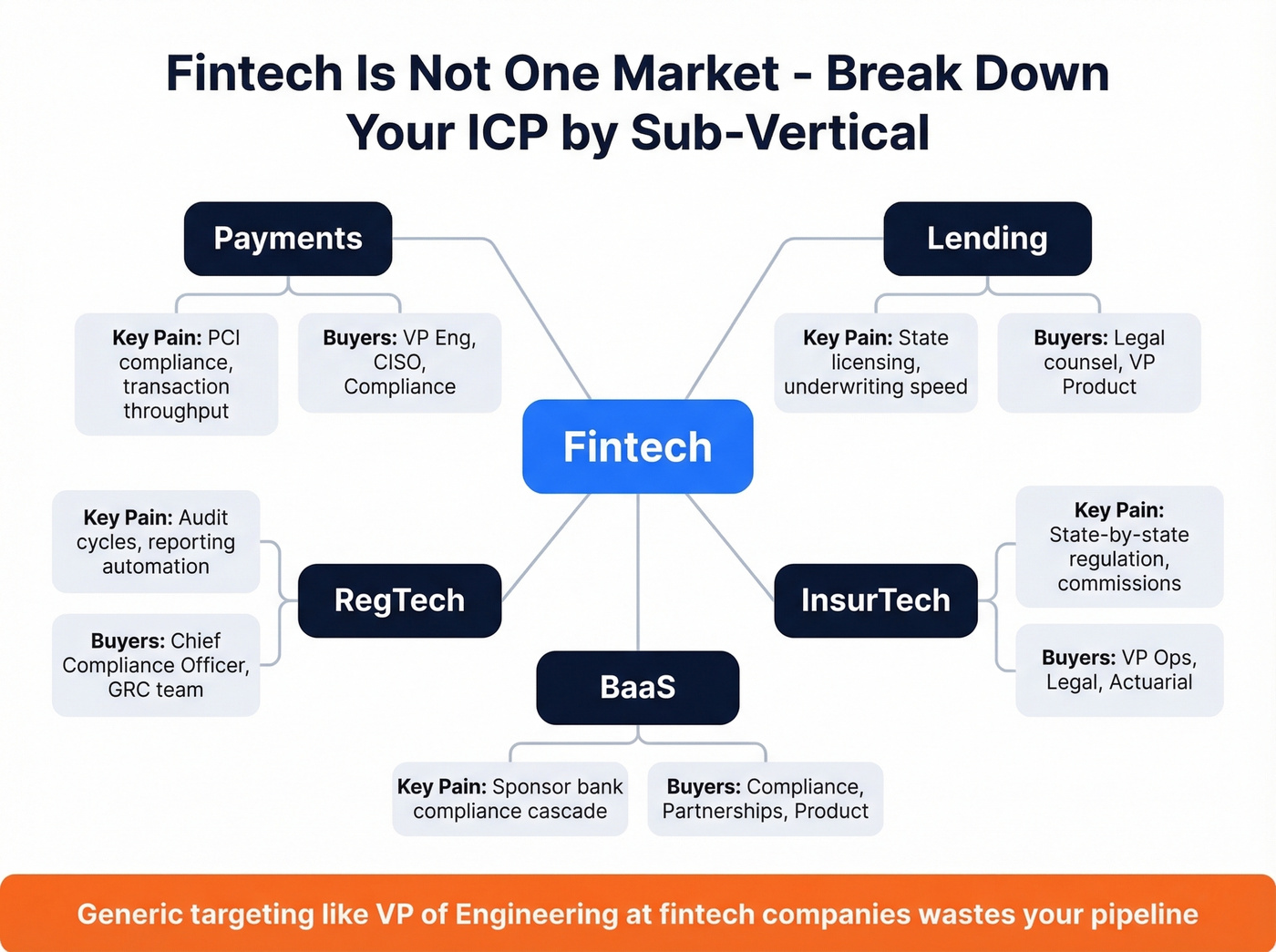

1. Hyper-Narrow ICP by Sub-Vertical

"Fintech" isn't a market. It's five or six markets wearing a trench coat.

Payments companies care about PCI compliance and transaction throughput. Lending platforms worry about state licensing and underwriting speed. RegTech buyers live in audit cycles. InsurTech is regulated state by state with commission-sharing constraints that shape every procurement decision. BaaS providers navigate complex compliance arrangements where the sponsoring bank's regulatory obligations cascade down to every partner.

Your ICP needs to reflect this. Instead of "VP of Engineering at fintech companies," try "VP of Engineering at mid-market payment processors handling 50k+ daily transactions who need real-time fraud detection APIs." That specificity changes everything downstream - your content topics, your outreach messaging, your ad targeting, even which triggers you monitor. Whether you're prospecting into payments startups or targeting enterprise compliance buyers, specificity beats volume every time.

The buying committee shifts by sub-vertical too. Payments deals pull in security and compliance early. Lending deals involve legal counsel and sometimes external regulators. If your SDRs don't know who else is in the room, they're setting meetings that stall at the next gate.

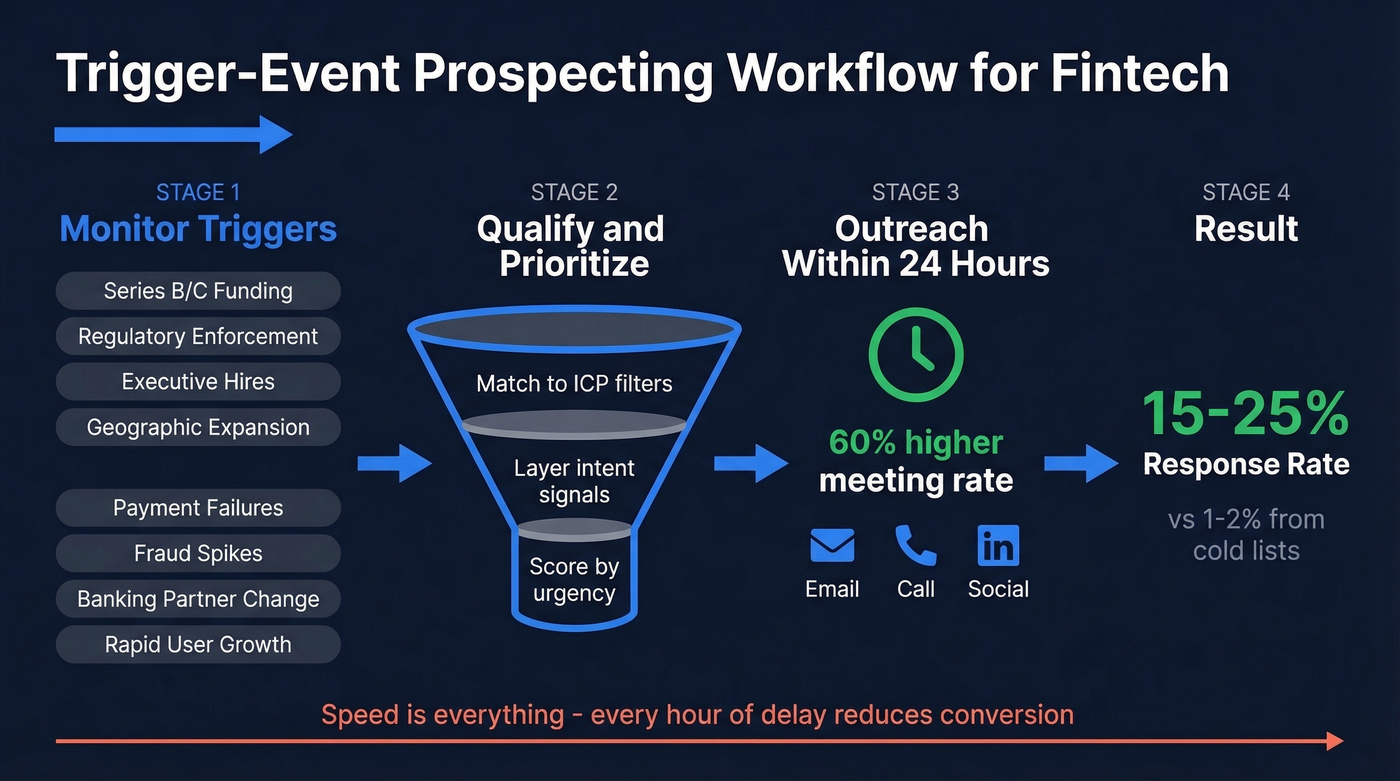

2. Trigger-Event Prospecting

This is the single highest-leverage strategy for fintech outbound.

Trigger-based outreach generates 10-15x higher response rates than generic cold lists, with 15-25% response rates versus 1-2% for purchased-list blasts. Properly qualified fintech appointments hit 75-85% show rates, and companies that act on triggers see a 30-50% increase in conversion rates overall.

Eight triggers matter most in fintech:

- Regulatory enforcement - a company that just got fined is suddenly budget-approved for compliance tooling

- Series B/C funding - new capital means new infrastructure spend, and it's the strongest signal for timely outreach

- Payment failures - public incidents create urgency for reliability solutions

- Fraud spikes - reported breaches open doors for security vendors

- Geographic expansion - new markets mean new compliance requirements

- Banking partner changes - forced migration creates buying windows

- Rapid user growth - scaling infrastructure pain is real and immediate

- Executive hires - new leaders bring new vendor evaluations

Speed is everything. Contacting within 24 hours of a trigger increases meeting likelihood by 60%. That means you need a system, not a manual process. Layer intent data with job change and funding signals to prioritize outreach by urgency, not alphabetical order. (Related: identifying buying signals.)

3. Intent-Based Targeting Over List Volume

Buying a list of 10,000 fintech contacts and blasting them is the fastest way to burn your domain and your budget simultaneously. Intent signals flip the model: instead of "who fits my ICP?" you're asking "who fits my ICP and is actively looking for a solution right now?"

The signals that matter: compliance hiring spikes (they're building a team to solve a problem), vendor migration chatter (they're evaluating alternatives), security and legal content consumption (they're researching), and pricing-to-product page visit patterns (they're comparing). When you stack these signals on top of firmographic filters, your outreach list shrinks from thousands to dozens - but those dozens actually reply. (If you’re formalizing this, use intent based segmentation.)

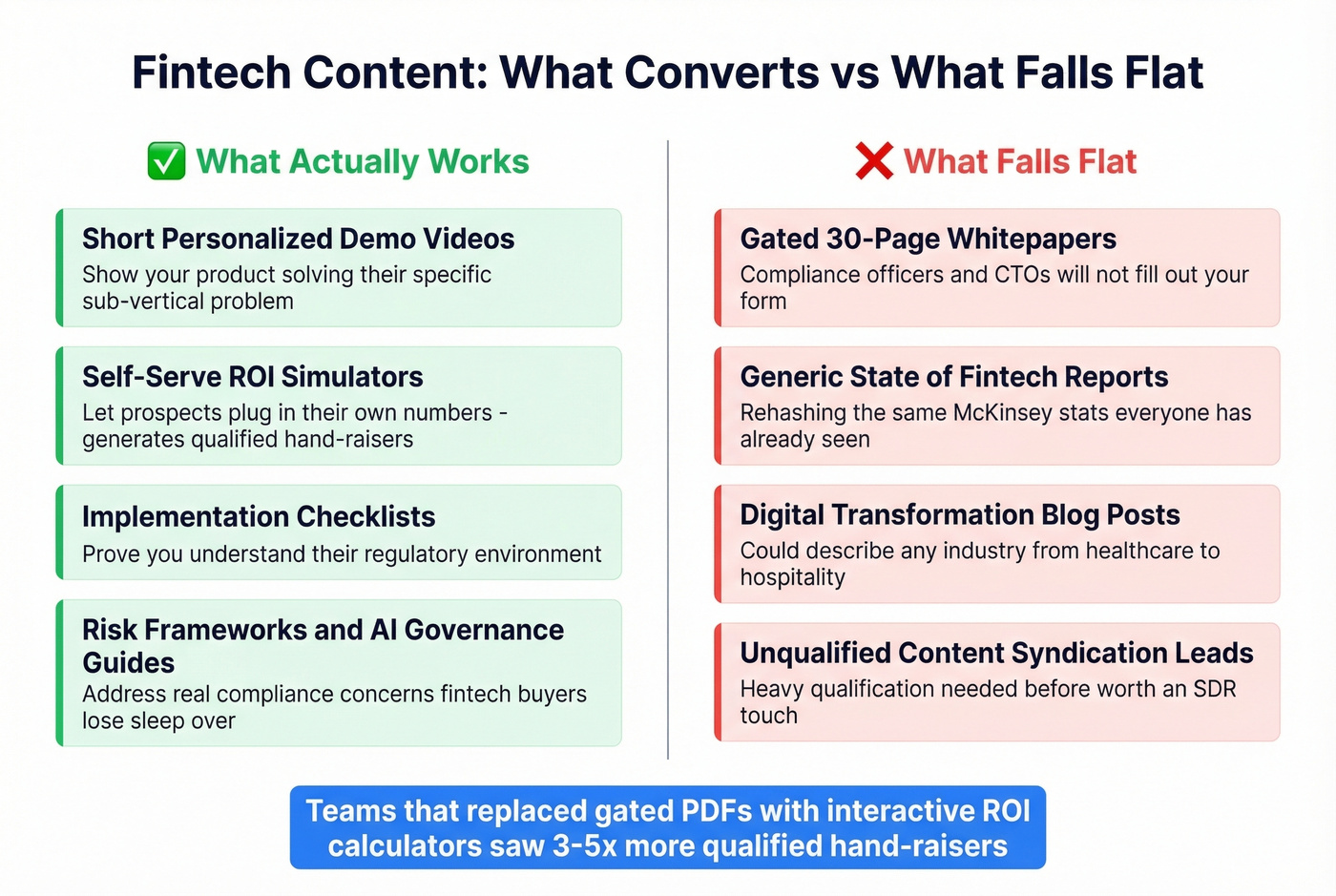

4. Content That Converts Fintech Buyers

Stop writing whitepapers. Compliance officers and CTOs at fintech companies don't download 30-page PDFs behind a form. They've been burned by vendor content too many times.

What works: short personalized demo videos showing your product solving their specific sub-vertical problem outperform everything else. Self-serve ROI simulators where prospects plug in their own numbers generate qualified hand-raisers. Implementation checklists that prove you understand their regulatory environment build trust faster than any sales deck. Risk frameworks and AI governance guides address real compliance concerns that fintech buyers lose sleep over. We've seen teams that replaced gated PDFs with interactive ROI calculators increase qualified hand-raisers 3-5x.

What falls flat: gated whitepapers requiring a work email, generic "state of fintech" reports rehashing the same McKinsey stats everyone's already seen, and blog posts about "digital transformation" that could describe any industry from healthcare to hospitality. Content syndication can supplement top-of-funnel volume, but watch lead quality closely - fintech syndication leads often need heavy qualification before they're worth an SDR's time.

The content themes that resonate are risk, ROI math with transparent assumptions, implementation timelines with realistic milestones, and AI governance. (More frameworks: what is B2B content marketing.)

5. Multi-Channel Outbound With Compliance Guardrails

Fintech outbound works best as a coordinated sequence across email, phone, and social - but you can't ignore the compliance layer. Since January 2025, the FCC's updated TCPA rules require one-to-one consent per seller. No more blanket opt-ins covering multiple partners.

What this means practically:

- Explicit, unchecked checkboxes for consent

- Digital signatures or confirmation emails

- Separate consent by channel (call consent doesn't cover SMS)

- Consent records stored in your CRM

Let's be honest: most fintech SDR teams aren't fully compliant here. Getting this right isn't just legal protection - it's a competitive advantage when your competitors' emails are landing in spam. (Also worth tightening: email deliverability basics.)

6. ABM for Enterprise Fintech Deals

For six-figure contracts to enterprise fintech companies, ABM isn't optional - it's the only approach that matches the buying process. These deals involve 6-24 month cycles with buying committees spanning compliance, product, finance, and sometimes external legal counsel. (If you’re blending sales + marketing, follow account-based selling best practices.)

Skip this strategy if your deal sizes are under $50K or your team doesn't have dedicated marketing support. ABM without proper resourcing just becomes expensive outbound with a fancier name.

ABM measurement looks different from demand gen. You're tracking account engagement, buying group coverage, and pipeline quality over long horizons - not MQLs per month. AVEVA's ABM program targeting GSK generated 2,000 visits to a personalized microsite, created 46 new relationships, and built £7M in pipeline. The timeline wasn't weeks. It was quarters.

Multi-threading is essential. If your only contact at a target account is the VP of Product, you're one reorg away from a dead deal.

7. Partnerships as a Pipeline Channel

This is the most underrated channel in fintech lead generation. A warm introduction from a platform partner your prospect already trusts beats 100 cold emails. Every time.

The model: fintech SaaS + vertical SaaS or platform partnerships. If you sell compliance tooling, partner with the banking-as-a-service platforms your prospects already use. If you sell fraud detection, partner with payment processors who need to offer it as a value-add. The partnership creates a warm pipeline that bypasses the cold outreach gauntlet entirely.

We've seen teams spend months optimizing cold email copy when a single integration partnership would've generated more qualified pipeline in the first 30 days.

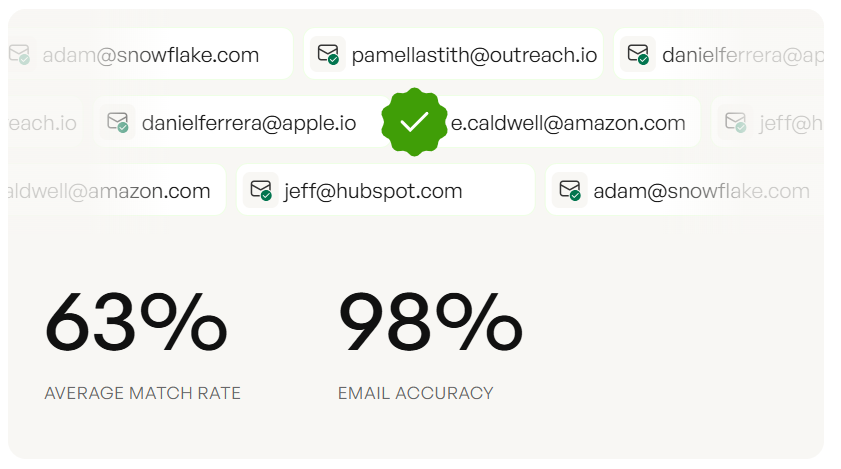

A 34% bounce rate doesn't just waste credits - it torches your domain in an industry where trust is everything. Prospeo's 5-step verification and 7-day data refresh keep bounce rates under 4%, so your fintech outreach actually lands.

Replace your stale fintech lists with 98% accurate, verified contact data.

The Right Tool Stack for 2026

Your stack needs five layers: data provider, intent signals, outreach platform, CRM, and automation glue.

| Tool | Category | Starting Price |

|---|---|---|

| Prospeo | Data + verification | Free; ~$0.01/email |

| Apollo | Data + outreach | $59/user/mo |

| ZoomInfo | Enterprise data | $15,000+/yr |

| Cognism | Global data + compliance | $15,000+/yr |

| Lusha | Quick lookups | $49/user/mo |

| Bombora | Intent data | $25,000+/yr |

| Instantly | Cold email | $47/mo |

| Lemlist | Multi-channel outreach | $91/user/mo |

| HubSpot | CRM | $15/seat/mo |

| Salesforce | CRM | $25/user/mo |

Choosing the right data provider for fintech outbound means prioritizing data freshness and compliance features over raw database size. Stale data isn't a minor inconvenience - it's the difference between pipeline and domain blacklisting. Prospeo's 7-day data refresh cycle matters here because fintech executives change roles frequently, and a 6-week-old record is already decaying. The 30+ search filters include buyer intent signals across 15,000 topics, technographics, job changes, headcount growth, and funding events - exactly the trigger signals that drive fintech outreach. (If you’re comparing vendors, start with B2B company data providers.) Snyk's team of 50 AEs saw their bounce rate drop from 35-40% to under 5% after switching, with AE-sourced pipeline up 180%.

Trigger-based fintech outbound only works if you reach the right person within 24 hours. Prospeo layers intent data across 15,000 Bombora topics with funding signals, job changes, and 30+ filters - so you hit fintech buyers the moment they enter a buying window.

Find in-market fintech buyers with intent signals and verified direct dials.

Data Quality: The Foundation Nobody Talks About

Here's a stat that should frustrate you: 79% of marketing leads never convert into sales. Bad nurturing gets the blame, but bad data is the silent accomplice. If 35% of your list bounces on the first sequence, you've already damaged your sender reputation before a single prospect reads your message. (If you’re diagnosing, use email reputation tools.)

In fintech, this hits harder. Your buyers work at companies that handle sensitive financial data. They notice when emails come from domains with poor reputation scores. They're more likely to flag you as spam. And once your domain is flagged, recovery takes weeks - weeks you don't have in a 6-12 month sales cycle.

The standard we recommend from any data provider: a 7-day refresh cycle, not the 6-week industry average. If your current provider can't deliver that, your outbound is leaking before it starts.

Common Mistakes That Kill Fintech Pipeline

ICP too broad. "Fintech companies" isn't targeting. Segment by sub-vertical, transaction volume, regulatory environment, and tech stack.

Ignoring compliance stakeholders. If your outreach only targets the CTO, you're missing the compliance officer and legal counsel who hold veto power. Map the full buying committee before you sequence.

Gating content behind forms. Compliance teams at regulated companies won't fill out your lead capture form. Ungate your best content and capture intent signals instead.

Relying on stale purchased lists. A list that's 60 days old is already decaying. In fintech, where exec turnover is high and companies restructure around funding events, stale data is worse than no data.

No speed-to-lead process. When a trigger fires, you have 24 hours to reach out before the window closes. If your team takes a week to act on signals, you're losing to competitors who don't.

Treating all fintech sub-verticals the same. The playbook for selling into InsurTech looks nothing like selling fraud detection to neobanks. Customize your sequences, value props, and compliance messaging for each segment.

FAQ

What's a realistic CPL for fintech leads?

Expect $150-400+ per qualified lead via PPC or content syndication, with SEO producing the lowest long-term CPL after a 4-6 month ramp. Enterprise deals with six-figure contract values can justify customer acquisition costs of $500-$1,500+. Channel choice should match your sales cycle and ACV.

How long before a fintech lead gen program produces results?

Trigger-based outbound can produce first meetings within 2-4 weeks if your data and signals are dialed in. SEO takes 4-6 months to generate consistent inbound. ABM programs targeting enterprise fintech accounts need 6-12 months to build meaningful pipeline.

Should I outsource or build in-house?

For enterprise deals above $100K, in-house SDRs who understand compliance language and regulatory nuance will outperform outsourced teams. Early-stage companies should start with self-serve tools and run outbound themselves, then hire once the motion is proven.

What's the best channel for fintech B2B leads?

Trigger-based outbound wins for speed to pipeline. SEO wins for compounding ROI - a 14.6% close rate versus 1.7% for outbound makes the math obvious over time. Most successful teams run both simultaneously rather than choosing one.

How do I stay TCPA compliant with fintech outbound?

Since January 2025, you need one-to-one consent per seller for calls and texts - no blanket opt-ins. Use explicit, unchecked checkboxes, store consent records in your CRM, and provide clear opt-out mechanisms. Separate consent by channel, as call consent doesn't cover SMS.