How to Calculate SAM: The Founder's Guide to a Defensible Number

You're staring at a blank market sizing slide. You've read five articles that all say "TAM times percentage," and you still don't know what that percentage should be.

Stop obsessing over TAM. Knowing how to calculate SAM is the only thing that matters for the next 18 months.

About 42% of startups fail because there's no market need. That's not a funding problem or a product problem - it's a sizing problem. And it almost always starts with a serviceable addressable market that's either inflated beyond belief or so vague it collapses under a single investor question.

The Quick Version

SAM Formula:

SAM = Number of Target Customers in Your Serviceable Segment x [Average Revenue Per Customer](https://stripe.com/resources/more/what-is-average-revenue-per-user-why-it-matters-and-how-to-calculate-it) (ARPU/ACV)Or:SAM = TAM x % of Market You Can Realistically Serve

SAM is the slice of your TAM you can actually reach and sell to today, filtered by geography, regulations, channel capacity, product fit, and buyer readiness. Bottom-up is the credible method - count real customers, multiply by a realistic price. If you can't defend the number in 60 seconds to an investor, it's not done yet.

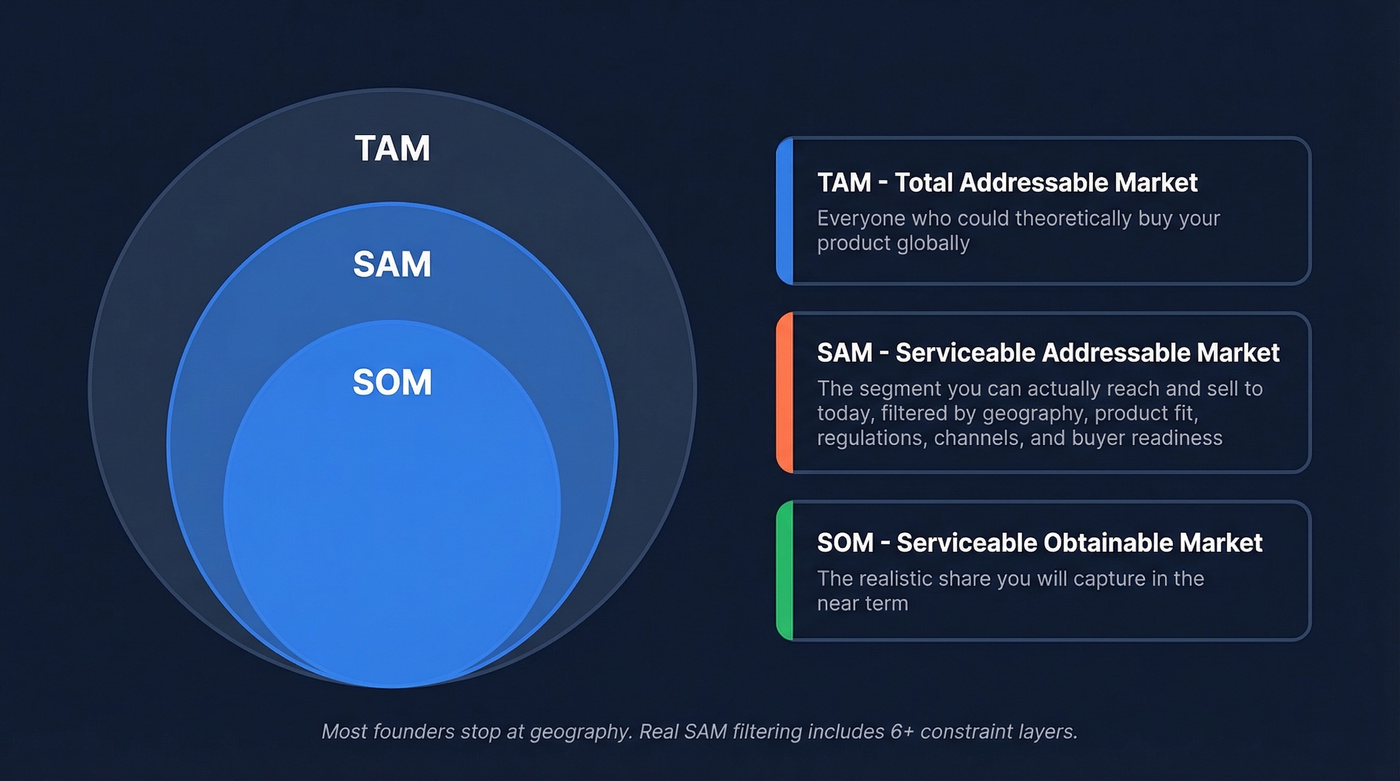

What Is SAM?

TAM is the total revenue opportunity if you had 100% market share globally. It's the dream number. SAM narrows that to the segment you can actually reach and serve right now - the portion of TAM that fits your current product, geography, and go-to-market capabilities. SOM is the realistic share of SAM you'll capture in the near term. (If you need a refresher, see our addressable market breakdown.)

Most founders treat SAM as "TAM minus geography." That's wrong. One Reddit founder sized their entire SAM by subtracting non-US revenue from a Gartner report and called it done - their investor tore it apart in under a minute. SAM filters include regulatory constraints, channel capacity, product limitations, competitive switching costs, and buyer readiness. A project management tool might have a global TAM, but if you only integrate with Jira and sell in English, your SAM excludes every team running Monday.com in Japan. Geography is one filter. It's rarely the most important one.

Step-by-Step SAM Calculation

Step 1: Start with TAM

You need a credible TAM before you can slice it. Use industry reports from Gartner, IDC, or IBISWorld for the top-down number, or calculate it yourself: total potential customers worldwide multiplied by average annual revenue per customer. Don't spend weeks here. TAM is the ceiling, not the answer.

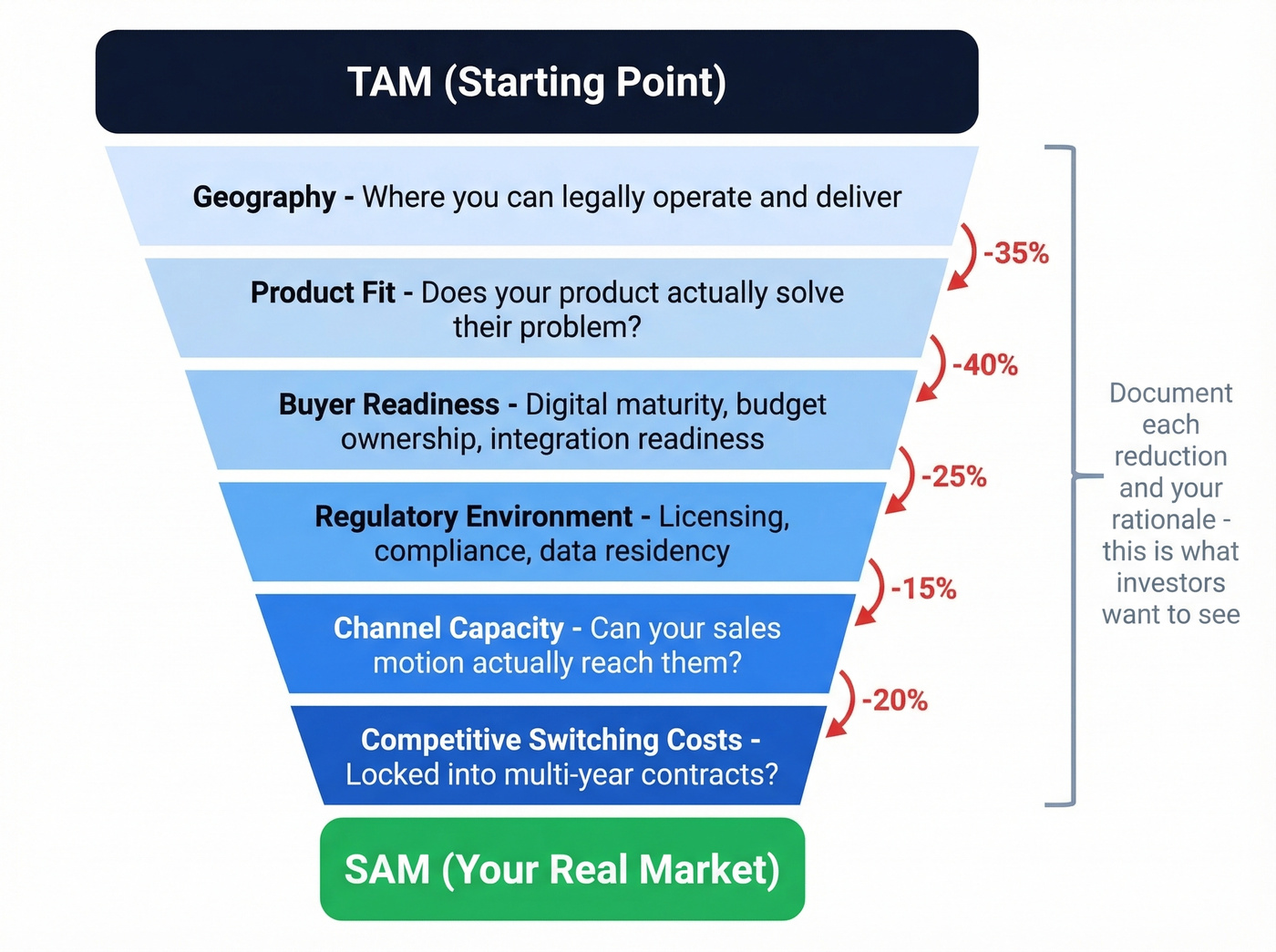

Step 2: Apply Constraint Filters

This is where most founders go wrong. They subtract one geography and call it a day. Your serviceable addressable market calculation needs to pass through every real-world filter that limits who you can actually sell to:

- Geography - Where you can legally operate and physically deliver

- Product fit - Does your product solve the problem for this segment, or just adjacent ones?

- Buyer readiness - Digital maturity, budget ownership, integration readiness. A company still running everything on spreadsheets isn't buying your AI platform this year.

- Regulatory environment - Licensing, compliance, data residency requirements that exclude certain markets

- Channel capacity - Can your sales team, partnerships, or self-serve motion actually reach these buyers? (If you're building outbound capacity, borrow these sales prospecting techniques.)

- Competitive switching costs - Buyers locked into multi-year enterprise contracts aren't in your SAM today

Each filter reduces your number. Document the percentage reduction and your rationale for each one. That's what investors actually want to see.

Step 3: Build Bottom-Up

Stop guessing percentages. Count real target customers and multiply by your realistic annual price. This is the method investors trust because it forces you to prove you know who your buyer is. If you haven't nailed your ICP, start with an ideal customer profile template.

SAM = Addressable accounts after filters x Average annual contract value

If you're selling a $12,000/year SaaS product and there are 8,000 companies that match your filtered criteria, your SAM is $96M. Simple math, defensible logic.

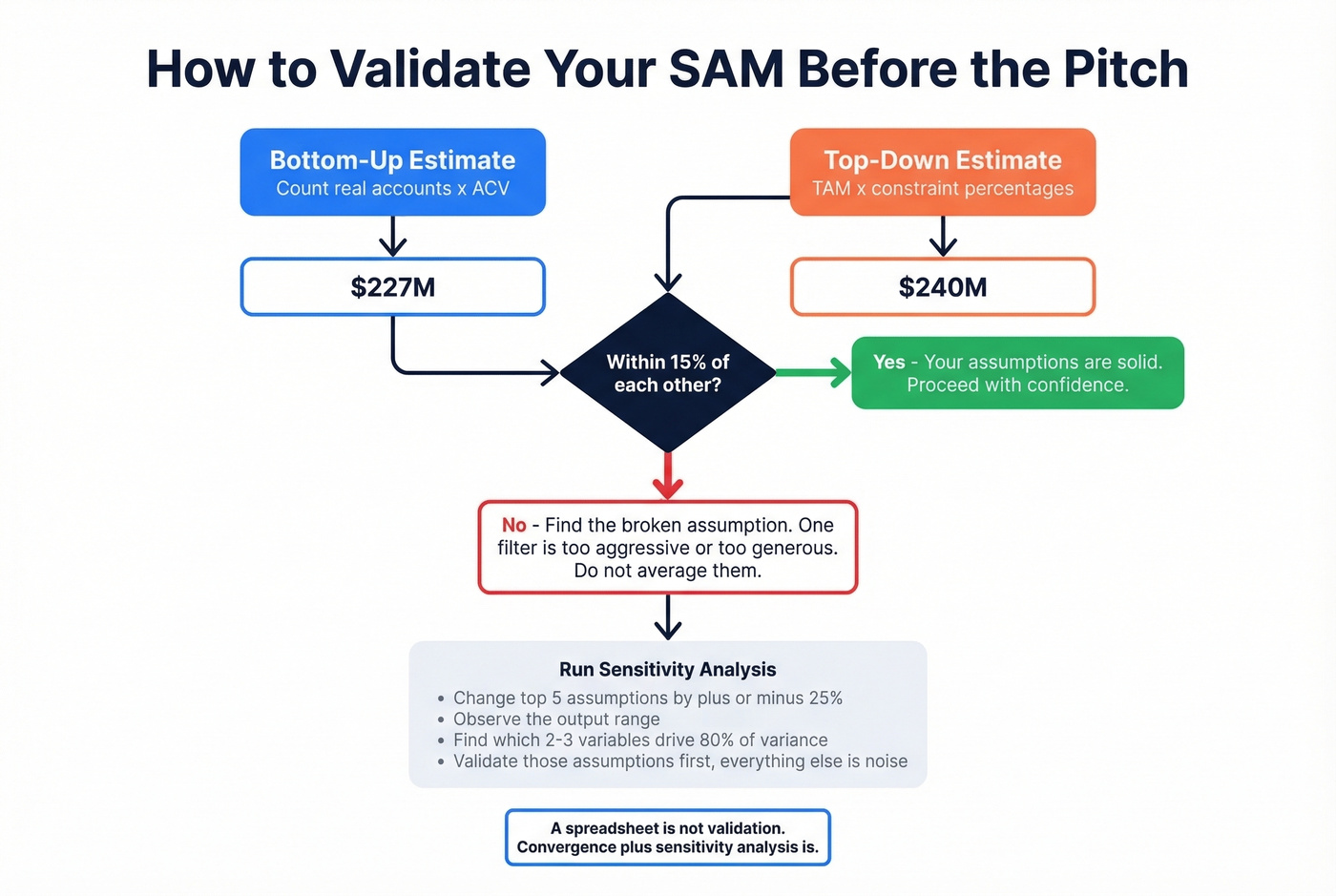

Step 4: Cross-Check with Top-Down

Run the top-down calculation separately: take your TAM and apply your constraint percentages. If your bottom-up and top-down estimates converge within roughly 15%, your assumptions are solid. If they diverge by more than that, don't average them - find the broken assumption. One of your filters is too aggressive or too generous.

Worked Examples with Real Numbers

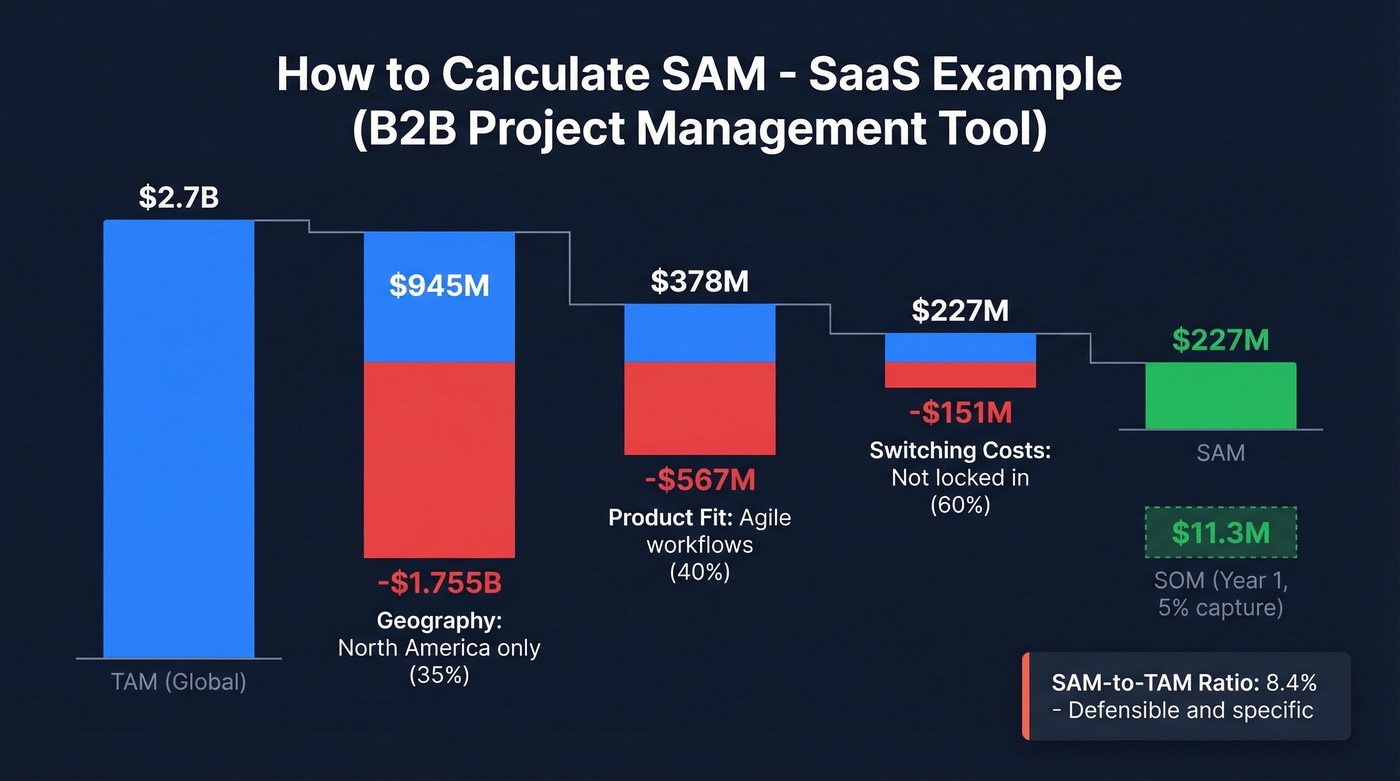

SaaS Example (B2B)

Let's say you're building a project management tool for mid-market companies with 100-1,000 employees in North America.

| Step | Calculation | Result |

|---|---|---|

| TAM (global) | 180,000 companies x $15K ACV | $2.7B |

| Geography filter | North America = ~35% | $945M |

| Product fit | Uses agile workflows = ~40% | $378M |

| Switching costs | Not locked in = ~60% | $227M |

| SAM | $227M | |

| SOM (Year 1, 5% capture) | $11.3M |

That's a SAM-to-TAM ratio of about 8.4%. Defensible, specific, and you can explain every filter. The SOM line shows investors you understand the gap between addressable and capturable - a distinction that separates serious founders from slideware. (More on positioning this slide in TAM SAM SOM in marketing.)

Physical Product Example

One founder on Reddit shared their actual sizing exercise for a medical device distributor. They identified 347 potential distributors nationally, each worth roughly $3,000/year in revenue. That's a TAM of about $1.04M. Then they applied real constraints: launching in 2 states covers around 12% of distributors, and only firms with 50+ employees qualify - about 40% of the remainder.

| Step | Calculation | Result |

|---|---|---|

| TAM | 347 distributors x $3K | $1.04M |

| Geography (2 states) | x 12% | $125K |

| Firm size filter | x 40% | $50K |

| SAM | $50K |

Small number? Good. It's real. Investors respect a founder who says "$50K SAM in year one, expanding to $125K as we go national" far more than one who waves around a billion-dollar TAM with no logic behind it.

Your SAM is only as good as your account list. Prospeo's B2B database lets you apply 30+ filters - headcount, revenue, technographics, funding, and buyer intent - across 300M+ profiles to count real target accounts, not inflated guesses from a Gartner report.

Stop estimating your SAM. Build it from verified accounts.

SAM for SaaS: Why Formulas Break Down

SaaS market sizing fails for structural reasons, not arithmetic ones. The standard formula of "count accounts times ACV" hides several traps.

Account universes are almost always over-inclusive. Inactive entities, subsidiaries without budget authority, and dissolved companies inflate your denominator. We've seen account lists shrink by 20-30% after basic entity verification - and that's before applying any product-fit filters. (If you're using firmographics/technographics, implement consistent firmographic filters.)

Then there's ACV. Your $15K mid-market price doesn't apply to the 200-person company the same way it applies to the 900-person one. Segment your pricing or your SAM is fiction.

The third trap is adoption velocity, and it's the one most founders ignore entirely. Enterprise procurement cycles exceed 12 months. Vendor lock-in creates real switching friction. A company that just signed a 3-year contract with your competitor isn't in your serviceable market - they're in your 2029 market. Demographic segmentation alone (industry, employee count, geography) isn't enough. You need to account for digital maturity, integration readiness, and actual budget ownership.

10 Mistakes That Kill Credibility

- The "1% of a massive market" pitch. The fastest credibility killer in any investor meeting. It signals you haven't done the work.

- Over-relying on top-down analysis. Industry reports give you a starting point, not an answer. Combine with bottom-up or you're guessing.

- Ignoring geographic restrictions. Legislation, logistics, and local policies exclude markets. Don't count revenue you can't legally earn.

- Generalizing your target demographic. "All mid-market companies" isn't a segment. Narrow by needs, budgets, and buying behavior.

- Overlooking product limitations. Your tool serves a niche. Don't size it against the whole industry.

- Using outdated data. Markets shift fast. A 2023 report won't cut it for a 2026 pitch.

- Assuming 100% market share. Even in your SAM, competitors exist. Price sensitivity matters.

- Failing to model price sensitivity. A 20% price increase can materially shrink your addressable market. Use price ranges and research the demand curve.

- Confusing TAM, SAM, and SOM. If your SAM slide shows a number bigger than your TAM, you've lost the room.

- Never updating. Markets change, competitors enter and exit, your product evolves. Recalculate at least annually.

How to Validate Your SAM

A spreadsheet isn't validation. Here's what actually works.

Run sensitivity analysis. Change your top 5 assumptions by plus or minus 25% each and observe the output range. Identify which 2-3 variables drive 80% of the variance. Those are the assumptions you need to validate first - everything else is noise. (If you're tying this to pipeline planning, use funnel metrics to keep assumptions consistent.)

Check convergence. If your bottom-up and top-down numbers land within 15% of each other, you're in good shape. If they don't, dig into the gap before you put the number on a slide.

Where to Get the Data

Instead of estimating "roughly 5,000 mid-market SaaS companies in the US," use a B2B database to filter by industry, company size, geography, and other criteria to get an actual count. That turns a guess into a data point - and that's the difference between a market size that survives diligence and one that doesn't. (If you're evaluating vendors, start with B2B company data providers.)

| Source | Type | Best For | Cost |

|---|---|---|---|

| US Census Bureau | Free | Business counts by NAICS/size/state | Free |

| BLS | Free | Employment/roles by industry | Free |

| SEC Filings | Free | Public company financials | Free |

| UN Data / ITC Trade Map | Free | International markets, trade | Free |

| Crunchbase | Freemium | Company + funding data | Free; Pro ~$50+/mo |

| Statista | Freemium | Market data, charts | Free basic; ~$80+/mo |

| Prospeo | Freemium | B2B account counts, 30+ filters | Free tier; ~$0.01/email |

| IBISWorld | Paid | NAICS-mapped industry reports | ~$1,000-$5,000+/year |

| Gartner / Forrester / IDC | Paid | Analyst reports, top-down data | ~$2,000-$5,000+ per report |

| PitchBook | Paid | Investor-grade company data | ~$20,000-$50,000+/year |

Free government sources give you the macro picture. Paid databases fill in the company-level detail. For B2B, you need both - macro to frame the TAM, micro to count the accounts that actually make up your serviceable addressable market.

Here's the thing: if your deal sizes are under $10K, you probably don't need PitchBook-level data. Census data plus a solid B2B database gets you 90% of the way there at a fraction of the cost.

You just learned that inactive entities and subsidiaries inflate account lists by 20-30%. Prospeo's 7-day data refresh and 5-step verification eliminate dead records so your bottom-up SAM reflects companies that actually exist, have budget, and match your ICP.

A defensible SAM starts with data refreshed every 7 days, not 6 weeks.

Presenting SAM to Investors

Start big with TAM to show ambition, narrow to SAM for product-market fit and GTM focus, then land on SOM for execution clarity. Show the constraint logic at each step. If you want the slide to actually land, apply a bit of sales deck storytelling instead of dumping numbers.

Spectup reviewed 1,000+ pitch decks and found market sizing is the "most consistently weak" slide. The fix isn't a bigger number - it's a defensible one. Your SAM and your financial model must align. If your SAM says $2M addressable and your model projects $5M in revenue, you've just told the investor you can't do math. (To sanity-check the model, map assumptions to cost to acquire customer and conversion rates.)

Let's be honest - we've reviewed dozens of pitch decks where the SAM number and the revenue model live in completely different universes. Investors notice. Every time.

FAQ

What's the difference between TAM and SAM?

TAM is the total revenue opportunity assuming 100% global market share. SAM narrows that to the segment you can actually reach given your geography, product capabilities, channel capacity, and regulatory constraints. TAM is the dream; SAM is the plan. Most investor-ready decks show SAM at 5-15% of TAM for a single-country launch.

How do you calculate SAM from TAM?

Apply constraint filters to your TAM: geography, regulations, channel capacity, product fit, competitive switching costs, and buyer readiness. Multiply the remaining addressable customers by your average revenue per customer. Document each filter's percentage reduction and rationale - that transparency is what makes the calculation credible.

What's a good SAM-to-TAM ratio?

There's no universal benchmark - it depends entirely on your constraints. A SaaS tool launching in one country typically lands at 5-15% of global TAM. The ratio matters less than your ability to defend the filters you applied. Investors care about logic, not a magic number.

How do you estimate SAM with no revenue data?

Count real target accounts via Census data, industry databases, or a B2B platform with firmographic filters. Multiply by a realistic price point validated through 10-15 prospect conversations, then apply your constraint filters. No revenue history needed - just real account counts and honest pricing.

How often should you recalculate SAM?

At minimum annually. Markets shift, competitors enter and exit, regulations change, and your product capabilities evolve. Stale numbers signal laziness to investors and lead to misallocated GTM resources internally.