How to Cold Call for Insurance Leads: The 2026 Playbook

It's 8:15 a.m. on a Monday. You've got a list of 200 names, a lukewarm coffee, and a script you printed from an agency forum. By 9:30, you've hit 40 dials, reached 6 voicemails, and talked to one person who hung up right after "I'm calling about your insurance."

The average cold call converts at roughly 2%, but that assumes you're reaching real people on real numbers. Most agents obsess over their script while dialing disconnected lines at noon. Fix the inputs first, and the conversations follow.

Here's the thing: cold calling still works. One data point we keep coming back to is that 69% of buyers accepted cold calls from new providers in the past year. The channel isn't dead - it's just done badly.

Your results come down to three things, in this order: clean data, smart timing, and a conversational script. Get the data right and call during the windows that actually work, and a mediocre script will beat a brilliant one dialed into dead air.

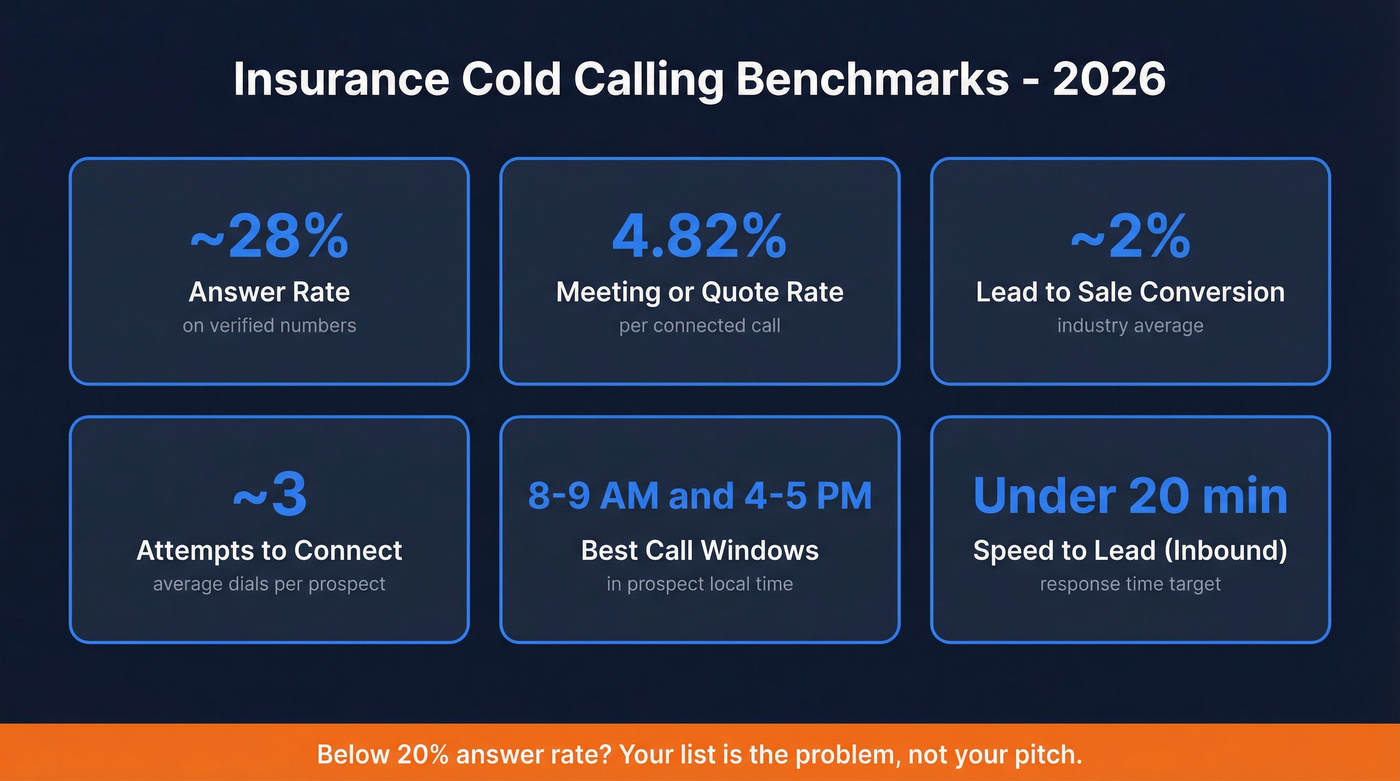

Benchmarks worth knowing

Before you change anything, know the numbers. These benchmarks are commonly cited across cold-calling research and line up with what we see in the field:

| Metric | Benchmark |

|---|---|

| Answer rate | ~28% |

| Meeting/quote rate | 4.82% |

| Lead-to-sale conversion | ~2% |

| Attempts to connect | ~3 |

| Best call windows | 8-9 a.m., 4-5 p.m. |

| Speed-to-lead (inbound) | Under 20 min |

If you're below a 20% answer rate, your list is the problem, not your pitch.

The step-by-step workflow

We've seen this workflow produce the most consistent results for insurance agents running outbound. It's not fancy. It just works when you run it the same way every day.

If you want to tighten the rest of your outbound motion too, borrow a few sales prospecting techniques that translate well to insurance.

1) Verify your list before you dial. If you only change one thing, make it this. Bad numbers destroy your answer rate, wreck your mood, and quietly train you to rush calls because you feel behind.

If you're comparing vendors, start with a quick scan of data enrichment services so you know what “verified” actually means.

2) Load your dialer and do 30 seconds of prep. Import the cleaned list into your dialer and turn on local presence if your setup supports it. Tag leads by line of business so your opener matches the product you're actually calling about.

Before each dial, grab just enough context to sound like a person: city, rough age bracket if you have it, and any notes from the lead source. Don't overdo it. Nobody likes the "I saw you live on Oak Street and drive a 2017 Camry" vibe.

3) Call in the windows that win. Block 8-9 a.m. and 4-5 p.m. local time. Midday can work, but it's where a lot of agents go to die slowly: people are busy, you're tired, and your tone gets sharp without you noticing.

4) Open with context, not a pitch. Name, reason, question. That's the formula. You don't need a monologue.

If you want more ways to keep your opener human, steal a few talk track examples.

5) Qualify fast (2-3 questions). You're confirming fit, not running a full needs analysis. Think: current coverage, renewal timing, and one life-change question (move, new car, new baby, retirement, Medicare eligibility).

A simple lead scoring rubric can help you decide who gets a second call vs. a text.

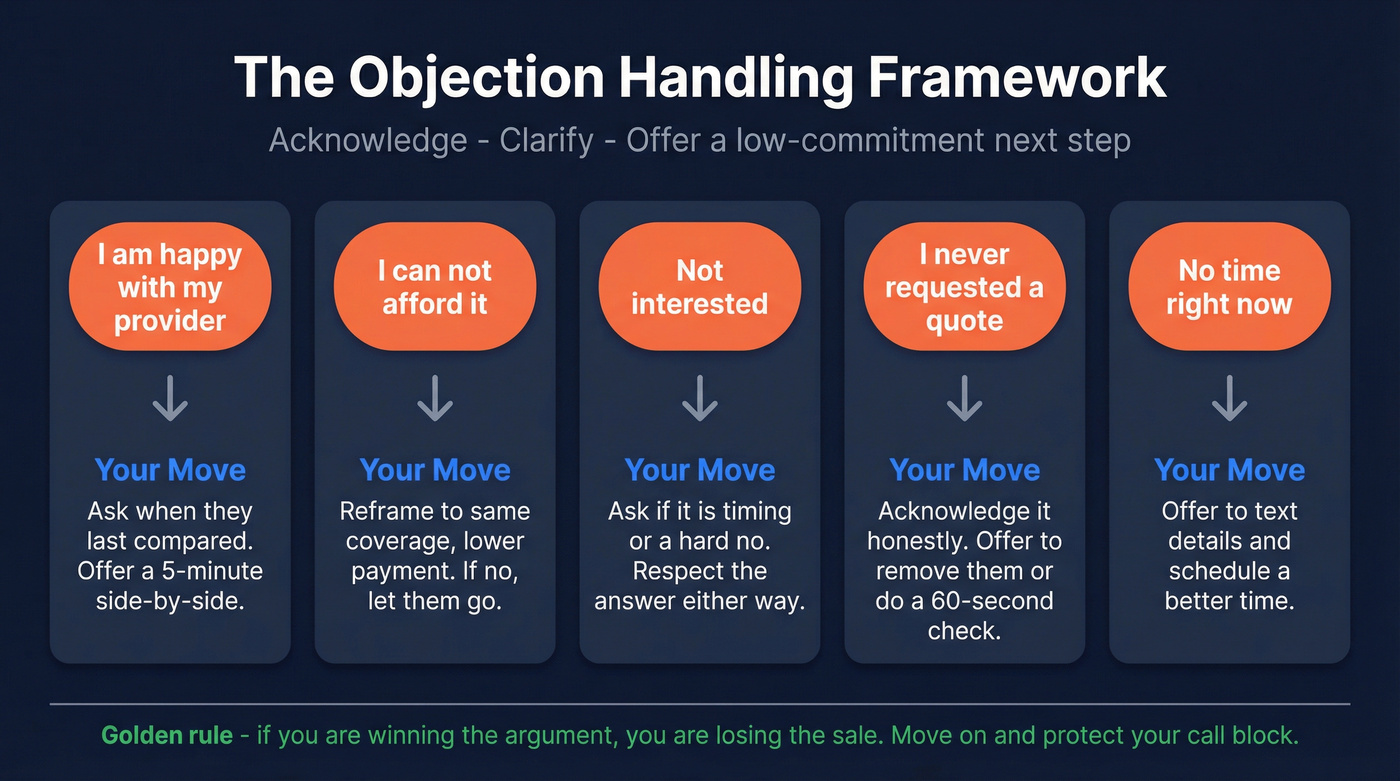

6) Handle objections without arguing. Acknowledge. Ask one clarifying question. Offer a low-commitment next step. If you find yourself "winning" the debate, you're losing the sale.

If this is your biggest leak, use a few frameworks from how to reduce sales objection rate.

7) Book a specific next step. Never end with "I'll call you sometime." Put a time on the calendar, even if it's a 7-minute quote review. This one change alone can clean up a messy pipeline because it forces you to separate "polite" from "progress."

8) Log every call in your CRM. Notes, disposition, next action. If you don't track it, you'll re-ask the same questions next week and sound like you don't listen. CrankWheel has a solid practical breakdown of the basics here: the ultimate guide to cold calling for insurance brokers and agents.

If your CRM setup is messy, start with these examples of a CRM and copy the fields you actually need.

9) Follow up multichannel. Calls plus email plus text gets dramatically better response than calls alone. Martal cites a 287% higher response rate when you don't rely on a single channel, and that matches what most high-volume agents figure out the hard way.

To make follow-up easier, keep a few plug-and-play sales follow-up templates ready.

Scripts that actually work

Let's be honest: most "insurance cold calling scripts" are written like a robot trying to pass as a human. The best scripts are simple, and they leave room for the prospect to talk.

One quick tone rule our team uses: if you catch yourself speeding up, you're nervous. Slow down. Drop your voice a little. And stop trying to sound "professional" in the way that really means "vague."

If you're newer to the phone, this cold calling for beginners guide will help you avoid the common traps.

Life and final expense

"Hi [Name], this is [You] with [Agency]. I'm reaching out because a lot of folks in [City] have been reviewing their life coverage after rate changes this year. I'm not trying to sell you anything on this call - I just wanted to see if it'd make sense to do a quick comparison. Do you have about two minutes?"

Why it works: it gives a reason, removes pressure, and asks for a small yes. Cold calling for life insurance goes best when you lead with relevance (rate changes, new grandkids, a recent move) instead of "Do you have life insurance?"

Auto and home

"Hey [Name], it's [You] from [Agency]. Quick question - are you open to a fast comparison on your auto and home? I've been helping people in [Area] save about $30-$50 a month by bundling, and I can tell you in a couple minutes if it's even worth looking at."

Health and Medicare

"Hi [Name], this is [You]. I help people in [County] compare health coverage options. Before I let you go, are you happy with what you're paying and what it covers, or would a quick review be helpful?"

Voicemail drop

"Hi [Name], this is [You] with [Agency]. I'm reaching out about your [coverage type]. I'll try you again [day], but you can call me back at [number]. Thanks."

One scenario we see constantly: you leave a clean voicemail, then send a short text that says "Just left you a voicemail - want me to run a quick comparison?" That combo pulls replies from people who'd never pick up an unknown number, and it keeps you from hammering the same lead with five more calls out of frustration.

If rejection is getting in your head, read this on cold call rejection and keep dialing.

You just read it: if your answer rate is below 20%, the list is the problem. Prospeo gives you 125M+ verified mobile numbers refreshed every 7 days - not the stale purchased lists most insurance agents burn through. At 30% pickup rate, you'll actually talk to prospects instead of voicemail boxes.

Fix your inputs first. Start dialing numbers that actually ring.

Handling common objections

You'll hear the same pushback on repeat. The goal isn't to "overcome" objections. It's to keep the conversation normal.

"I'm happy with my current provider."

"Good - that's what I like to hear. Quick one: when's the last time you did a side-by-side comparison? If it's been a while, I can run one and tell you in five minutes if there's anything worth changing."

"I can't afford it right now."

"Totally fair. If we could keep the coverage the same and lower the payment, would you want to see that? If not, I'll get out of your hair."

"Not interested."

"Got it. Is it the timing, or are you set on your current setup? I'm fine either way - I just don't want to keep bothering you if it's a hard no."

"I never requested a quote."

"You're right, and I appreciate you saying that. Your info can come through partner sites sometimes. I can remove you right now, or if you've got 60 seconds, I can at least tell you whether you're in the range most people in [Area] are paying."

"No time right now."

"No problem. Want me to send a quick text with what I'd compare, and you tell me a better time - today after 4, or tomorrow morning?"

Look, the worst feeling in insurance outbound is realizing you're arguing with someone who already decided. Don't do it. Move on, keep your tone clean, and protect your call block.

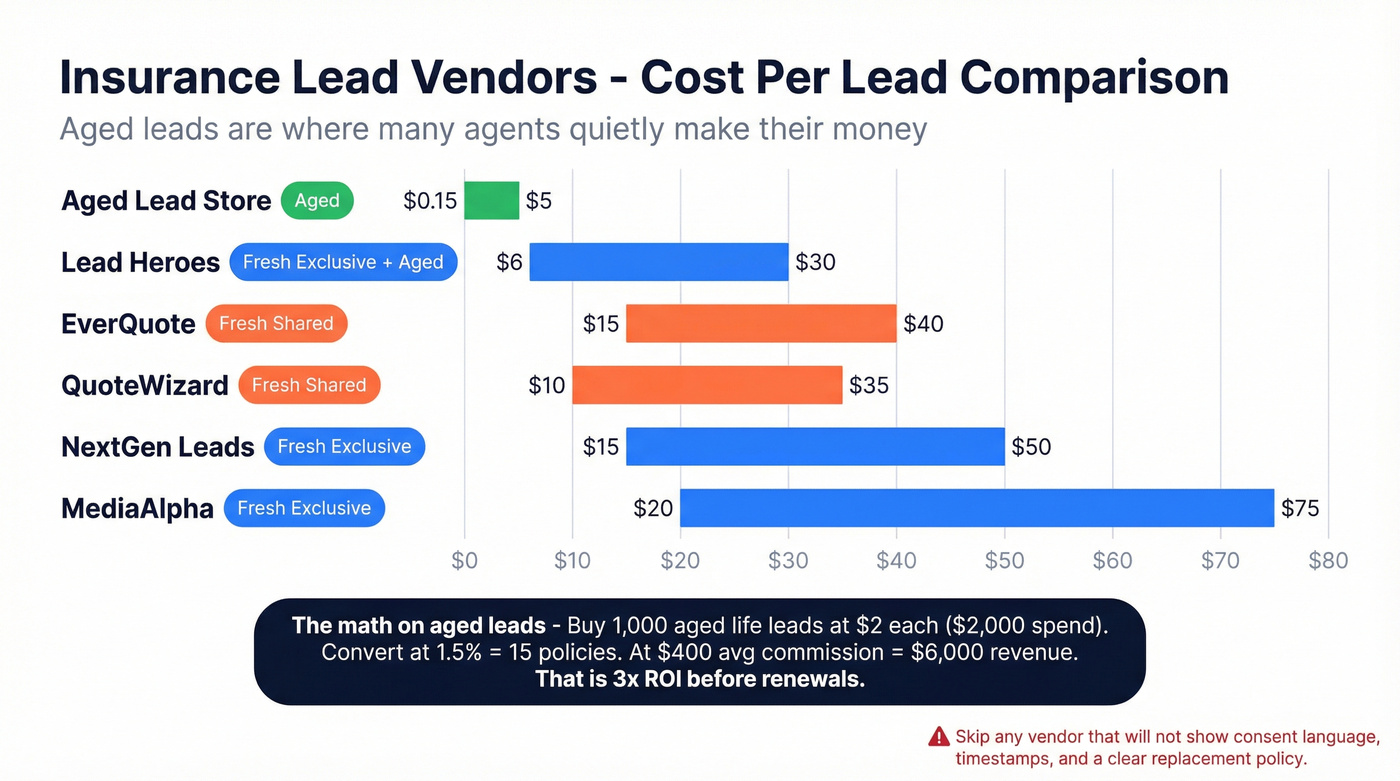

Where to get leads (and what to skip)

Your lead source determines your economics more than anything else. A great closer can't fix a list full of wrong numbers and angry people who never opted in.

| Vendor | Lead type | CPL range |

|---|---|---|

| Aged Lead Store | Aged (15-2,000+ days) | $0.15-$5 |

| Lead Heroes | Fresh exclusive + aged | $6-$30 |

| EverQuote | Fresh shared | $15-$40+ |

| QuoteWizard | Fresh shared | $10-$35+ |

| NextGen Leads | Fresh exclusive | $15-$50+ |

| MediaAlpha | Fresh exclusive | $20-$75+ |

Aged leads are where a lot of agents quietly make their money. Aged Lead Store points out that 60-80% of insurance policies are sold more than 60 days after the first inquiry. That matches the reality of how people buy insurance: they procrastinate, they get distracted, and they only act when something forces the decision.

Here's the math, and it's worth sitting with it for a minute because it changes how you buy leads. Buy 1,000 aged life leads at $2 each. Convert at 1.5% and that's 15 policies. At $400 average commission, that's $6,000 revenue on a $2,000 spend, before renewals. It's not magic, it's follow-up.

If you want a cleaner way to think about unit economics, map it to your cost to acquire customer and work backward.

Hot take: if your average commission is under $200, skip fresh exclusive leads. The CPL math usually doesn't work unless your process is tight and you're running serious volume.

And a negative recommendation you won't hear from lead sellers: skip any vendor that won't show you consent language, timestamping, and a clear replacement policy. You'll pay for it later in chargebacks, complaints, and wasted time.

Reddit's not always right, but it's honest. The consensus in r/InsuranceAgent threads is pretty consistent: lead vendors get hammered for chargebacks and prospects saying "I never asked for this." Agents who verify numbers before loading the dialer cut wasted dials hard, and they also cut the number of accidental wrong-party calls that turn into complaints.

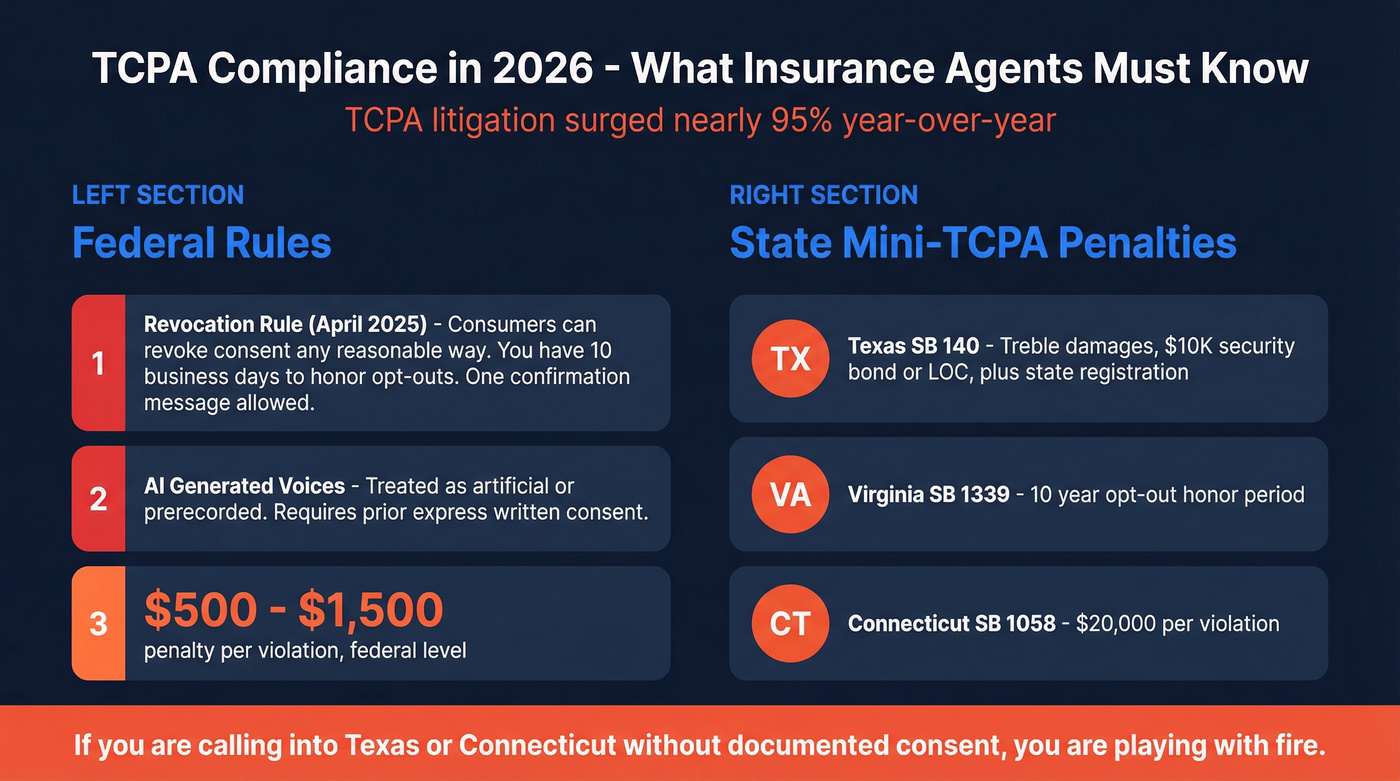

TCPA compliance in 2026

TCPA risk isn't theoretical anymore. Parker Poe notes that TCPA litigation surged nearly 95% year-over-year. If you're calling without documented consent, you're gambling with your agency.

A few rules to keep straight:

- Revocation rule (in effect since April 11, 2025): Consumers can revoke consent in any reasonable manner. You've got 10 business days to honor opt-outs, and you get one confirmation message.

- AI-generated voices: Treated as "artificial or prerecorded," which requires prior express written consent.

- Penalties: $500-$1,500 per call federally.

State mini-TCPA laws are tightening fast. A few examples that get agents in trouble:

| State | Key provision |

|---|---|

| TX (SB 140) | Treble damages, $10K security (bond/LOC), plus state registration requirements |

| VA (SB 1339) | 10-year opt-out honor period |

| CT (SB 1058) | $20K per violation |

Real talk: if you're calling into Texas or Connecticut without documented consent, you're playing with fire.

Your dialing tech stack

You don't need an expensive dialer to start. You need something reliable, plus a process you actually follow.

| Dialer | Starting price |

|---|---|

| Nextiva | ~$20-$30/mo |

| CloudTalk | ~$25/mo |

| Ringover | ~EUR21/mo |

| PhoneBurner | $140-$215/mo |

Auto dialers help you connect with more prospects without adding staff. Prioritize CRM integration, local presence, voicemail drop, and built-in DNC tools.

If you're evaluating platforms, this roundup of SDR tools can help you sanity-check features and pricing.

One more opinion from the trenches: don't buy a premium dialer to compensate for a messy list. Spend that money on verification and better lead buying. You'll feel the difference on day one, because your first call block won't be 30% wrong numbers.

Calls plus email plus text gets 287% higher response - but only if you have real contact data for all three channels. Prospeo returns verified emails (98% accuracy), direct mobile numbers, and 50+ data points per contact so you can run the multichannel follow-up this article recommends.

One platform for every channel in your insurance outreach stack.

FAQ

How many cold calls should an insurance agent make per day?

Aim for 80-100 dials in two focused one-hour blocks. At a ~28% answer rate, that's about 20-30 live conversations, which is enough to book one to two appointments if your list is clean and your follow-up's consistent.

Are aged insurance leads worth buying?

Yes, if you follow up like a professional. At $1-$6 per lead versus $20-$50 for fresh, aged leads can produce strong ROI because many policies close well after the original inquiry.

How do I verify my lead list before calling?

Run the numbers through a verification tool before you load your dialer. Prospeo's mobile finder checks against 125M+ verified mobile numbers, so you're not burning dials on disconnected lines and wrong-party calls.

Is cold calling for life insurance still effective in 2026?

Yes. Life and final expense remain strong for outbound because the product needs explanation, prospects rarely shop proactively, and commissions support the cost per dial. Combine verified contact data with tight call windows and a simple, human opener, and you'll see quote rates move fast.